A founder gets the signed term sheet back from the lead investor, scans the economics, and feels relieved for about five minutes. Then the last page says the round will use NVCA model forms. For many first-time founders, that line sounds reassuring and alarming at the same time. Reassuring because “standard” suggests efficiency. Alarming because no one wants to sign a stack of documents they don't understand and live with those terms for years.

That reaction is justified. The term sheet is only the headline. The ultimate allocation of economics, control, disclosure risk, and future fundraising flexibility sits in the definitive documents. In Seattle and across Washington, that matters even more for startups handling regulated data, selling into healthcare, using AI systems, or taking money from investors and founders with international ties. The forms may be standardized, but the risk profile rarely is.

The useful way to think about NVCA forms is simple. They are the market's shared drafting language for venture financings. They save time, narrow fights, and give experienced counsel a common baseline. They are not self-executing, and they are not “safe” just because they are common.

Navigating Your First Venture Term Sheet

A Seattle founder signs a term sheet on Friday, tells the team the round is basically done, and then spends Monday learning that detailed negotiation is just starting. The economics may fit on a few pages. The documents that govern board control, investor vetoes, future financings, founder transfers, and disclosure exposure do not.

That gap matters in Washington. I see it most often with companies that process sensitive data, have engineers or investors outside the United States, or expect to raise in tranches tied to product or regulatory milestones. In those deals, the term sheet rarely answers the questions that create friction later. The NVCA forms do.

The usual sequence goes like this. A founder spends weeks learning how founders secure venture capital, negotiates valuation and board seats, and finally receives a term sheet that says the deal will be documented on NVCA forms. Many founders read that as a sign that the legal work is mostly administrative. It is better to read it as a sign that the next set of decisions will be more technical and more durable.

NVCA forms became common because they give both sides a familiar starting point. They reduce drafting time, make markups easier to compare across firms, and help investors and company counsel focus on the key pressure points instead of rebuilding the same documents from scratch. Recent 2025 updates have also pushed parties to pay closer attention to national security review, foreign investor diligence, and milestone-based closings. For Washington startups with cross-border founders, defense-adjacent technology, AI applications, or customers in healthcare and critical infrastructure, those points are not side issues. They can shape who can invest, what information can be shared before closing, and whether one closing or multiple closings makes more sense.

What “standard” means in practice

Standard forms are market shorthand. They are not market outcomes.

A founder still has to make deliberate choices about:

- Downside protection. The charter and related approvals determine how much protection investors get if the company sells below expectations or raises a tougher next round.

- Information rights. Investors may ask for budgets, financial statements, inspection rights, and compliance reporting that feel routine until they become operational burdens.

- Control mechanics. Board composition, preferred veto rights, and stockholder approval thresholds decide who can block key actions when the company is under pressure.

- Future financing flexibility. Pro rata rights, pay-to-play concepts, transfer restrictions, and tranche conditions can either preserve room for the next round or make it harder to assemble.

For a first priced round, the practical goal is not to fight every provision. It is to identify which terms will matter if the company misses plan, needs insider support, brings in an out-of-state lead, or gets acquisition interest before reaching scale. Founders who prepare early usually handle this stage better, especially if they review startup funding and seed-stage legal planning for Washington companies before the first draft set arrives.

Practical rule: If the term sheet feels founder-friendly but the draft documents feel dense, review gets more important, not less.

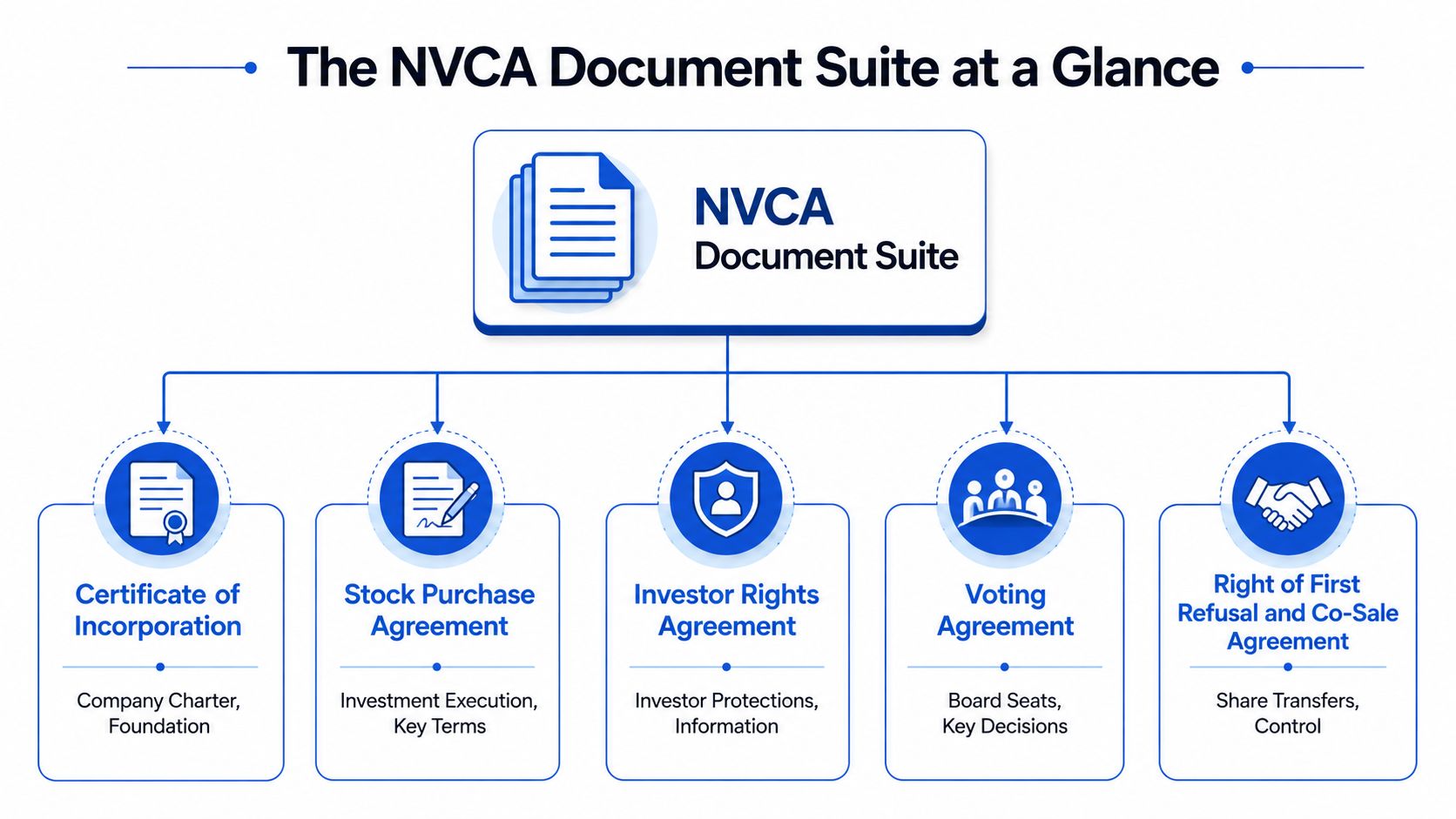

The NVCA Document Suite at a Glance

The cleanest way to understand NVCA model forms is to stop treating them as one pile of paperwork. They are a coordinated system. Each document governs a different part of the deal, and the package works because the pieces are designed to fit together.

The NVCA model legal documents page describes the package as the venture-capital market's de facto standardized financing set, consisting of the charter or certificate of incorporation, stock purchase agreement, voting agreement, investors' rights agreement, and right of first refusal and co-sale agreement. Practitioners use it as a modular system because each instrument addresses a different transaction layer, from security terms to governance and transfer controls.

The five documents and their jobs

| Document | What it does | Why founders should care |

|---|---|---|

| Certificate of Incorporation | Creates the preferred stock and sets its economic and voting rights | This is where liquidation preference, conversion mechanics, anti-dilution, and many protective rights live |

| Stock Purchase Agreement | Executes the sale of shares to investors | This is where reps, warranties, disclosure schedules, closing conditions, and purchase mechanics sit |

| Investors' Rights Agreement | Governs ongoing investor rights after closing | This controls information rights, pro rata rights, registration rights, and sometimes observer rights |

| Voting Agreement | Binds stockholders to certain voting commitments | This often locks in board composition and drag-along mechanics |

| ROFR and Co-Sale Agreement | Restricts transfers of founder and other stockholder shares | This controls who can get onto the cap table and how secondary sales happen |

How the package works in practice

A lot of first-time founders focus almost exclusively on valuation and maybe board seats. That's too narrow. The core drafting discipline is checking how one document changes the practical effect of another.

For example:

- The charter may define a preferred class vote.

- The voting agreement may determine who controls the board that recommends the action.

- The investors' rights agreement may give a major investor the information needed to pressure the issue early.

- The ROFR/co-sale agreement may limit a founder's ability to reshape the stockholder base later.

That interlocking structure is why founders shouldn't “fill in blanks” and move on. Good counsel adapts the package to the actual cap table, board dynamics, founder vesting position, and financing strategy, instead of pretending the startup is a generic software company with a generic investor group.

Deep Dive The Certificate of Incorporation

The certificate of incorporation is the heart of the economics. If the term sheet is the summary and the SPA is the mechanic, the charter is the source code. It creates the preferred stock the investor is buying and defines what that stock is worth in good outcomes, bad outcomes, and messy outcomes.

Founders often underestimate this document because it feels technical. That's a mistake. The charter determines what happens if the company sells for less than hoped, raises a down round, or needs investor approval for a major decision. A useful companion for that conversation is this explanation of preferred stock and how it differs from common, because the negotiation only makes sense once the founder sees how the security itself is engineered.

Liquidation preference drives real exit outcomes

The single question to ask is not “What's the preference?” It's “What waterfall does this language create?”

A non-participating preference usually gives investors a choice. They can take their preference amount back first or convert and share in the sale proceeds with common. A participating preference can let investors take the preference first and then share again in the remainder on an as-converted basis. That difference can materially change founder and employee proceeds in a modest exit.

A founder doesn't need a spreadsheet to understand the policy point. The more investor-favoring the preference, the more the exit has to outperform before common stock starts behaving like the headline valuation suggested.

The charter doesn't just price the round. It prices disappointment.

Anti-dilution is about future pain allocation

Anti-dilution provisions matter only if the company later raises at a lower price, but if that happens, they matter a lot. The central trade-off is between broad-based weighted average protection and more punitive structures.

A practical founder review should focus on these questions:

- What triggers the adjustment? Some issuances should be carved out, such as equity compensation or other customary exclusions.

- How broad is the formula denominator? Broader formulations are usually less punishing to common holders.

- Does the draft preserve flexibility for recruiting and strategic grants? A company that can't use equity flexibly often creates a bigger governance problem later.

Control terms often hide in “routine” provisions

The charter also handles consent rights and class votes over major actions. Some are ordinary and sensible. Investors should have a voice on fundamental matters such as amending the charter, issuing senior securities, or changing the rights of the preferred. The trouble starts when the consent list creeps into ordinary-course management.

A founder should be wary when approval rights reach into day-to-day decisions that belong at the board or management level. Overly broad controls can slow bank debt discussions, complicate employee equity grants, and create points of influence unrelated to true investor protection.

Here is a practical review lens:

| Founder question | Why it matters |

|---|---|

| Does this require investor consent for ordinary financing operations? | Routine approvals can become a veto over normal company growth |

| Are option pool actions appropriately carved out? | Hiring flexibility often gets constrained through sloppy drafting |

| Is the board structure workable after the next round? | A charter that works only at closing can create governance stress quickly |

For first-time founders, the charter is the document to read slowly. It carries consequences long after the closing dinner is forgotten.

Deep Dive The Stock Purchase Agreement

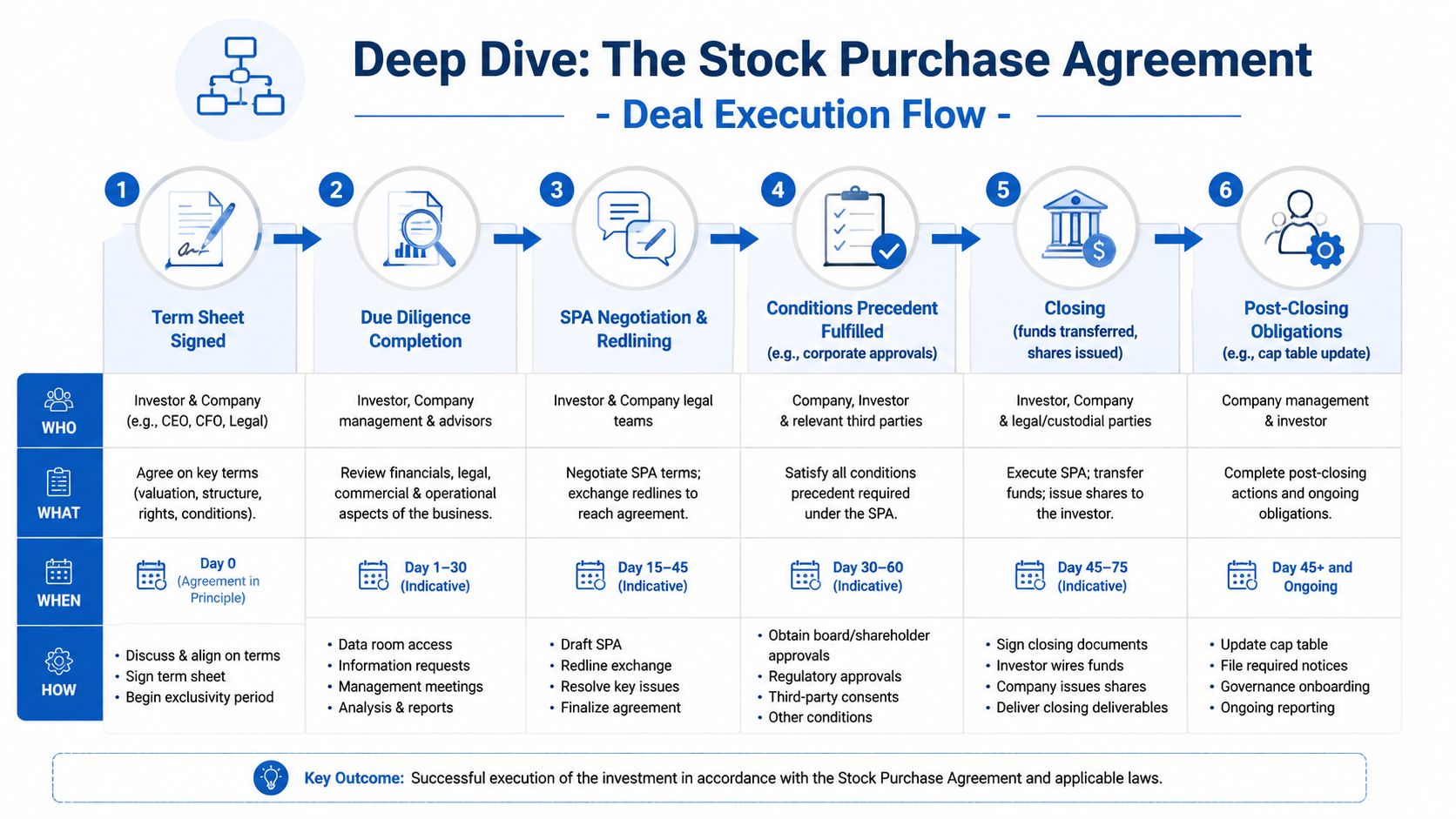

A founder often feels the pressure of the Stock Purchase Agreement the first time counsel asks for disclosure schedules on a Friday night, the lead wants to close next week, and someone finally realizes the company never collected invention assignments from two early contractors. That is a normal first-round moment. It is also why the SPA deserves more attention than many founders give it.

The SPA is the sale document. It states who is buying, how many shares they are buying, the price, the closing conditions, and the promises each side is making. For the company, those promises matter most. The representations and warranties are the part founders underestimate, because they turn messy operating facts into legally binding statements.

That process exposes real risk. If the company says it owns its IP, complies with applicable law, has paid taxes, and has disclosed material contracts, those statements need to be true as drafted or properly qualified in the schedules. In practice, the SPA is one of the best forcing mechanisms in the round. It flushes out issues management has been carrying informally.

The usual pressure points are predictable. Contractor IP assignments. Open source use that does not match the product team's assumptions. Privacy disclosures that were copied from an old website and never updated. Export controls for a company selling encryption, infrastructure, aerospace, robotics, or dual-use software. Customer side letters. Cap table mistakes from the pre-seed period.

A disciplined founder-side process usually looks like this:

- Start disclosure schedules early. The last week before closing is the worst time to discover missing signatures, side promises, or nonstandard customer terms.

- Match the reps to the business. A Washington AI company training on sensitive datasets has a different risk profile than a consumer app with no regulated data and no foreign operations.

- Qualify carefully. Overbroad qualifiers can start a fight with the lead. Under-disclosure creates a bigger problem if the issue resurfaces after closing.

- Pull in the right internal owners. Finance, product, security, and whoever manages contractors or vendor onboarding usually know facts legal does not.

The 2025 NVCA updates made this document more operational for founders. The revised forms added language that fits milestone-based or tranched financings and expanded national security and data security representations. For Washington companies, that shift matters. Many local startups have cross-border engineering teams, Canadian affiliates, overseas founders, government-facing customers, or data practices that raise questions investors did not ask with the same intensity a few years ago.

Tranched financing is a good example. It can solve a real valuation gap. An investor may agree to fund part of the round at closing and release the rest when the company hits a product, regulatory, or commercial milestone. Sometimes that structure keeps a deal alive. Sometimes it creates a new control problem.

The key issue is whether the milestone is measurable and who decides if it has been met. “Market readiness” is a recipe for argument. “Delivery of a named FDA submission package” or “execution of customer contracts meeting stated revenue and term thresholds” is much cleaner. I usually push founders to test every milestone with one question: if the relationship sours, could a neutral third party tell whether the milestone was satisfied without guessing at intent?

The newer security and foreign ownership reps also deserve careful review. In Seattle, that often means looking beyond the Delaware parent and asking practical questions about who has access to source code, where data is stored, whether any investor or founder has rights that could trigger foreign influence concerns, and whether the company's customers or products touch sensitive sectors. If there is a non-U.S. parent, a foreign subsidiary, or a distributed team handling sensitive code or data, the schedules should reflect those facts accurately rather than trying to smooth them over.

Washington founders should also remember that state-level compliance still feeds into national-form documents. The SPA may use NVCA language, but the diligence behind it is local and company-specific. Washington trade secret practices, employee invention assignment hygiene, privacy disclosures, and software contracting discipline all affect whether the reps can be made cleanly. Cross-border founders often feel this most sharply, because a structure that looks efficient for tax or hiring purposes can create extra work once the lead investor starts asking ownership, sanctions, export, and data-access questions.

One practical rule helps. Read every company rep as if it were a diligence checklist item that might become a closing condition. Because often it is.

A careful SPA review should cover beneficial ownership, data flows, key vendors, IP chain of title, sanctions and export exposure, and any business line that could draw national security scrutiny. Generic “market” drafting will not solve disorganized facts. Clean facts, sensible qualifiers, and clear schedules usually will.

Deep Dive The Investor Rights Agreement

After closing, the investors don't disappear into the cap table. The investor rights agreement governs the ongoing relationship. If the charter handles economics and the SPA handles the sale, the IRA decides what the investor gets to see, when they can double down, and how the company must accommodate them over time.

Many founders discover that the cost of capital isn't limited to dilution. It also includes reporting cadence, response burden, future allocation pressure, and obligations that can feel minor when the round closes and much less minor once the company is trying to run.

Information rights shape the operating rhythm

Information rights sound benign because serious investors do need visibility. In practice, though, the drafting determines whether the company is delivering sensible governance reporting or supporting a miniature public-company regime before it is ready.

A useful founder-side review asks three questions:

| Clause area | Healthy version | Problem version |

|---|---|---|

| Financial reporting | Timelines the finance team can actually meet | Deadlines that are unrealistic for a lean team |

| Budget delivery | Annual planning materials tied to actual board process | Rolling demands for frequent updates outside ordinary governance |

| Inspection or access rights | Limited to reasonable requests and proper purposes | Open-ended access that disrupts management time |

What works is tailoring the obligation to stage and sophistication. A company with a controller and mature board materials can carry more reporting than a startup still building basic close processes. The wrong move is agreeing to polished reporting obligations and then breaching them repeatedly because no one asked whether the company could operationally comply.

Pro rata rights are helpful until they crowd the next round

Pro rata rights let investors maintain their ownership in future financings. That sounds simple, and often it is. Existing investors want the chance to keep backing the company if it performs well.

The friction usually appears later, when a new lead investor wants room in the round, or when several smaller investors all claim participation rights that reduce allocation flexibility. For founders, the strategic issue isn't whether pro rata rights are “good” or “bad.” It's whether the rights fit the company's future financing plan.

A practical negotiation often focuses on:

- Who qualifies as a major investor. Thresholds matter because they determine who gets the full package.

- Whether the rights are transferable. Transferability can create unexpected cap table complexity.

- How the company preserves room for new money. Future lead allocation needs to remain workable.

Registration rights matter later, but drafting still matters now

Most startup founders won't spend much time thinking about registration rights during an early priced round, and that's understandable. They become relevant in a public offering context, not in the ordinary life of a private company. Even so, they shouldn't be ignored completely.

The main founder concern is proportionality. These rights should preserve future flexibility without creating avoidable obligations or process friction long before the company is remotely near a public transaction.

Information rights are easiest to negotiate before closing and hardest to soften after patterns of investor reporting are already established.

The investor rights agreement works well when it supports a functioning long-term relationship. It works poorly when it becomes a standing source of administrative debt.

Deep Dive The Voting and ROFR Agreements

The first real surprise for many founders comes after the economics are set. The term sheet says who gets a board seat and outlines basic transfer restrictions. The NVCA voting agreement and ROFR and co-sale agreement are the documents that turn those summary points into binding control terms. In a Washington company, that drafting matters because it affects day-to-day board function, future secondary sales, and how much flexibility remains when the next round gets harder or more conditional.

The voting agreement usually does two jobs. It binds the parties to a specific board construction, and it sets the drag-along rules for an exit. Those are not housekeeping points. They determine who can select directors, when those rights terminate, and what approvals are needed to force support for a sale.

Founders should read the board provisions with one practical question in mind. What happens after ownership changes? A lead investor who starts with a clear designation right may lose it below a threshold. A founder seat may be tied to continued service. An "independent" seat may require mutual approval, but the drafting can still give one side a quiet veto. In my experience, early-stage companies often find themselves giving up more control than intended due to these provisions, usually because the term sheet description sounded balanced and the final language was more specific than expected.

A clean review usually focuses on a short list:

- Board designation rights. Which holder or constituency names each seat, and what ownership or service conditions apply?

- Loss of designation rights. Do those rights fall away automatically, or only after notice and confirmation?

- Independent director selection. Does the process require genuine agreement, or can one camp stall until it gets its preferred candidate?

- Drag-along approval structure. Does a sale require board approval plus preferred and common support, or can one bloc force the result if the protective provisions are already satisfied?

The drag-along section deserves more attention in 2025 than it used to. More rounds now include milestone-based closings, extension options, or tranched financing mechanics. If the company misses a product milestone and the inside investors control the next tranche, the sale approval provisions can become part of the pressure campaign. A founder should ask whether the drag-along trigger gives fair protection to common stock if the company is sold in a down cycle, before the full financing plan plays out.

The ROFR and co-sale agreement addresses a different problem. It controls who gets onto the cap table through private transfers and who gets to sell alongside a founder or early holder. Investors want it because they do not want a stranger buying a meaningful stake without giving the company or the existing investor group a chance to step in. The company wants it for the same reason.

For founders, the harder issue is liquidity planning. A transfer restriction that looks standard can still block ordinary founder estate planning, a divorce settlement transfer, or a small pre-Series B secondary that would otherwise reduce personal pressure without changing control. The right answer is usually not to remove the restrictions. It is to draft sensible carve-outs, clear notice procedures, and realistic exercise periods so the process does not break every time someone needs consent.

This also connects to dilution planning. A secondary sale does not dilute the company, but transfer restrictions, pro rata participation, and board approval rights all affect who holds influence as ownership shifts over time. Founders who want a clearer baseline should understand how equity dilution changes ownership and control over multiple rounds before they treat a transfer document as minor cleanup.

Cross-border structures add another layer. Seattle startups often have a Washington operating company, a foreign founder, overseas engineering, or a parent-subsidiary structure created for tax or hiring reasons. In that setup, the voting agreement and transfer restrictions need closer drafting. Board observer rights, successor provisions, transfer exceptions, and information-sharing mechanics can all raise diligence questions if a new investor is sensitive to export controls, national security review, or foreign ownership concentration.

Washington founders should also pay attention to state corporate mechanics. If the company is a Washington corporation rather than a Delaware corporation, the enforceability analysis starts with Washington law and the charter documents, not just the NVCA form. The concepts are familiar, but details such as notice, stockholder approval thresholds, and the interaction between transfer restrictions and the company's governing documents should line up cleanly at closing. That is especially true when the company has converted from an LLC, has out-of-state stockholders, or expects a future flip into another jurisdiction.

These agreements work well when they are treated as operating documents, not annexes. They should fit the company you have: one founder or several, local or cross-border, one lead investor or a crowded syndicate, a single close or a tranched round with conditions attached. That is where the legal drafting starts to match the business reality.

Your Negotiation Strategy and Redline Tips

A founder doesn't need to fight every redline. In fact, that usually backfires. The better strategy is to know where influence matters, where market practice is truly market, and where “standard” language can still produce an off-balance outcome.

One practical issue gets overlooked constantly. The forms are actively maintained, and the major October 2025 update cycle is a reminder that version control matters across the entire financing stack. Practitioner guidance tied to the NVCA public policy and model legal document resources emphasizes refreshing term sheets, diligence checklists, and related deal materials because changes in one document can affect representations, covenants, and closing deliverables elsewhere.

Where founders should spend leverage

The highest-value negotiations usually sit in a short list.

- Economics that survive the term sheet. Liquidation preference mechanics, anti-dilution formulation, and option-pool treatment deserve close review because small drafting shifts can change long-term outcomes.

- Control rights that affect ordinary operations. Board designation, protective provisions, and drag-along triggers should protect investors without turning management decisions into repeated consent exercises.

- Future financing flexibility. Pro rata rights, transferability, and major investor thresholds can shape who fits in the next round and on what terms.

- Compliance-linked reps and covenants. National-security and data-governance language should reflect the business as it operates, not how a clean software startup would operate.

What to mark as market and what to challenge

A useful founder-side framework looks like this:

| Likely market | Worth scrutiny |

|---|---|

| Use of NVCA forms as a baseline | Overbroad investor vetoes on ordinary business |

| Standard transfer restrictions with sensible carve-outs | Drag-along provisions lacking balanced approvals |

| Ongoing information rights for meaningful holders | Reporting obligations the company can't realistically satisfy |

| Board governance commitments | “Standard” reps that don't fit the company's data or cross-border profile |

Process mistakes cause expensive problems

The legal issues are only half the job. Process discipline matters just as much.

A founder should insist on:

- One controlling draft set with tracked changes managed carefully.

- A version-date check to confirm the parties aren’t mixing old and updated forms.

- Cross-document consistency so rights in the charter match obligations in the IRA and voting agreement.

- A live issues list that separates material asks from cosmetic comments.

- A dilution review before closing, especially if the option pool or conversion assumptions changed. This overview of equity dilution and how it affects founders is a useful refresher before final numbers are locked.

Don’t measure negotiation success by how many comments were accepted. Measure it by whether the final documents behave the way the founder thinks they do.

The best redline strategy is selective, informed, and relentless on the points that echo into the next round or the next crisis.

Washington State Considerations and Next Steps

Washington founders rarely fit the cleanest version of the NVCA assumptions. Many Seattle-area startups combine software, AI, health data, enterprise services, regulated contracting, or international talent structures. That means the legal work is not just “venture docs.” It is venture docs plus state-specific contract, privacy, and governance judgment.

For companies with sensitive personal information, health-related data, or complex vendor chains, the newer data-security and diligence expectations in the updated forms need to be mapped against actual Washington operations. That review often starts with basic questions that should have been answered before the round but often weren’t. Where does data move, who touches it, what has the company promised in customer contracts, and do those promises match internal practice?

Washington drafting needs operational facts

Founders using tranched financings should define milestones with enough objective detail that they can be administered cleanly under ordinary contract principles. If the milestone depends on product readiness, customer delivery, regulatory work, or technical performance, the SPA should identify the evidence required to determine completion. Ambiguous milestones create exactly the kind of dispute no startup needs while waiting on the second tranche.

For companies with cross-border ownership or founder structures, governance drafting deserves extra care. As noted earlier, a recent cross-border analysis observed that 34% of 2025 venture deals involved founders with foreign incorporation and highlighted the lack of consensus on adapting certain NVCA voting provisions in ways that satisfy security compliance and disclosure concerns for startups with international capital, particularly relevant for Washington’s global startup ecosystem, as discussed in this analysis of cross-border NVCA issues.

A workable founder checklist

A Washington startup preparing for a priced round should line up these workstreams before the first major redline exchange:

- Corporate cleanup. Cap table accuracy, IP assignments, board approvals, and founder vesting status.

- Privacy and data review. Customer commitments, data maps, vendor list, and incident history.

- Cross-border assessment. Founder residency, entity structure, beneficial ownership, and any foreign-control sensitivities.

- Financing strategy. Whether the round needs room for insider participation, angel investors and other early backers, or a future institutional lead.

- Milestone drafting discipline. If funding is tranched, define the milestone like someone may eventually need to enforce it.

The best next step is simple. Treat NVCA model forms as a strategic negotiation framework, not a clerical package. Founders who do that usually close faster, disclose more accurately, and avoid the avoidable fights that consume management attention after the money hits the bank.

By Design Law Firm & Legal Consultancy, PLLC helps Washington startups, founders, and investors turn complex financing documents into practical business decisions. For guidance on venture financings, governance, data privacy, technology transactions, and startup growth issues, visit By Design Law Firm & Legal Consultancy, PLLC. Call us today at (206) 593-1519.