A founder is often closest to a first check right when the company is least prepared to take it. The deck is getting polished. A few angel conversations are warm. Someone asks for the cap table, the stock plan, the contractor agreements, and proof that the code belongs to the company. That's the moment many seed rounds stop feeling like momentum and start feeling like cleanup.

That mismatch sits at the center of funding and seeding. The early conversation is framed as a pitch problem, but the primary issue is usually a records problem. If the company can't show who owns what, who approved what, and whether the business controls its IP, a good term sheet can become an expensive legal repair project. In some deals, it becomes a reason to walk away.

Seed capital has become far more important in the startup ecosystem. The National Science Foundation's global innovation analysis reports that worldwide seed-stage venture capital grew from more than $300 million in 2006 to $5.8 billion in 2016, with a 34% annualized average growth rate, while still accounting for only 4% of total venture investment in 2016. The United States received $3.3 billion, or 58% of the global total, according to the NSF's innovation indicators report. More money reached seed, but that didn't make the process forgiving.

The Hidden Risks in Early Stage Funding

The first legal mistake in early stage fundraising is usually a simple one. A founder thinks a small check deserves small paperwork. It doesn't. Small checks can create large problems when they come from different sources, on different documents, with different expectations.

That's why most practical failures in funding and seeding don't begin with fraud or bad faith. They begin with informality. A friend wires money before subscription documents are signed. An accelerator gets advisory rights no one logs in a central file. A contractor builds the product without an invention assignment. Months later, a lead investor's counsel asks routine diligence questions and finds a company held together by email threads and memory.

Where legal risk actually enters

A recurring gap in startup advice is the distance between “raising money” and “taking money lawfully.” As Antler's discussion of pre-seed funding notes, startup financing now often comes from friends and family, angels, crowdfunding, and accelerators at the same time. That creates fragmented rights and future diligence problems if the documents aren't handled carefully.

Some founders assume this only matters once institutional capital appears. It matters earlier. Securities-law compliance, disclosure discipline, investor qualification, and state and federal filing obligations can all appear before the first priced round. Founders exploring community raises should understand how these issues intersect by reviewing resources on crowdfunding and securities law for Seattle entrepreneurs.

The practical question isn't only where to find capital. It's how to accept capital without creating a defect that gets repriced, renegotiated, or exposed in the next round.

The expensive myths

Three assumptions cause most early damage:

- “We'll paper it later.” Later usually means during diligence, when the advantage passes to the investor and legal fees increase.

- “It's just friends and family money.” Informal investors can still create formal securities and governance issues.

- “A SAFE keeps things simple.” A SAFE can be simple when it's used carefully. A stack of SAFEs with inconsistent caps, side letters, and missing approvals usually isn't.

The founder's job before fundraising is to build a company that can survive inspection. That means the company should be able to answer basic questions quickly, with signed records, clean ownership, and a coherent story from formation through financing.

Laying the Legal Foundation Before You Pitch

Investors don't fund a concept in the abstract. They fund a legal entity with assets, obligations, decision-makers, and records. If those basics are weak, diligence will expose it.

A seed process should be run as an evidence-building exercise because seed financing is selective. One dataset cited by Equidam reports that only 15.4% of startups that raised seed in early 2022 closed a Series A within two years, versus 30.6% for the 2018 cohort, which is why founders need a clean cap table, reconciled records, and a prepared data room before fundraising begins, as discussed in this Equidam analysis of startup funding probability.

Form the right entity and keep it current

Most venture-backed companies are expected to operate through a Delaware C corporation or to convert into one before a priced institutional round. The reason is straightforward. Venture documents, board structure, preferred stock mechanics, and market expectations are built around that format.

If the business is still in an LLC, the company shouldn't assume conversion will be painless. The operating agreement, tax history, member approvals, and IP ownership all need to align before any restructure. Founders operating through an LLC should at least make sure the governance documents are in order, including a written Washington LLC operating agreement, before talking to investors about a later conversion.

Clean up ownership before anyone asks

A cap table should answer four questions immediately:

- Who owns stock today

- What was authorized and when

- What options, SAFEs, or notes are outstanding

- What approvals support each issuance

A spreadsheet is not the problem. An inaccurate spreadsheet is. The company should reconcile every founder issuance, vesting schedule, stock option grant, and convertible instrument against signed documents and board approvals. If there's a mismatch between the spreadsheet and the legal file, the legal file controls until fixed.

Practical rule: If a founder can't hand over the charter, bylaws, stock purchase agreements, board consents, and current cap table in a single diligence folder, the company isn't ready to raise.

Secure IP assignment from everyone who touched the product

Founders often believe they “own” what they built because they paid for it or directed it. That isn't enough. The company needs written assignment agreements from founders, employees, and contractors who created code, designs, content, inventions, or core know-how.

That review should include:

- Founder contributions: Check whether pre-incorporation work was assigned into the company.

- Contractor work product: Confirm the agreement includes present-tense assignment language, not just a promise to assign later.

- Open-source exposure: Track material open-source use and the licenses attached to it.

- University or employer overlap: Verify no prior employer, grant program, or academic institution has a claim.

Build a diligence-proof record set

A serious pre-pitch file usually includes:

| Area | What should be ready |

|---|---|

| Corporate records | Formation documents, bylaws or operating agreement, board and stockholder consents |

| Equity records | Cap table, stock ledger, option plan, grant notices, SAFE or note files |

| IP records | Assignment agreements, trademark filings, contractor IP provisions |

| Commercial records | Customer agreements, pilot terms, vendor contracts, partnership papers |

| Employment records | Offer letters, confidentiality agreements, invention assignment documents |

| Compliance records | Privacy policy, terms of use, any regulated-industry policies that apply |

Founders don't need perfection. They need coherence. A company that can explain every document and fix a narrow issue quickly will usually fare better than a company that keeps improvising under diligence pressure.

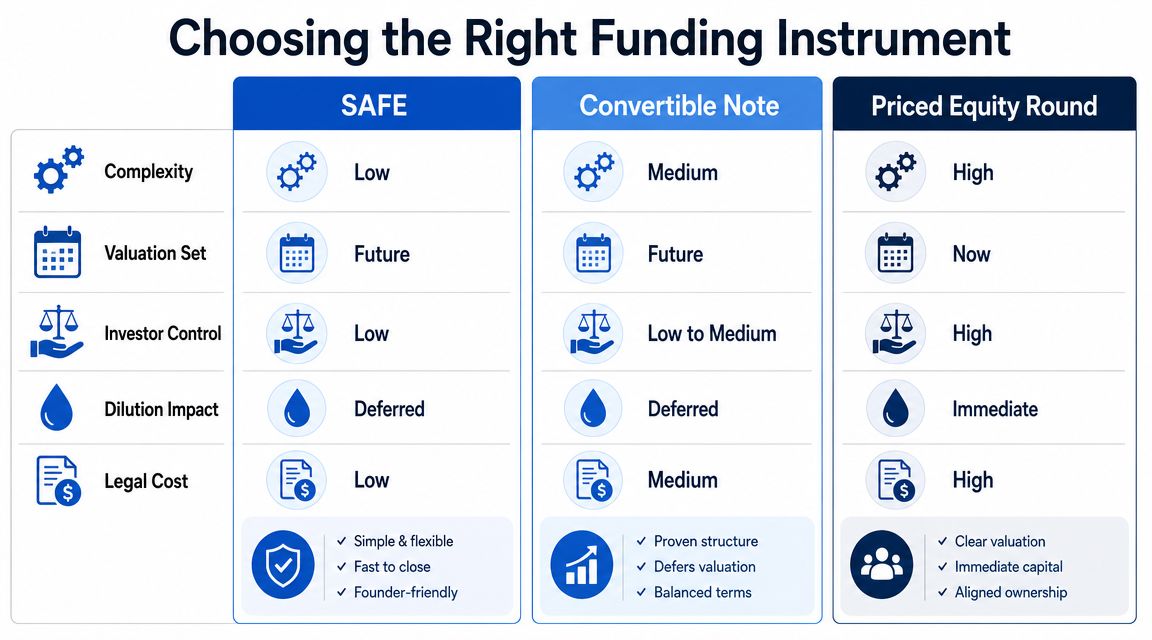

Choosing the Right Funding Instrument

The instrument matters because it shapes dilution, financial capacity, speed, and cleanup cost later. Founders often treat SAFEs, convertible notes, and priced rounds as interchangeable ways to get cash into the bank. They're not.

The better approach is strategic. The company should choose the instrument that matches its stage, investor mix, and ability to maintain discipline after signing. A document that looks founder-friendly on day one can become founder-hostile if the company stacks too many versions of it over time.

SAFE when speed matters and records stay tight

A SAFE works best when the company needs speed and the round is still forming. It avoids setting a present valuation in the same way a priced equity round does, and it usually requires less negotiation at the front end.

The trade-off shows up later. A SAFE doesn't eliminate dilution. It delays the moment when dilution becomes visible. If the company signs multiple SAFEs with different caps, side terms, or most-favored-nation provisions, the next round can become a conversion exercise that surprises everyone, especially the founders.

Use a SAFE when:

- The round is still developing

- Check sizes are relatively small

- The company can track every instrument precisely

- Counsel has modeled conversion outcomes before the next priced round

Convertible note when timing and leverage need boundaries

A convertible note adds debt mechanics. That means maturity dates, interest, and the possibility of pressure if the company doesn't raise a qualifying round in time. For some founders, that added structure can be useful because it creates clearer decision points. For others, it introduces a clock the company doesn't need.

The note isn't necessarily worse than a SAFE. It's just less forgiving if fundraising slows or the next financing takes longer than expected.

Priced round when clarity is worth the cost

A priced equity round is heavier at signing, but clearer after closing. The company issues preferred stock, adopts the related investor rights structure, and sets valuation and ownership immediately. That usually means higher legal cost and more negotiation, but it also means less ambiguity about what investors bought.

Priced rounds can make sense when the company has enough traction, enough capital being raised, or enough investor concentration that doing the full work now is cleaner than deferring it.

Don't default to equity if a weaker option can be avoided

Founders should also question whether equity is the right first move at all. As AccountingDepartment.com's overview of funding options notes, early-stage capital has shifted toward fewer, larger checks, which has made many smaller founders more reliant on grants, revenue-based funding, accelerators, and customer prepayments. The key legal and strategic question is whether equity now makes the company weaker later.

A simple decision frame helps:

| Instrument | Best use case | Main legal concern |

|---|---|---|

| SAFE | Early fundraising, speed, light negotiation | Hidden future dilution if stacked carelessly |

| Convertible note | Early fundraising with debt-style discipline | Maturity and repayment pressure |

| Priced round | Larger or more organized seed financing | Higher upfront cost and governance complexity |

| Non-dilutive funding | IP-heavy, regulated, or slower-revenue businesses | Program restrictions, reporting, and use-of-funds compliance |

The wrong instrument usually isn't wrong because of the document itself. It's wrong because it doesn't match the company's operating reality.

Decoding the Term Sheet What Really Matters

A founder can lose control at a “great” valuation. That happens when attention stays fixed on the headline number and drifts past the terms that govern downside, voting, and future advantage.

Start with economics, not excitement

The first pass on a term sheet should focus on what the investor gets in a mediocre outcome, not only in a big win. That means reading the liquidation preference before celebrating the valuation.

A standard 1x non-participating preference usually means the investor gets its money back first or converts into common if that produces a better result. The term becomes more founder-unfriendly when the preferred stock participates after receiving the preference, or when the multiple exceeds the original investment amount.

Control often hides in protective provisions

The next review should move to veto rights. Investors commonly ask for approval rights over major actions such as creating a new class of stock, selling the company, or taking on major debt. That can be reasonable. The problem appears when the list expands into routine operations and turns a financing partner into a day-to-day gatekeeper.

Founders should review whether the term sheet gives investors effective control over:

- Future financings

- Budget-level borrowing

- Executive hiring or firing

- Changes to option pools

- Commercial decisions that should remain management issues

A good term sheet aligns governance with risk. A bad one gives one investor a standing invitation to renegotiate every operational choice.

The safest term sheet isn't the highest one. It's the one the company can live with through a hard year, a flat year, or a financing delay.

Board seats and pro rata rights deserve a separate read

Board composition affects more than meeting schedules. A board seat creates fiduciary duties, information access, and a real role in company decisions. A board observer can also matter, especially if confidentiality lines are weak or the investor is highly active. At seed, founders should ask whether the company benefits from a board member now or whether a lighter governance structure fits better.

Pro rata rights look harmless because they concern future participation, not current control. But broad pro rata rights can constrain later round construction if too much future allocation is already spoken for. The issue becomes sharper when one investor negotiates super pro rata rights that go beyond its current ownership.

A related contract mindset appears outside financing documents too. Founders reviewing investor documents often benefit from understanding broader allocation-of-risk concepts such as indemnity clauses in Washington State contracts, because the same discipline applies: identify who bears the risk, when, and under what trigger.

A short explainer can help founders hear these issues in plain English before negotiations intensify:

Terms worth pushing on first

A founder doesn't need to fight every point. The points worth immediate attention are usually:

- Liquidation preference structure

- Board seat and observer rights

- Protective provisions

- Option pool treatment in pre-money math

- Pro rata scope

- Founder vesting resets or expansions

The term sheet is where bargaining power is highest before definitive documents start absorbing time and fees. Once the company begins drafting long-form agreements, “market” starts getting used to justify terms that should have been narrowed at the outset.

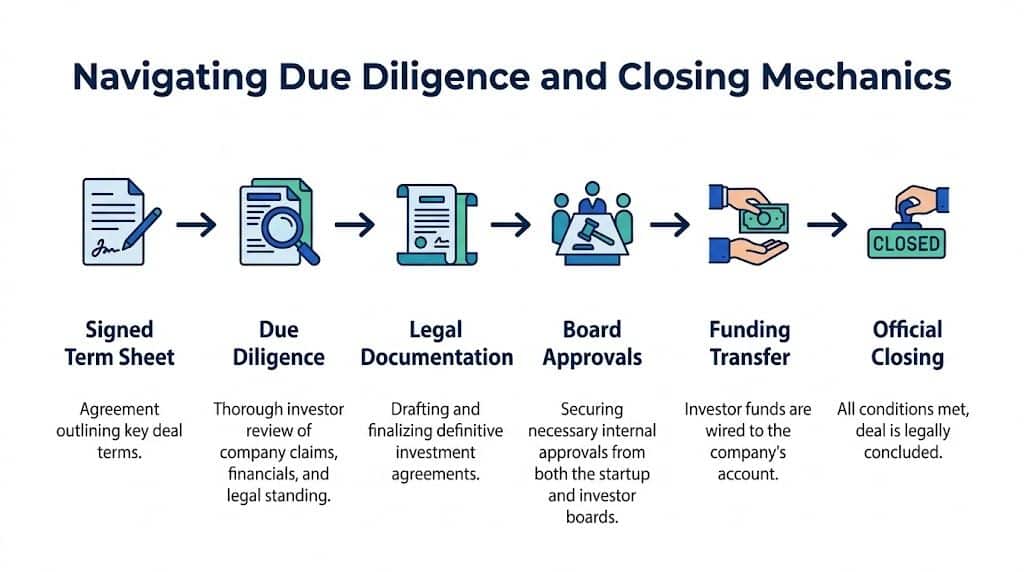

Navigating Due Diligence and Closing Mechanics

A signed term sheet is not cash. It is permission for lawyers, investors, and finance teams to begin verifying that the company is what the pitch said it was.

Founders should budget for the process accordingly. Altoira's guidance on seed rounds recommends planning from the operating plan backward, budgeting for 18 to 24 months of runway, and recognizing that seed fundraising often takes 3 to 6 months. It also warns that common failures include underestimating the duration, failing to model dilution from stacked SAFEs, and not keeping investor updates current, as discussed in this seed fundraising best-practice guide from Altoira.

What belongs in the data room

A credible data room is organized by subject, current, and internally consistent. It should not force investors to ask the same ownership or approval question twice.

Core folders usually include:

- Corporate documents: Certificate of incorporation, bylaws, amendments, board and stockholder consents, good standing records

- Capitalization records: Stock ledger, cap table, option plan, grant agreements, SAFE and note files

- Finance materials: Historical financials, budget, runway model, debt schedules, tax filings if available

- Commercial contracts: Customer agreements, pilots, reseller arrangements, material vendor contracts

- Employment records: Founder agreements, offer letters, confidentiality and invention assignment agreements, contractor files

- Regulatory and privacy materials: Website terms, privacy policy, regulated-industry compliance files where applicable

- IP materials: Trademark records, patent filings if any, assignment agreements, open-source policy or code audit notes

If the product is the company's value, IP records deserve extra care. Founders that haven't yet systematized this work should address intellectual property protection basics before diligence begins, not after investor counsel flags missing assignments.

Reconcile before investor counsel does

The most common diligence failure isn't that a document is missing. It's that several documents tell different stories. The cap table doesn't match the board consent. A contractor agreement names the wrong entity. A founder claims vesting started on one date while the stock purchase agreement uses another.

A pre-diligence reconciliation should test:

| Issue | What to verify |

|---|---|

| Equity consistency | Cap table matches stock ledger, SAFEs, notes, and board approvals |

| Signature completeness | All material contracts are fully executed by the right parties |

| Entity consistency | The same legal entity appears across bank, contract, and tax records |

| IP chain of title | Every creator assigned rights into the company |

| Disclosure alignment | Pitch claims match financial records and customer documentation |

Closing mindset: Diligence is less about having polished files than having files that agree with each other.

Don’t ignore securities compliance on the way to close

Closing mechanics also require securities-law discipline. The exact path depends on the exemption being used and the structure of the offering, but the company should expect to coordinate subscription paperwork, investor representations, board approvals, and post-closing filings. Founders who use a platform, crowdfunding route, or mixed investor base should be especially careful, because accredited and unaccredited participation can change the compliance posture materially.

The practical legal sequence usually looks like this:

- Confirm the financing exemption and investor eligibility

- Finalize definitive documents

- Obtain company approvals

- Collect executed signature packets and investor representations

- Receive funds into the correct company account

- Issue the security and update the cap table

- Complete required post-closing notices and filings

Closing delays often come from one of three places: investor signatures, unresolved diligence items, or corporate approvals that should have been prepared earlier. All three are manageable if the company treats closing as an operations process, not just a legal event.

After the Close Post-Funding Governance and Milestones

The round closes. The company account is funded. The legal work is not over. It has shifted from transaction mode to governance mode.

That shift matters because seed money is bridge capital, not permanent safety. UNESCO describes seed funding as financing used to transform early ideas or prototypes into products or services, and current market summaries report a median seed round size of $3.5 million in 2024, with 52% of pre-seed and seed-stage companies raising between $1 million and $4 million, according to this UNESCO seed funding overview. That money is supposed to move the company from concept toward commercialization. It has to buy proof.

Governance is part of execution

Post-close governance works when it is disciplined but not theatrical. The company should calendar board meetings, circulate materials in advance, maintain written minutes or consents, and track reserved matters that require approval. Those habits don’t exist to satisfy formality. They create clean decision trails for the next financing, strategic partnership, or acquisition review.

A board packet at seed doesn’t need to be elaborate. It does need to be consistent. Most useful packs cover cash position, hiring, product milestones, major commercial developments, legal risks, and decisions requiring board input.

Investor updates are leverage, not courtesy

The strongest post-funding habit is a regular investor update. A short monthly or periodic note can do more for the next round than a polished emergency memo sent when cash gets tight.

Useful updates usually include:

- What changed: Product, customers, hiring, or partnerships

- What missed: Milestones that slipped and why

- Where help is needed: Introductions, recruiting, channel access, regulatory expertise

- What management is watching: Burn, concentration risk, legal exposure, technical blockers

A disciplined update style changes the investor relationship. It gives investors a concrete way to help, documents execution, and reduces surprise. It also creates a historical record that helps support future diligence.

Good governance shortens the distance between this round and the next one because it turns company history into organized evidence.

Milestones should be legal as well as commercial

Founders often define progress only in product and revenue terms. The better view is broader. If the company needs enterprise customers, privacy terms and contract process matter. If it operates in a regulated space, compliance milestones matter. If the business depends on proprietary technology, patent strategy, trade secret controls, and IP assignment hygiene matter.

The companies that raise efficiently later are often the ones that treated governance as a build function from the start, not as post-close paperwork.

Founders preparing for funding and seeding often need more than form documents. They need coordinated legal guidance on entity structure, securities compliance, cap table hygiene, commercial contracts, privacy, and IP ownership before diligence starts. By Design Law Firm & Legal Consultancy, PLLC advises startups and growth-stage businesses in Washington on those issues, including formation, governance, fundraising-related legal cleanup, technology contracts, and risk management. Contact our law offices today at (206) 593-1519.