A founder closes a few pilot customers, hires the first real team, and finally sees momentum. Then the bank balance starts to tighten. Payroll, product work, and customer delivery can't wait, but setting a clean valuation still feels premature. If the company prices the round too low, the founders may give away too much ownership. If it prices too high, serious investors may walk.

That tension is where many early financings begin. A convertible note often looks like the practical answer because it lets the company raise money now and push the valuation fight into a later round, when there is more traction, better data, and a clearer story for institutional investors.

That sounds simple. It isn't always simple in practice. A note can be fast, flexible, and founder-friendly when the terms match the company's stage. It can also become a balance-sheet problem, a cap table problem, or a maturity problem if the startup misses the next financing window. Founders who are comparing options such as angels, venture capital, and other early funding paths often benefit from grounding that decision in broader fundraising strategy first, which is why Fundl on getting startup capital is a useful starting point before papering any deal.

The Founder's Dilemma Funding Early Growth

A common seed-stage fact pattern looks like this. The startup has enough traction to persuade insiders, angels, or a small syndicate that the business is moving. But the company does not yet have the metrics, revenue history, or a strong bargaining position for a confident priced round.

In that setting, a note works as a bridge. The investor wires money now. The company issues a legal instrument that starts as debt and is supposed to become equity later. The hard valuation discussion gets deferred until a later financing, when the startup can support the number with more than a product demo and a few encouraging customer calls.

That's one reason founders often first encounter notes through angel discussions rather than institutional term sheets. Investor expectations also matter, and founders who are lining up an angel syndicate should understand how those participants typically evaluate early risk, control, and conversion economics through resources like angel investor guidance for startups.

Smooth fundraising documents don't rescue a weak financing plan. They only document it more efficiently.

The practical appeal is obvious. A note can get money into the company without forcing everyone to pretend that an early valuation is precise. The practical danger is less obvious. The note is still a contract, and every shortcut taken in the first conversation usually shows up later as an advantage for someone else.

Why founders reach for notes

Three motivations usually drive the decision:

- Speed matters: founders need payroll runway and product progress more than they need a prolonged pricing debate.

- Valuation is fuzzy: the company may have signs of traction, but not enough to defend a fully priced seed round.

- The next milestone is visible: management believes the business can reach a stronger financing position with additional time and capital.

That combination makes a note attractive. It does not make it harmless.

What Exactly Is a Convertible Note

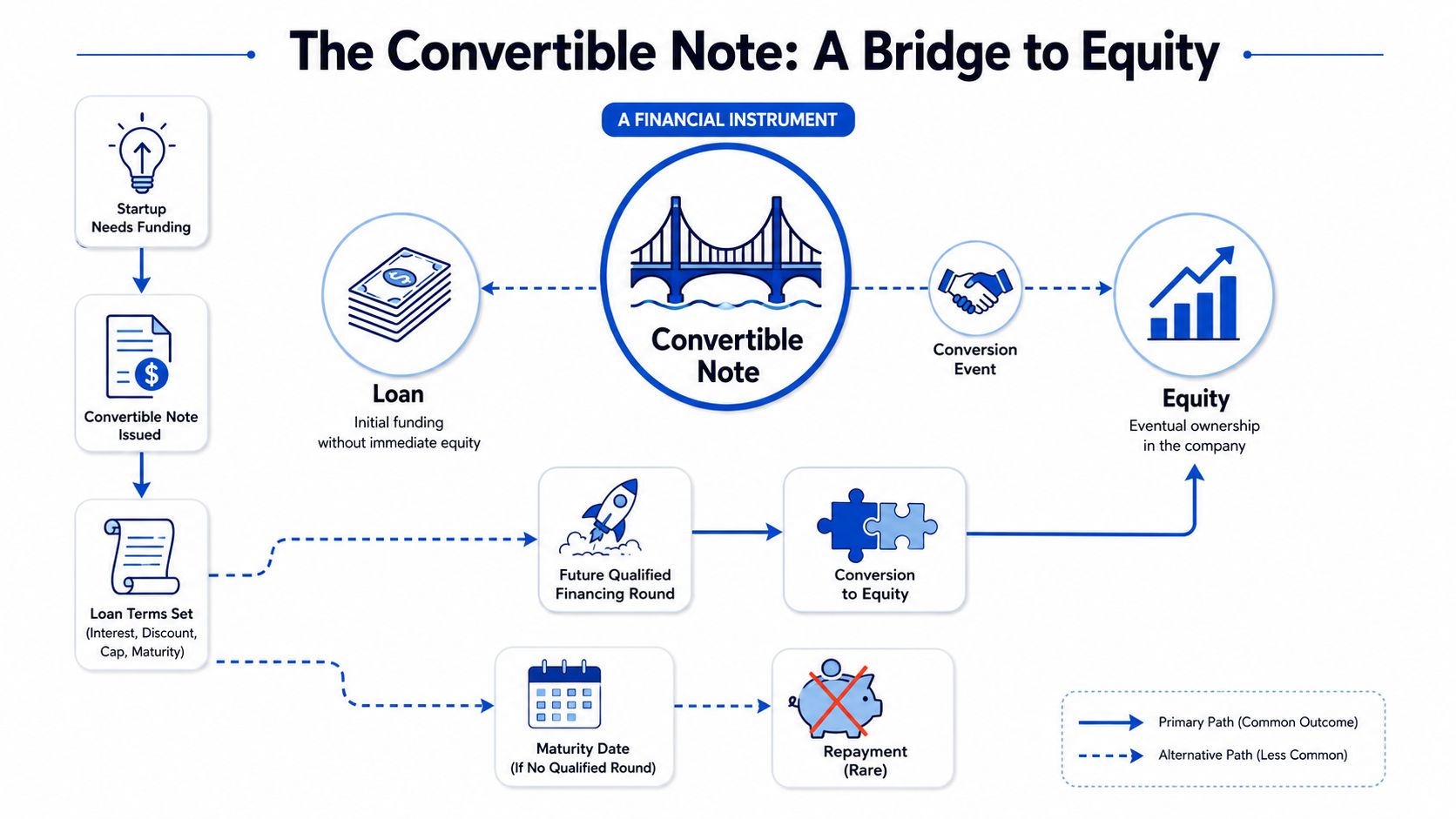

A convertible note is a short-term debt instrument designed to convert into company equity later rather than be repaid in cash in the ordinary course. It begins life as a loan. It is carried as debt. Then a later event, usually a qualified financing round, triggers conversion into shares.

AngelList's overview of convertible notes describes the structure as short-term debt with a typical interest rate of 4 to 8 percent per annum and a maturity date of 18 to 36 months. It also notes that, upon a qualifying equity financing that is often defined as raising $250,000 or more, the outstanding principal plus accrued interest typically converts into equity shares, often at a 20 percent discount to the next round's price.

Debt first, equity later

That hybrid character is the whole point. The startup gets financing now without immediately issuing priced preferred stock. The investor gets contractual protections that pure equity might not provide at that moment, including debt status before conversion, interest accrual, and a maturity date.

For a first-time founder, the simplest working description is this: a note is a loan built to become ownership if the company reaches the next real financing event.

That distinction matters because founders sometimes treat notes as informal placeholders. They are not placeholders. They are legal obligations with conversion math attached.

Why notes still matter after SAFEs

Historically, notes dominated early startup financing. Startups.com's explanation of convertible notes states that convertible notes were the dominant pre-seed and seed financing instrument from approximately 2005 until 2013, when Y Combinator introduced the SAFE (Simple Agreement for Future Equity), which lacks debt characteristics like interest and maturity dates, leading to a gradual market shift toward SAFEs.

That history explains today's market. SAFEs are common because they strip away the debt features many founders dislike. Notes remain relevant because those debt features are exactly what some investors want, especially in bridge situations or when the company's next financing path is less certain.

A founder should not ask whether a note is popular. The better question is whether debt features help or hurt this company in this round.

For startups using a note as part of a broader financing plan, clean documentation and clear ownership forecasting matter early. That is especially true once multiple investors, side letters, and follow-on rights enter the mix.

The Core Mechanics of a Convertible Note

The economics of a note are driven by four terms. Founders usually spend most of their energy on the cap and discount. The legal risk often sits elsewhere, especially in the maturity language and the remedies that apply if the company has not raised a priced round on time.

Interest rate

A convertible note accrues interest while it remains outstanding debt. In many deals, the company does not make cash interest payments before conversion. The accrued amount is added to principal and converts into equity with the rest of the note.

Waveup's summary of convertible notes notes that these instruments commonly include interest and a defined maturity period, with accrued interest converting along with principal.

The practical point is straightforward. Interest increases the number of dollars converting into stock. If the note stays outstanding longer than expected, the increase is larger. That matters most when the company is already managing a tight option pool or several overlapping convertible instruments.

Maturity date

The maturity date is the term that can turn a bridge financing into a pressure point.

If the company has not completed a qualifying financing by that date, the note does not wait politely in the background. The document will say what happens next. Sometimes the investor can demand repayment. Sometimes the note extends only with investor consent. Sometimes conversion is forced on a formula that founders barely reviewed when signing.

That risk is easy to underestimate in an optimistic fundraise. It becomes very real when the market slows, a lead investor drops out, or the round comes together six months later than planned.

For Washington startups, this deserves a close legal read. A note is debt under state law and under the contract the company signed. If repayment is not realistic, the company usually needs an amendment, an extension, or a negotiated conversion before maturity becomes a live default issue. Founders should review not only the date, but also default interest, investor approval thresholds, and whether one holder can act alone or a majority of holders controls the outcome.

Discount

The discount gives the noteholder a lower conversion price than the new money investors pay in the next priced round. That lower price buys more shares for the same invested amount, which is how the note rewards early risk.

The founder mistake here is usually not misunderstanding the concept. It is failing to model the effect across all outstanding notes, SAFEs, and option pool changes. A discount that seems manageable in isolation can produce a very different ownership result once several instruments convert at the same closing.

A founder working through dilution scenarios should model these outcomes in advance, especially where multiple notes or SAFEs are already outstanding. Accurate capitalization table management for startups turns a note from a rough assumption into a decision you can price.

Here's a useful explainer that shows the concepts visually:

Valuation cap

The valuation cap sets a ceiling on the company valuation used for conversion. If the next priced round values the company above that cap, the investor converts as if the valuation were lower. That usually means more shares for the noteholder and more dilution for founders and existing stockholders.

This cap example on YouTube explains the basic mechanic. If the priced round valuation is above the cap, the capped price controls.

In most note documents, the investor gets the better of the discount price or the cap price. Founders should negotiate the cap with the same care they would use in a priced round because the cap is deferred pricing. A cap that looks harmless when cash is short can become the term everyone regrets when the equity round finally closes.

How a Convertible Note Converts Into Equity a Worked Example

A founder signs a $250,000 note to get through product development, then closes a priced round a year later and learns the note converts into far more stock than expected. That result usually comes from one place. Nobody modeled the conversion before signing the note.

The conversion math is not complicated, but the details drive dilution. Price per share, accrued interest, the cap table definition, and whether the investor gets the discount or the cap can all change the outcome.

Scenario one using the discount

Start with a simple case. The company issues a note with a 20 percent discount and later closes a qualified financing at $1.00 per share.

The noteholder does not pay $1.00 per share. The note converts at $0.80 per share. In practical terms, the note investor gets more shares for the same dollars than the new cash investor in the round.

That difference shows up immediately on the cap table. If the note principal is large, or if several notes convert at once, founder dilution can jump more than expected.

Scenario two using the cap

Now add a valuation cap. Assume the cap produces a conversion price lower than $0.80 per share. In most note documents, the investor converts at that lower price because the investor gets the more favorable term.

Founders often miss the effect of that clause because the cap looks abstract when the company is raising a small bridge round. It is not abstract at conversion. It is deferred pricing, and it can produce a share count that feels out of step with the size of the original check.

For Washington startups, this is also where clean drafting matters. I often see early notes borrowed from another state, then layered onto a Delaware C corporation with Washington founders and operations. The conversion formula may still work, but sloppy definitions of "Company Capitalization," "Qualified Financing," or interest treatment can create disputes at the exact closing where the company needs speed and certainty.

A simple worked example

Assume:

- Note principal: $250,000

- Accrued interest converting with the note: $10,000

- New round price: $1.00 per share

- Note discount: 20 percent

- Valuation cap formula implies a $0.65 conversion price

Total amount converting is $260,000.

If the discount applies, the note converts at $0.80 per share, producing 325,000 shares.

If the cap applies, the note converts at $0.65 per share, producing 400,000 shares.

That 75,000 share difference matters. It affects founder ownership, the new investor's percentage, and often the size of the option pool the lead investor expects the company to refresh at closing.

What changes after conversion

A note conversion changes legal status as well as economics:

- Founders and common stockholders: own a smaller percentage after the new shares are issued.

- The note investor: stops being a creditor and becomes an equity holder.

- New investors: usually buy preferred stock in the financing round, with rights that sit above common stock in several important respects.

Table: Cap Table Impact of Convertible Note Conversion

| Stakeholder | Pre-Conversion % Ownership | Post-Conversion % Ownership |

|---|---|---|

| Founders and existing common holders | Higher | Lower |

| Convertible note holder | 0 as equity holder | Gains equity on conversion |

| New preferred investors | 0 before round | Gains negotiated preferred ownership |

The table stays qualitative because the actual percentages depend on the note amount, interest, the conversion formula, option pool treatment, and the capitalization definition in the financing documents.

Founders should ask for one thing before signing a note. A written conversion model that shows the discount case, the cap case, and the fully diluted ownership result after the priced round closes. Without that model, the note remains "simple" only until the closing checklist arrives.

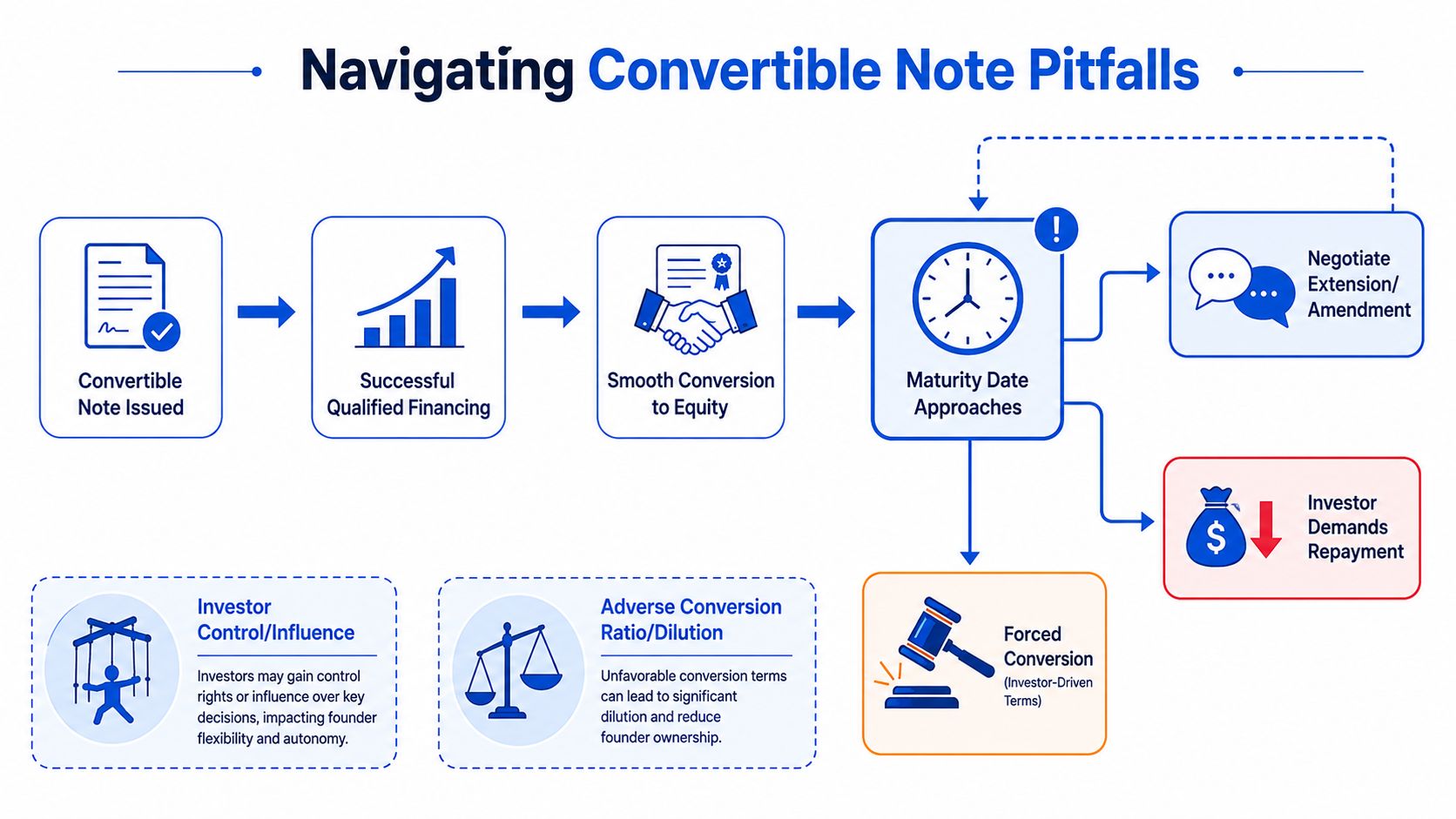

The Maturity Date Trap and Other Hidden Risks

Most explainers stop at the happy path. The startup raises a strong next round, the note converts smoothly, and everyone congratulates themselves for keeping the early financing simple.

That is not the only path.

When the bridge ends before the next round

Kruze Consulting's discussion of convertible note risks warns about the Maturity Date Trap. If the startup fails to raise a priced round before maturity, the note can function as a hard debt obligation requiring repayment of principal plus interest, potentially forcing insolvency or a fire-sale liquidation. The same source also notes that standard templates often lack effective extension negotiation clauses.

That issue matters more in slower fundraising markets. A company may still be viable, still shipping product, and still attracting customer interest, yet fail to close the next round before the note matures. Once that happens, the investor's incentives can diverge sharply from the founder's.

When a note matures in a weak market, the legal document starts to matter more than the optimism that originally got the deal signed.

Other risks founders overlook

Maturity is the sharpest edge, but it is not the only one.

- Stacked note risk: multiple notes from different dates can create inconsistent discounts, caps, and side rights that complicate the next financing.

- Control drift: information rights, consent rights, or informal investor influence can expand if the company needs amendments near maturity.

- Adverse conversion outcomes: a low cap agreed early can produce much heavier dilution than management expected when the next round finally closes.

- Change-of-control pressure: if the company is sold before a standard equity financing, the payout or conversion mechanics may not align with founder expectations.

What works better in note drafting

Founders reduce risk when they negotiate the downside path with the same seriousness they give the upside path.

Useful protections often include:

- Clear extension mechanics: the note should say how maturity can be extended and who must approve it.

- Defined maturity outcomes: the parties should not leave post-maturity treatment to improvisation.

- Conversion clarity on a sale: acquisition treatment should be explicit.

- Consistency across notes: later closings should not create a patchwork of incompatible terms.

If the company cannot explain what happens on the bad day, it is not ready to sign on the good day.

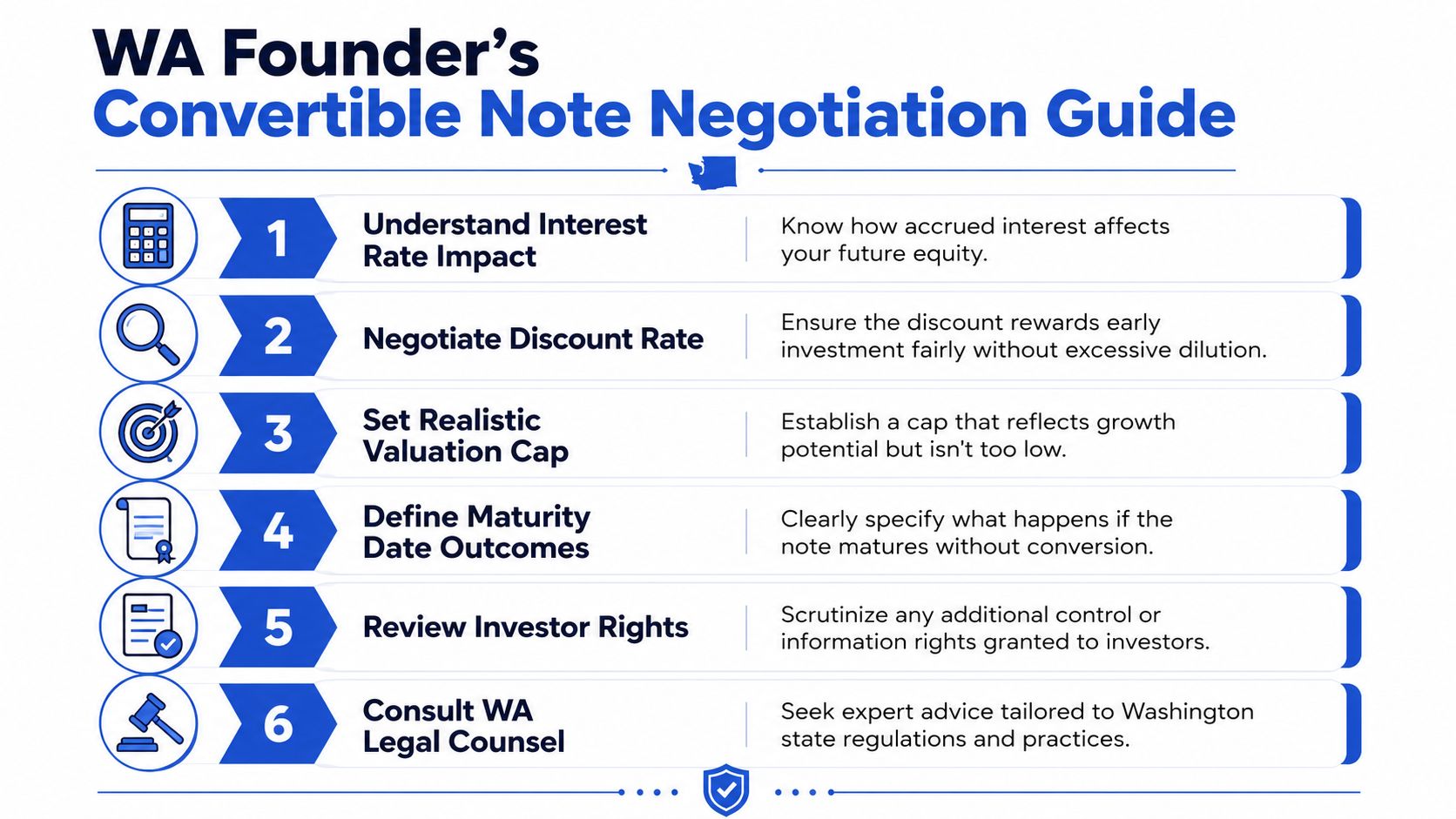

A Washington State Founder's Negotiation Checklist

Washington startups often use notes in a specific slice of the market rather than as a universal funding tool. Pipeline Road's Washington-focused glossary states that in Seattle and Washington State startup markets, convertible notes are technically optimized for the seed-bridge stage, post-pre-seed and pre-Series A, to secure 12 to 24 months of runway while valuation discussions are deferred until the company has stronger traction data.

That framing is useful because it narrows the question. A Washington founder should not ask whether a note is good in the abstract. The better question is whether the company is in a seed-bridge moment.

The checklist that actually matters

A disciplined founder should review the note in this order.

Maturity outcome first

Start with the unpleasant scenario. If the company does not raise the next priced round on time, what happens? Extension, repayment, optional conversion, or investor election should not be left vague.Valuation cap second

The cap is deferred pricing. If it is too low, the bridge financing may become expensive equity in disguise.Discount after the cap

The discount should reward early risk, but the founder needs to understand whether it will ever matter if the cap is expected to control.Interest in context

Interest may seem minor, but it adds to the amount converting into shares. It belongs in the full dilution model, not in a footnote.Investor rights review

Pro rata rights, information rights, and any consent language should be read alongside the economics. A founder can accept a fair price and still over-grant control.Change-of-control language

If the startup is acquired before the note converts in a standard financing, the agreement should clearly define the investor's treatment.

Washington-specific practical habits

Founders in the Seattle and Greater Puget Sound ecosystem usually benefit from stronger process discipline than the earliest friends-and-family round often receives.

A clean pre-signing package should include:

- A modeled cap table: no one should sign before seeing likely ownership outcomes.

- A document set with consistent terms: avoid mixing forms and side promises casually.

- A diligence checklist: basic financial and legal housekeeping reduces amendment fights later. For founders who need a practical operational prompt, HireAccountants' pragmatic checklist is a useful companion to legal review.

- A market-standard drafting baseline: starting from recognized forms can reduce avoidable friction, and founders should understand the role of NVCA model forms in venture financings.

A founder gains leverage by being organized before negotiation starts, not by sounding tough after the draft arrives.

Next Steps Is a Note Your Best Option

A note is often the right tool when the company needs speed, the valuation is still hard to defend, and the round is a bridge to a nearer priced financing. It is often the wrong tool when the business cannot realistically predict its next financing window or when the founders are already worried about maturity before the documents are signed.

A SAFE may be a better fit when the company wants valuation deferral without debt features. A priced seed round may be better when the startup has enough traction, investor interest, and negotiating clarity to set terms now and remove conversion uncertainty later. The right answer depends less on trend and more on timing, bargaining power, and downside tolerance.

Founders who need help assessing financing paths beyond a single instrument can also review directories that find financing specialists by category and need. The key is to pressure-test the choice before papering it. A fast document is still a long-term commitment.

A convertible note explained properly is not just a financing shortcut. It is a debt instrument with equity upside, a legal timetable, and a built-in negotiation over what happens if the company's next round arrives late. Founders who understand that point early usually make better deals.

By Design Law Firm & Legal Consultancy, PLLC helps Washington founders structure financings with clear documents, realistic risk allocation, and practical guidance that fits the company's stage. Startups that need experienced counsel on convertible notes, seed rounds, governance, and growth-stage legal planning can learn more at By Design Law Firm & Legal Consultancy, PLLC.