A founder receives a first venture term sheet and sees familiar words used in unfamiliar ways. Stock. Preference. Conversion. Protective provisions. The document looks short, but its economics and control terms can shape the company for years.

That's why what is preferred stock isn't a beginner's side question. For a startup, it's one of the central legal and financial concepts in the financing itself. The investor usually isn't buying the same security held by founders and employees. The investor is buying a customized class of shares with negotiated rights that affect payouts, governance, and influence in the next round.

What Is Preferred Stock An Introduction for Founders

Preferred stock matters most when a company is about to take outside money. Founders often hold common stock. Investors usually ask for something else because they want ownership upside, but they also want built-in protections if the company underperforms, restructures, or sells for less than expected.

Legally and economically, preferred stock sits between straight equity and debt. VanEck describes preferred stock as a hybrid security that blends equity and debt features. It usually pays a fixed dividend, ranks ahead of common stock in dividend payments and liquidation, often has limited or no voting rights, and is generally senior to common stock but subordinate to bonds in the capital structure, as explained in VanEck's overview of preferred stock.

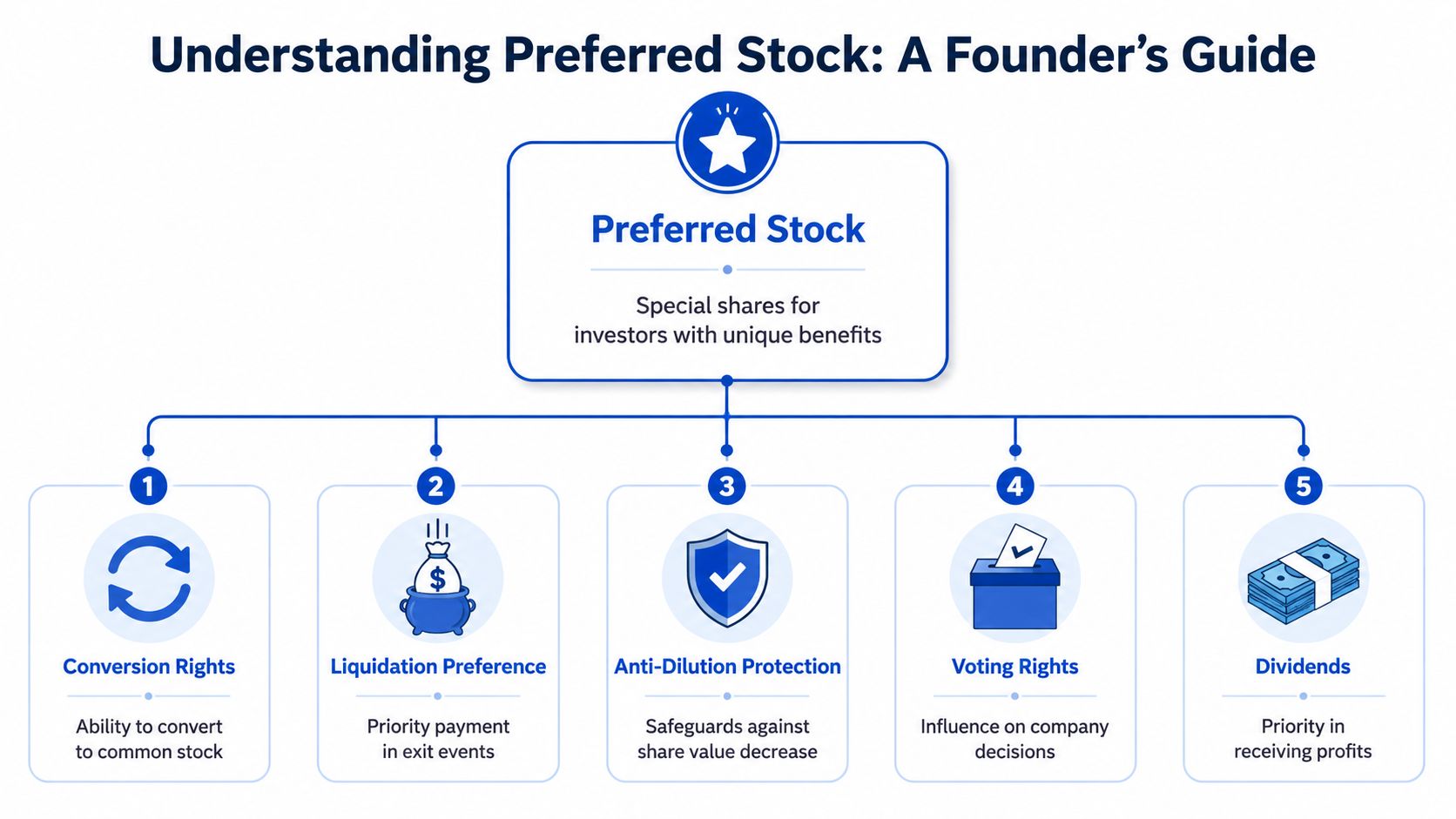

For a founder, that definition becomes practical fast. Preferred stock usually means investors negotiate rights tied to five pressure points:

- Downside protection: priority if the company is sold or wound down

- Control: consent rights over major decisions

- Dilution: mechanisms that respond to future down rounds

- Optionality: conversion into common when that produces a better outcome

- Return structure: dividend and participation mechanics that change the economics of an exit

Preferred stock isn't just “better stock.” It's a contract layer placed on top of equity.

In Washington startup financings, these terms sit alongside securities compliance and offering rules. Founders raising from a crowd, angels, or a lead investor should understand how the financing path affects the legal paperwork and disclosures, especially where exempt offerings are involved, as discussed in this overview of crowdfunding and securities law for Seattle entrepreneurs.

Preferred Stock vs Common Stock Key Differences

Founders and employees usually own common stock. Investors usually buy preferred stock. That split exists because the parties are taking different risks and bargaining for different rights.

Common stock is the purest form of ownership. It usually carries the residual upside if the company becomes highly valuable, but it also sits at the bottom of the payout stack. If the company exits modestly, common can end up with very little after senior claims are paid.

Preferred stock is structured differently. In major markets, it has historically functioned more as an income-oriented instrument than a growth asset. S&P Global notes that preferred stocks have historically offered higher yields than common stocks, have lower claim priority than bondholders, and are typically less volatile than common stocks, according to S&P Global's research on the U.S. preferred market. In venture deals, that same instinct shows up through negotiated protections rather than through retail-style yield investing.

Common Stock vs Preferred Stock

| Feature | Common Stock (Founders/Employees) | Preferred Stock (Investors) |

|---|---|---|

| Primary role | Pure ownership and upside participation | Ownership plus negotiated downside protections |

| Liquidation priority | Paid after preferred and creditors | Paid before common, but behind debt |

| Dividends | Usually discretionary and often nonexistent in startups | May include dividend rights and priority features |

| Voting | Often standard voting rights | May have class voting or separate approval rights |

| Conversion | Not typically relevant | Often convertible into common |

| Anti-dilution | Rarely included | Commonly negotiated in venture deals |

| Risk profile | Highest risk, highest residual upside | Reduced downside risk, but often with capped or structured upside in some scenarios |

Why founders should care

The legal difference becomes an economic difference when things don't go according to plan.

If the company has a large exit, preferred holders often convert to common and share in the upside. If the company has a modest exit, preferred holders may rely on their negotiated preference instead. That means the same headline valuation can produce very different founder outcomes depending on the security design.

A founder who treats preferred stock as “just investor shares” usually misses three practical realities:

- Control terms can outlast the round.

- Preference stacks can distort exit incentives.

- The next investor will read the old preferred terms before wiring new money.

A clean cap table isn't just about who owns what. It's about what rights each class can enforce.

Decoding Core Preferred Stock Rights

A preferred share isn't one right. It's a bundle. The problem for founders is that term sheets often compress that bundle into a few short clauses, making aggressive language look ordinary.

Liquidation preference

Liquidation preference answers one question first. Who gets paid before the common holders in a sale, merger, dissolution, or similar event?

Founders should think of this as a waterfall. Money comes in at the top, and the legal terms determine who catches it first. Preferred holders usually get their negotiated priority before common stock shares in the remainder.

This is the term that can make a respectable acquisition feel disappointing to the common holders. A founder may focus on valuation. Counsel usually focuses on payout order.

Dividends

Preferred stock often includes dividend language, but startup founders shouldn't assume that means regular cash checks are going out. In many venture deals, dividends exist more as a legal and economic preference than as an operating reality.

Fidelity explains that preferred stock behaves like equity legally, but is designed economically to produce bond-like income through a fixed dividend tied to par value. Fidelity also notes that par in U.S. retail issues is often $25, while institutional issues often use $1,000 par, and that this fixed structure makes valuation highly sensitive to interest rates, as described in Fidelity's preferred stock explainer.

For a private company, the more important founder question is simpler. Is the dividend cumulative, accruing over time, or mostly dormant unless there's an exit or specific trigger?

Conversion rights

Conversion rights let investors swap preferred into common. That usually matters when the common payout becomes more attractive than taking the preference.

In plain terms, investors want the better of the two doors. They can keep the protections of preferred when the downside case dominates. They can convert when the upside case makes common more valuable.

That flexibility is one reason preferred stock is standard in venture financings. It gives investors a way to preserve downside protections early while still participating in major upside later.

Anti-dilution provisions

Anti-dilution terms matter when the company raises money later at a lower price. Founders often learn this only after a rough financing environment turns a theoretical clause into a live issue.

There are several forms, but the core purpose is the same. The clause adjusts economics in favor of existing preferred holders if later investors buy in at a lower valuation. That can materially shift dilution onto founders, employees, and other common holders.

Voting and protective provisions

Some preferred rights don't show up in ownership percentages. They show up in consent requirements.

A founder may still hold significant common equity and still be unable to complete key actions without preferred approval. That can include selling the company, changing the charter, authorizing new shares, taking on debt, or changing board structure.

Practical rule: The most dangerous preferred term is often the one that doesn't change valuation at signing but changes decision-making later.

When disputes arise over suspended dividends, seniority, or rights tied to a preferred issue, founders and investors sometimes need a sharper understanding of enforcement and damage theories. For readers dealing with a contested situation rather than a clean financing, this discussion of investment loss recovery for preferred stock gives useful context on the kinds of issues that can surface after the deal documents are signed.

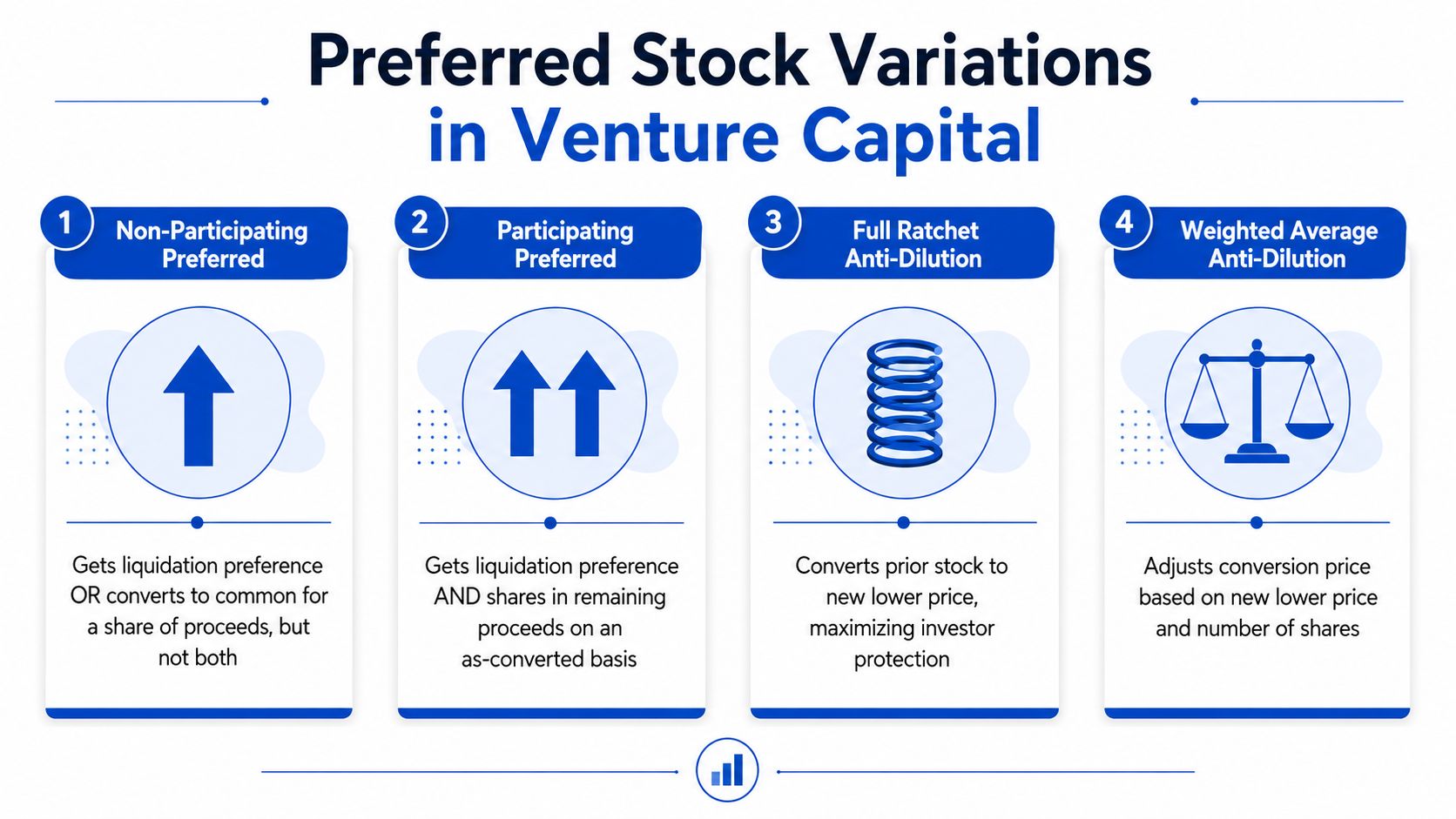

Common Types of Preferred Stock in Venture Deals

The label “preferred stock” sounds singular. It isn't. Venture financings use multiple variants, and the variant matters because small wording changes can reallocate large portions of exit proceeds and future control.

Participating and non-participating preferred

Non-participating preferred usually gives the investor a choice. Take the preference, or convert into common and take the common share of proceeds.

Participating preferred changes that. The investor first receives the liquidation preference and then also shares in remaining proceeds on an as-converted basis. Founders often call that a double dip because, economically, it can produce exactly that effect.

Many founder-friendly headline terms often stop being founder-friendly. A financing can look ordinary on valuation and board structure but become expensive through participation mechanics.

Cumulative and non-cumulative dividends

The dividend protection profile is a major distinction. With cumulative preferreds, skipped dividends accumulate and must be paid before common shareholders receive dividends. With non-cumulative preferreds, missed payments are forfeited. Many issues also include call features, allowing redemption at par after a specified date, as summarized in this explanation of preferred stock features and dividend protection.

For startups, cumulative dividends can gradually increase the economic weight of a preferred round over time, even when no one expects routine dividend payments. Non-cumulative structures are generally lighter from the company's perspective.

A short visual helps separate these variations:

Convertible preferred and anti-dilution style

Most venture preferred is convertible preferred. That gives investors the option to convert into common when the upside case justifies it.

Anti-dilution protection adds another layer. Two patterns appear often in negotiations:

- Full ratchet: highly protective of the investor, often painful for founders in a down round

- Weighted average: still protective, but usually less punitive because it accounts for both price and share count

Founders should model preferred economics under a weak exit, a strong exit, and a down round. If the documents only make sense in the best case, the deal isn't fully understood.

Reading a Term Sheet Sample Preferred Stock Clauses

Founders rarely struggle with the label of a term. They struggle with the sentence that implements it. A short clause can move control, cash, and influence in ways that aren't obvious on a first read.

Liquidation clause

“In the event of any liquidation, dissolution, or deemed liquidation event, the holders of the Series Seed Preferred shall be entitled to receive, prior and in preference to any distribution to holders of Common Stock, an amount per share equal to the original purchase price, plus any declared but unpaid dividends.”

Plain English: the investor gets paid first, before common receives anything. The phrase “deemed liquidation event” deserves attention because it often includes a merger, asset sale, or similar transaction, not just a shutdown.

What to scrutinize:

- Scope of the trigger: Does a sale of substantially all assets count?

- Amount of the preference: Is it only the purchase price, or more than that?

- Dividend add-on: Are unpaid dividends stacking onto the payout?

Participation clause

“After payment of the preference, the remaining proceeds shall be distributed pro rata among the holders of Common Stock and Preferred Stock on an as-converted basis.”

Plain English: the preferred holder may get the preference first and then keep participating with the common. That's the clause that often changes founder economics more than the headline valuation.

Aggressive drafts may also cap participation, while others don't. A cap can soften the effect. No cap can make moderate exits much less attractive to common holders.

Protective provisions clause

“So long as any shares of Preferred Stock remain outstanding, the consent of the holders of a majority of the Preferred Stock shall be required for any amendment to the Charter, creation of any senior or pari passu security, declaration of dividends, redemption of shares, or sale of the Company.”

Plain English: the company can't take major actions without investor approval.

Governance power is vested in this arrangement. A founder negotiating investor participation should also review related guidance on working with angel investors, because many early-stage governance dynamics appear before institutional venture money arrives.

If a clause affects charter amendments, future securities, or a sale process, it isn't boilerplate. It's control language.

What usually works and what doesn't

What works is disciplined reading of definitions, triggers, and approval thresholds. What doesn't is focusing only on valuation, board seats, and option pool size while skipping the payout mechanics in the fine print.

A strong review usually asks:

- What happens in a modest sale?

- What happens in a down round?

- What approvals are needed for the next financing?

- Can one investor block a transaction the board supports?

Strategic Implications for Your Startup

Preferred stock is often described as an investor security. For founders, it's better understood as a long-tail governance system. It influences who can approve what, who gets paid first, and who bears the pain if the next round is harder than expected.

Cornell's legal overview makes the key point cleanly. Preferred stock is not one standard instrument. It is a negotiated contract that can affect control, the liquidation waterfall, and future financing outcomes. Cornell also notes that preferred stock can be less about “better dividends” and more about allocating downside protection and control rights, as explained in Cornell's definition of preferred stock.

Control doesn't only sit on the board

Founders often watch board composition closely and assume that's where control lives. It doesn't stop there. Protective provisions, class votes, and consent rights can create investor vetoes outside ordinary board governance.

Examples include:

- New financing approvals: existing preferred may need to approve a new class or senior security

- M&A decisions: a buyer may be ready, but the preference stack changes who supports the sale

- Operational flexibility: debt, redemptions, charter changes, and option expansions may require investor signoff

Exit math shapes company culture

A financing that heavily protects investors can also affect internal incentives. If employees understand that a modest exit mostly clears preferences, common stock can feel remote rather than motivating.

That doesn't mean preferred stock is bad. It means its economics should match the company's stage, capital structure, and realistic outcomes. The strongest founder negotiations usually focus less on abstract fairness and more on preserving a workable incentive structure for the team.

For founders trying to understand how financing terms reduce their ownership and economic outcomes over time, this explanation of equity dilution is a useful companion topic.

A term that looks harmless in a hot market can become decisive in a flat or down market.

Future rounds read the old documents

Every new investor will review existing charter rights, side letters, and approval thresholds. If the first round contains unusually restrictive provisions, later financings become harder to close because the company must negotiate around old rights before bringing in new capital.

That is why founders should negotiate for durability, not just closing speed. A fast round that complicates every later round often turns out to be the expensive one.

The Legal Process for Issuing Preferred Stock

The legal work starts after the handshake, not before it ends. A signed term sheet usually isn't the issuance itself. The company still needs the corporate authority and documentation to create and sell the preferred shares validly.

The usual sequence

Most financings follow a sequence close to this:

- Term sheet negotiation: economics, control rights, and closing conditions are outlined.

- Due diligence: investors review legal, financial, and operational records.

- Definitive agreements: stock purchase documents, investor rights agreements, voting agreements, and amended charter documents are prepared.

- Approvals: the board approves the transaction, and stockholders approve charter changes when required.

- Issuance and records: the company issues the shares and updates the capitalization records.

- Filings and compliance: state filings and securities law notices are completed as needed.

Founders who want a finance-side checklist to match the legal work should review this guide to vetting deals effectively. It's a useful complement to legal diligence because many closing delays come from basic records gaps rather than headline deal disputes.

The document founders often underestimate

The charter amendment is usually the critical document because that is what authorizes the preferred class and defines many of its rights. If the charter isn't correctly amended and approved, the rest of the financing paperwork may not accomplish what the parties think it does.

For Washington companies raising early capital, this broader discussion of funding and seeding helps place the preferred issuance process in the larger startup financing lifecycle.

Closing funds is only part of the job. Closing the paperwork correctly is what makes the financing enforceable.

Frequently Asked Questions About Preferred Stock

Founders usually ask the hardest questions after they've read the term sheet twice and still feel uneasy. Those questions are usually the right ones.

| Question | Answer |

|---|---|

| Can a founder issue preferred stock without changing the company's formation documents? | Usually not if the current charter doesn't already authorize that class and its rights. In most startup financings, the company must amend the charter or certificate to create the preferred series and define its economics and governance terms. |

| Does preferred stock always mean investors control the company? | No. Preferred stock can include strong control rights, but it doesn't automatically hand over operational control. The real issue is the specific approval rights, board rights, and protective provisions in the deal documents. |

| Should founders fight every investor protection term? | No. Many protections are standard and commercially sensible. The better approach is to focus on the terms that distort future fundraising, make moderate exits unattractive, or give a small investor group blocking power over ordinary strategic decisions. |

A practical way to review preferred terms is to ask three business questions before signing: does this term make the next round harder, does it change sale incentives, and does it reduce management flexibility in routine decisions? If the answer is yes, that term deserves deeper negotiation even if it looks “market” on paper.

Founders don’t need to become securities lawyers. They do need to understand that preferred stock is where economics and governance meet. A term sheet can look short and still rewrite the company’s power structure.

By Design Law Firm & Legal Consultancy, PLLC helps startups and growth-stage companies structure financings, negotiate term sheets, and build durable governance frameworks before small drafting choices become expensive problems. Founders who want practical legal guidance on preferred stock, equity, fundraising, and corporate control can learn more at By Design Law Firm & Legal Consultancy, PLLC. Call us today at (206) 593-1519.