A Washington founder usually reaches the angel round at an awkward moment. The product is far enough along that friends-and-family money no longer fits the risk, but the company is still too early, too thinly staffed, or too unpredictable for a traditional venture fund. Payroll, product deadlines, customer traction, and legal cleanup all collide at once.

That's also the point where small mistakes become expensive. A rushed SAFE, a messy cap table, a casual securities violation, or a poorly negotiated pro rata right can follow the company into every later financing. For Washington startups, the legal side isn't separate from the fundraising strategy. It is part of the strategy.

Who Are Angel Investors and Why Do They Matter

Angel investors sit in the gap between bootstrapping and institutional venture capital. They're often individual investors, former operators, executives, or founders who can move faster than a fund and tolerate earlier risk. In practice, they often back companies when the business still looks more like a developing thesis than a settled machine.

That role has become far more important than many founders realize. In the United States, there were 363,460 active angel investors in 2021, and they typically wrote checks in the $25,000 to $100,000 range, helping bridge the space between founder capital and the first institutional round, according to this overview of the angel investor market.

Why founders pursue angels before venture funds

A first institutional round usually requires a level of traction, process, and market proof that many startups don't yet have. Angel investors often accept that ambiguity if the team is strong and the opportunity is credible.

That matters for a Washington startup building in software, AI, life sciences, climate, or consumer products. Local companies often need enough capital to hire carefully, tighten the product, and prove repeatable demand before they're attractive to seed funds on the West Coast or beyond.

Practical rule: The right angel round buys evidence, not just time.

Founders sometimes treat angel capital as interchangeable money. It isn't. A well-chosen angel can open recruiting channels, make customer introductions, pressure-test pricing, and help a founder avoid preventable governance mistakes. A poorly chosen one can complicate the cap table, demand inconsistent reporting, and distract management.

What angels are really buying

At this stage, angels rarely have the luxury of relying on long operating histories. They're underwriting the people, the problem, and the possibility that a small company can become much larger.

A strong founder should assume an angel is evaluating questions like these:

- Can this team execute: Do the founders have domain knowledge, speed, and judgment?

- Is the problem painful enough: Are customers trying to solve it already?

- Is there room to grow: Can the company plausibly become venture-scale, or is it a durable but smaller business?

- Will this founder be coachable: Can the company absorb advice without losing conviction?

That last point gets ignored too often. Angel rounds are relationship rounds. The legal documents matter, but so does the working dynamic after the wire lands.

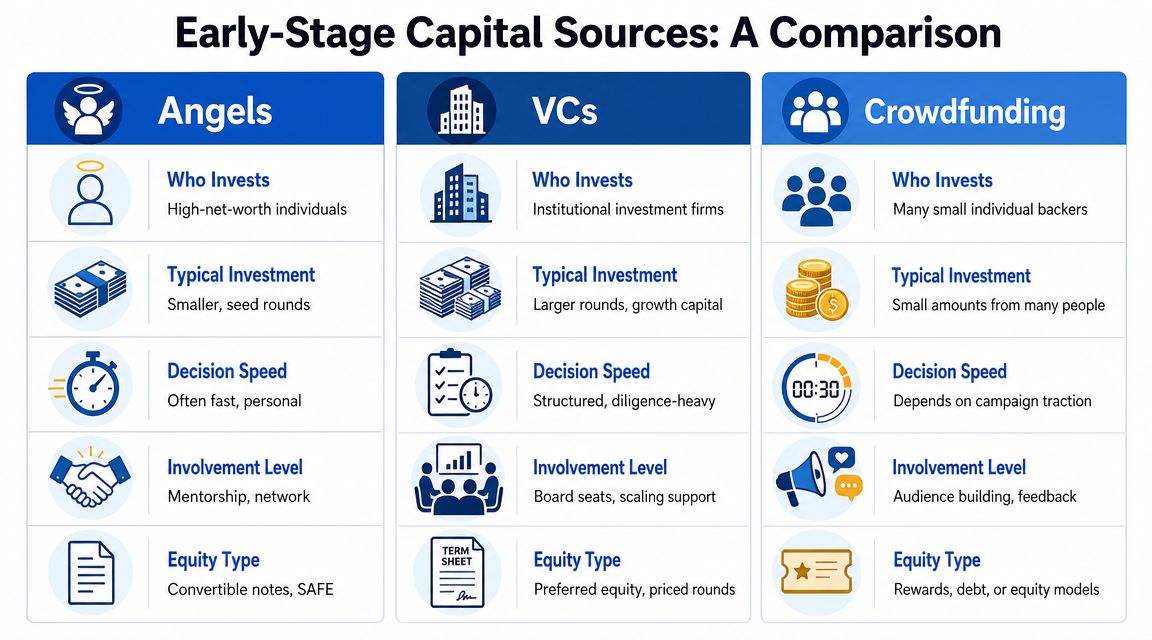

Angels vs VCs vs Crowdfunding A Comparison

The wrong funding source can create problems even when the money closes. Some companies should raise from angel investors. Some are better suited to a priced seed round from a fund. Others may benefit from a crowdfunding strategy if the brand, customer base, and compliance plan support it.

The real differences

Angel investors usually write smaller checks and make more personal decisions. Venture funds are more process-driven and often need a company to fit portfolio economics, ownership targets, and fund timing. Crowdfunding can broaden access to capital, but it can also create investor-management and disclosure burdens that a first-time founder underestimates.

The angel market has also become more organized. The old image of a single wealthy local investor isn't the full picture anymore. The market now includes groups and syndicates, and founders have to decide whether an individual angel, a network such as Sand Hill Angels, or a larger organized ecosystem is the better fit. A Carnegie Mellon summary notes 300,000+ investors participating in 71,000+ deals in 2017, and member groups collectively invested approximately $950 million in 2021, reflecting the scale and structure of the category, as summarized in this CMU overview of the angel investor landscape.

Early-Stage Funding Comparison

| Attribute | Angel Investors | Venture Capital (Seed Stage) | Equity Crowdfunding |

|---|---|---|---|

| Who invests | Individuals, syndicates, organized angel groups | Institutional funds | Large pool of online investors |

| Typical fit | Pre-seed and early seed companies | Companies with stronger traction and fundable scale story | Consumer-facing or community-backed companies that can manage broad investor communications |

| Decision style | Personal, relationship-based, often faster | Formal, committee-driven, structured diligence | Platform-based, marketing-heavy, compliance-sensitive |

| Strategic value | Mentorship, introductions, operating input | Follow-on signaling, governance structure, institutional credibility | Customer engagement and public validation, if done well |

| Main founder risk | Too many small investors or inconsistent terms | Higher ownership expectations and tighter control terms | Cap table complexity, disclosure burden, and execution risk |

Which path usually works best

A founder deciding among these routes should ask different questions than “Where can the money come from?”

- Choose angels when the company needs early conviction, industry contacts, and flexible structuring.

- Choose venture capital when the startup already shows enough traction to support institutional diligence and a larger ownership discussion.

- Choose crowdfunding only after understanding securities compliance, public communications limits, and cap table consequences. For Washington founders, this guide on crowdfunding and securities law for Seattle entrepreneurs is a useful starting point.

Some money is expensive because of valuation. Other money is expensive because of the people, process, and obligations attached to it.

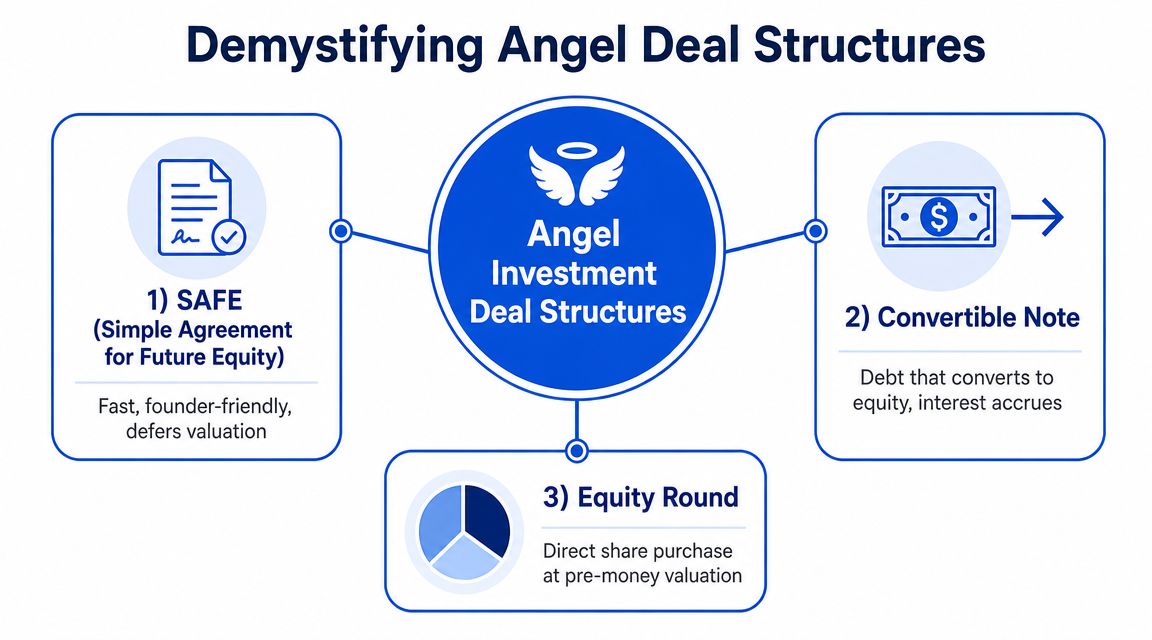

Understanding Angel Deal Structures and Term Sheets

Most first angel deals fall into one of three buckets. SAFE, convertible note, or priced equity round. The right structure depends on timing, bargaining power, investor expectations, and how cleanly the company wants to set up its next round.

What each structure does

A SAFE is the fastest and simplest paper in many early deals. It usually defers the valuation fight until a later financing. Founders like SAFEs because they can reduce legal friction. Investors like them when they believe the company will raise a next round soon enough for the instrument to convert on expected terms.

A convertible note is similar in spirit, but it begins as debt that converts into equity later. That means it adds debt concepts to an already delicate stage. If the company needs speed but the investor wants a more traditional instrument, a note may appear. It can work, but founders should understand the maturity, conversion, and default language instead of assuming it’s just a SAFE with extra paper.

A priced round is the most explicit structure. The company sets a valuation, sells shares directly, and usually adopts a fuller package of investor rights. That can be cleaner in the long run, especially if the round is large enough to justify the cost and discipline.

The terms that actually matter

Early-stage valuation is uncertain, so angels often use convertible structures. They typically target 5% to 15% equity in pre-seed rounds and 15% to 20% in seed rounds, and the founder needs to understand how valuation cap and check size affect dilution because that can shape later control and fundraising flexibility, as explained in this practical guide to angel investment terms.

For founders, the most important term sheet concepts usually include:

- Valuation cap: This sets the maximum valuation at which a SAFE or note converts. A low cap can result in a transfer of greater ownership than the founder expected.

- Discount: This gives the investor a better price than new money in the next round.

- Pro rata rights: These let the investor maintain ownership in later rounds. Reasonable pro rata rights are common. Overbroad versions can complicate future financings.

- Liquidation preference: This matters more in priced rounds. It affects who gets paid, and in what order, in a sale or wind-down.

- Information rights: Monthly updates may sound harmless, but the reporting burden adds up.

What founders often miss

The legal issue isn’t only what a term means in isolation. It’s how terms interact over time. A founder can accept a “standard” cap, plus broad pro rata rights, plus side-letter promises, and only later realize the company has become hard to finance cleanly.

That’s why the underlying paper matters. Founders who need a refresher on baseline deal documentation and negotiation discipline should review these essential contracts for business owners before circulating investor documents.

A founder shouldn’t negotiate an angel round as if the angel round is the last financing. Every clause should be tested against the next one.

Navigating Securities Law and Washington State Rules

Selling stock, SAFEs, or convertible notes means selling securities. That triggers federal and state law even when the deal feels informal, local, or relationship-driven. A startup doesn’t get a free pass because the investor is a friend of a friend or because the company is still small.

Why securities compliance matters in a small round

Most startup financings rely on an exemption from full securities registration. Founders often hear “Reg D” and move on. That’s risky. The exemption is the path that makes the round lawful, and the details affect how the company can market the raise, who can invest, and what records need to be kept.

Two federal routes often come up in private startup rounds:

- Rule 506(b): Common when the company is raising through existing networks and introductions. This route is generally used for private outreach, not broad public solicitation.

- Rule 506(c): Often considered when the company wants to market the round more openly, but that comes with stricter verification expectations for investor status.

A founder doesn’t need to become a securities lawyer. That founder does need to know that a LinkedIn post, podcast appearance, demo day slide, or email blast can create issues if the legal approach and fundraising behavior don’t match.

Washington-specific practical points

Washington companies also need to think about state-level notice filings and regulator expectations. Even when a federal exemption applies, state notice obligations can still exist. The Washington State Department of Financial Institutions is the place founders and counsel should check when planning or closing a private offering.

Good compliance also connects to broader corporate records. Regulators, investors, and later-stage funds all care whether the company knows who owns it, who controls it, and whether records match reality. For founders cleaning up internal reporting obligations, this discussion of the Corporate Transparency Act and preparation steps is relevant because ownership and governance discipline tend to surface together during financing.

What not to do

The most common mistakes are ordinary ones:

- Posting too freely: Public statements about the raise without matching the exemption strategy.

- Treating templates as legal advice: Online forms can help with vocabulary, but they don’t decide compliance.

- Skipping state filings: Federal compliance doesn’t automatically finish the job.

- Closing before cleanup: If formation documents, board approvals, or stock records are incomplete, the financing should pause long enough to fix them.

Washington founders usually benefit from thinking about securities law early, not after the first investor says yes.

How to Prepare Your Startup for Angel Investment

A founder is rarely rejected because the deck needed a prettier font. Rejection usually comes from unresolved legal basics, weak evidence, vague use of funds, or a team that doesn’t inspire confidence.

The investor-ready checklist

Founders should prepare the company as if diligence starts the moment the first serious meeting ends.

- Clean corporate formation: The entity should be formed correctly, board consents should exist, stock issuances should be documented, and founder vesting should make sense.

- IP ownership: Contractors, employees, and co-founders should have signed assignment documents. If the company doesn’t own its product, investors notice quickly.

- Cap table accuracy: Every share, promise, option, SAFE, and note needs to appear correctly.

- Financial model: It doesn’t need to be ornate. It does need to show assumptions, hiring plans, and cash use clearly.

- Use of funds: “More runway” is weak. “Hire an engineer, complete enterprise security work, and support a defined go-to-market motion” is stronger.

- Customer proof: Pilots, paid users, usage trends, letters of intent, and retention signals all matter qualitatively.

- Founder story: Investors need to understand why this team should solve this problem now.

The strategic side matters as much as the checklist. NBER research found that angel-backed startups were at least 14% more likely to survive 18 months or more, hire 40% more employees, and were 10 percentage points more likely to exit the startup phase successfully, which supports the idea that the value of angels often comes from mentorship and network, not just capital, as summarized by the NBER digest on how angel investors help startup firms.

Show why this specific angel helps

That research matters because founders often pitch for money without explaining why a given investor belongs on the cap table. Strong founders do the opposite. They explain how the investor’s network, sector expertise, recruiting reach, or customer credibility will help the company move faster.

This overview of funding and seeding issues for early-stage companies is useful for founders who are still tightening the legal and strategic groundwork before outreach begins.

A short visual summary can help teams align internally before they start taking meetings.

Founder lens: The best angel pitch answers two questions at once. Why should this company win, and why should this investor be part of that outcome?

The Process of Negotiation and Due Diligence

An angel round often starts casually. An introduction. A coffee. A warm email after a demo day. Then the process gets serious very quickly. Once an investor moves from curiosity to interest, the founder’s job shifts from storytelling to disciplined proof.

What the first conversations are really testing

In the first meeting, the investor usually isn’t trying to master every detail of the business. The investor is asking whether the company is worth deeper time. That means the founder needs a sharp explanation of the problem, solution, customer, market, and near-term plan.

After that, the diligence questions get more concrete. Angel diligence tends to prioritize team capability, traction quality, and market size over historical financials, and the most persuasive pitch combines hard metrics with a credible unit economics story and a concise explanation of how the capital accelerates execution, according to this analysis of what angel investors actually evaluate.

How a well-run diligence process feels

A disciplined founder makes diligence easy to complete. That usually means a simple data room, clean naming conventions, prompt follow-up, and consistency between the deck, model, cap table, and legal documents.

A useful diligence package often includes:

- Corporate records: Certificate of formation, bylaws, board consents, stock ledger, and prior financing documents.

- Commercial materials: Pitch deck, customer pipeline summary, material contracts, and partnership documents.

- Financial information: Historical financials if available, current budget, assumptions, and cash forecast.

- Product and IP materials: Demo links, product roadmap, patent or trademark filings if relevant, and IP assignment paperwork.

- Team information: Founder bios, org chart, key hires, and advisory relationships.

Negotiation points that deserve attention

Founders often spend too much time fighting over headline valuation and too little time on terms that can create friction later. Side letters, investor information rights, board observer asks, veto concepts disguised as “consent rights,” and open-ended pro rata language deserve close review.

Negotiation also has a relationship component. A founder who is evasive loses trust. A founder who discloses real risks clearly usually gains credibility. Good investors know early-stage companies are imperfect. What they won’t tolerate is surprise.

One practical approach works well. Keep momentum, answer quickly, and avoid negotiating every issue by email. Material points should be discussed directly, then reflected in clean documents. That reduces misunderstanding and preserves the working relationship after closing.

When to Engage Legal Counsel in Your Angel Round

Legal counsel should enter the process before the founder starts trading draft documents with investors. Waiting until a term sheet is “mostly agreed” often means the founder has already made business concessions that are difficult to reverse.

The key trigger points

There are a few moments when outside counsel stops being optional and becomes protective.

- Before outreach begins: If the entity, cap table, IP chain, or founder stock records are messy, they should be fixed before serious diligence starts.

- When the first term sheet arrives: Valuation mechanics, investor rights, and financing structure need legal review.

- Before signing SAFEs, notes, or stock purchase documents: Form matters, but deviations from standard forms matter more.

- When securities filings are due: Exempt offerings still require process discipline.

- When multiple investors are joining the round: Side terms that seem harmless in one negotiation can become unworkable across several investors.

Why this saves money instead of wasting it

Founders often see legal spend as a drag on runway. In a financing, that framing is too narrow. Good counsel protects ownership, catches compliance issues before they harden, aligns board and stockholder approvals, and keeps the company financeable for the next round.

That is especially important in angel rounds because the documents look simple. Simplicity on paper can hide serious downstream consequences. A rushed cap table cleanup, an overbroad information right, or a sloppily handled exemption can cost far more to unwind later than it would have cost to structure correctly at the start.

A founder doesn’t need a law firm to run the business. That founder does need legal guidance when the company is selling securities, reshaping ownership, and setting terms that future investors will inspect closely.

By Design Law Firm & Legal Consultancy, PLLC helps Washington founders handle early-stage financings with the level of care these deals require. For startups preparing for an angel round, cleaning up governance, or negotiating investor documents, the team provides practical, business-minded counsel that protects the company while keeping the financing moving. Learn more at By Design Law Firm & Legal Consultancy, PLLC. Call us today at (206) 593-1519.