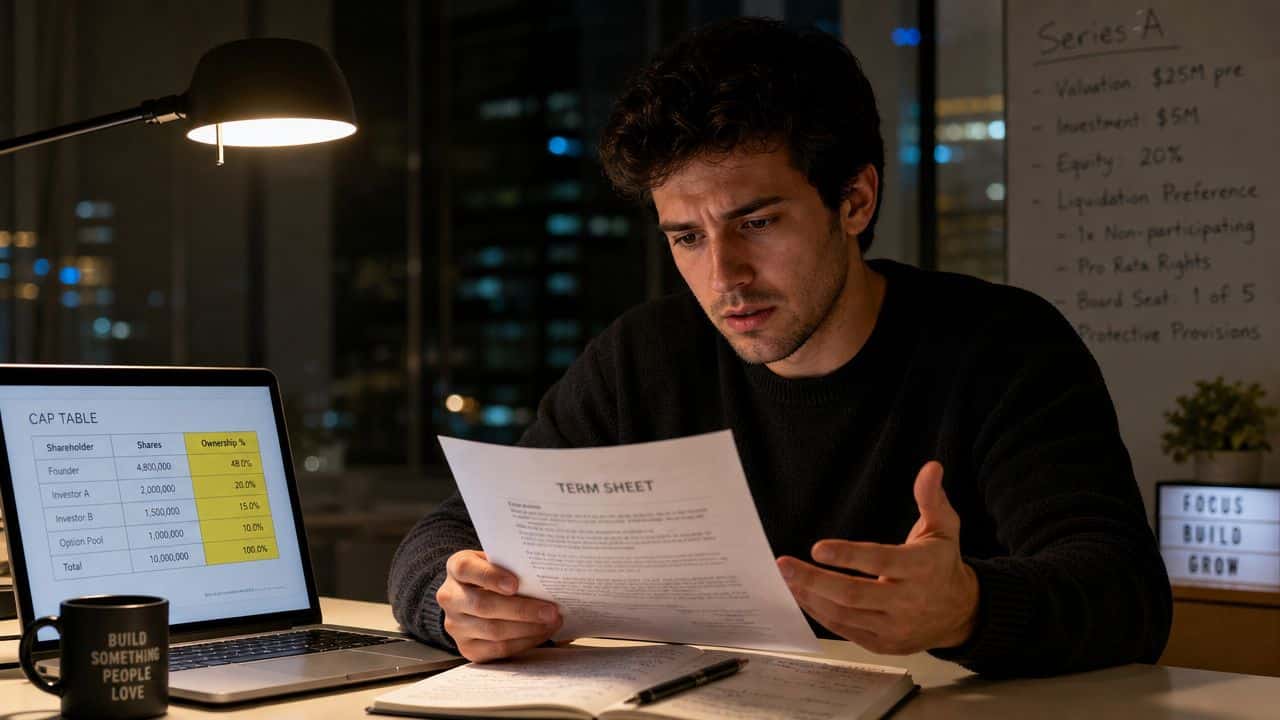

A founder in Washington gets the first real term sheet. The valuation looks flattering. The investor's brand carries weight. Then the cap table model lands in the inbox, and the founder notices the uncomfortable part. Ownership is about to shrink.

That moment is where most conversations about dilution go wrong. Founders often treat the percentage drop as the whole story. It isn't. The legal and financial question isn't whether ownership changes. It will. The question is whether the company is issuing new equity on terms that improve the odds of building something far more valuable.

The Founder's Dilemma Understanding Dilution

A Washington founder signs a financing term sheet, skims to valuation, and likes what they see. Then counsel sends the revised cap table. The founder still holds the same number of shares, but the ownership percentage drops. That is dilution.

Equity dilution happens when the company issues new shares and an existing owner ends up with a smaller percentage of the company without selling any stock. The emotional reaction is understandable. In my experience, first-time founders do not just see a lower number on a spreadsheet. They see questions about control, board influence, future proceeds, and whether the years they put into the business are being priced correctly.

Why founders react so strongly

For a founder, ownership is rarely just economics. It is also voting power, board influence, and a record of who built the company before outside money arrived. A drop from 100% to 80% can feel smaller on paper than it does in the room.

That reaction becomes a problem when percentage protection turns into the only goal. I have seen founders under-raise to avoid dilution, resist an option pool they need to recruit senior hires, or take money from the wrong investor because the headline percentage looked better. Those choices can weaken the business and leave the founder with more paper ownership in a company that is harder to finance, govern, or sell.

Practical rule: A smaller stake in a well-funded company with the right terms often beats a larger stake in a company that cannot hire, execute, or survive the next 18 months.

Percentage is not the same as outcome

Founders should track both economics and control. Percentage ownership affects exit proceeds, but financing terms also affect board seats, protective provisions, investor consent rights, liquidation preferences, and the size of the option pool. In Washington companies, those legal details often shape the founder's real position more than the first percentage drop does.

Valuation language also needs to be read carefully before anyone agrees to the round. A clear explanation of Post Money Valuation helps show how ownership is measured after the financing closes and why a strong headline valuation can still produce meaningful dilution if the round structure is aggressive.

The investor mix matters too. Founders deciding whether to raise from funds, strategic investors, or individuals should understand how angel investors in early-stage companies often affect governance, follow-on financing, and negotiation dynamics in the next round. The right dilution is a business decision. The wrong dilution is a legal and strategic mistake that keeps showing up long after the wire hits the bank.

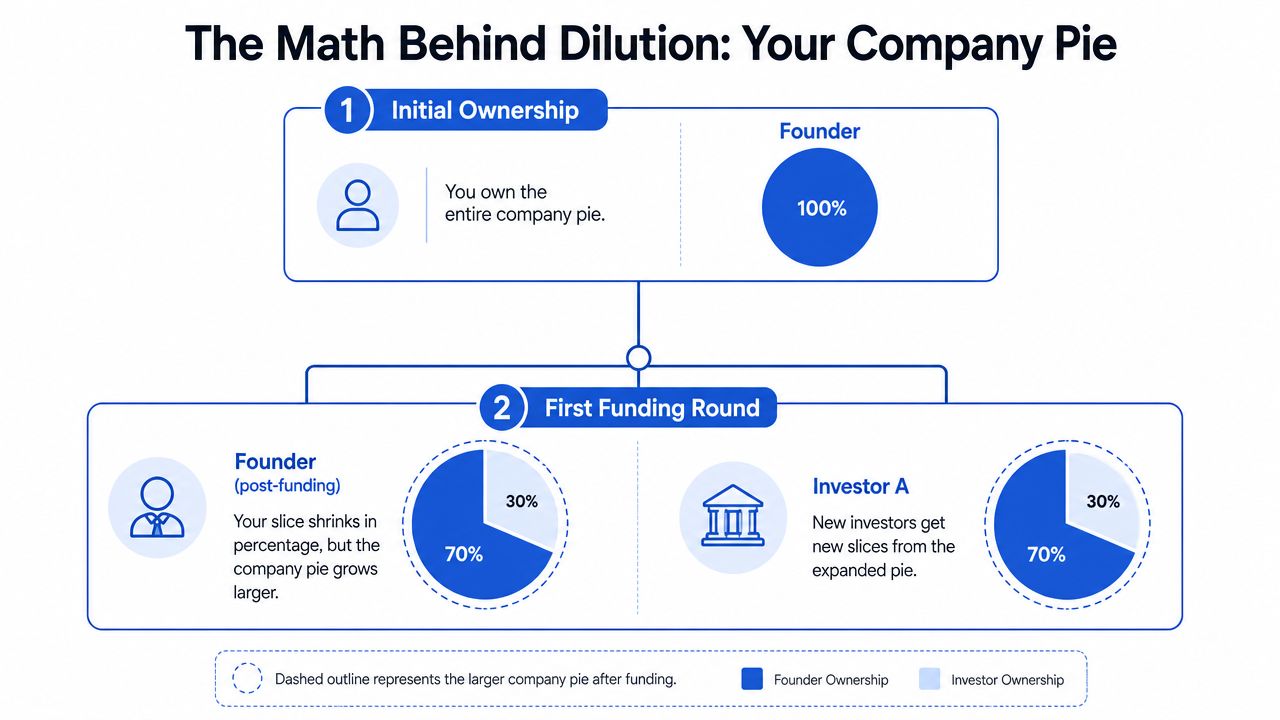

The Math Behind Dilution A Cap Table Breakdown

A founder signs a term sheet expecting to sell 20% of the company. Closing arrives, the option pool is increased before the round, the SAFE notes convert, and the final ownership number is lower than expected. That surprise usually comes from cap table math, not bad faith.

Dilution is a denominator problem. The mechanics of dilution do not involve founders handing over existing slices one by one. The company issues new shares, the total share count goes up, and each existing holder owns a smaller percentage of the company unless they also receive additional shares.

A simple before and after cap table

Start with one founder.

| Holder | Shares | Ownership |

|---|---|---|

| Founder | 1,000,000 | 100% |

| Total | 1,000,000 | 100% |

Now assume the company raises money and issues 250,000 new shares to an investor.

| Holder | Shares | Ownership |

|---|---|---|

| Founder | 1,000,000 | 80% |

| Investor | 250,000 | 20% |

| Total | 1,250,000 | 100% |

The founder still holds 1,000,000 shares. What changed is the denominator.

That sounds simple until the legal documents define which shares count in that denominator. In Washington financings, founders often focus on valuation and miss the drafting choices that change the share count before the money even hits the account.

The terms that matter on a term sheet

Three concepts drive the math:

- Pre-money valuation: The company's value before the new investment.

- Post-money valuation: The company's value after the investment closes.

- Fully diluted share count: The total share base used to calculate ownership, often including shares reserved for options and shares that may be issued on conversion.

Those definitions control real outcomes. If investors require the option pool to be expanded pre-closing, founders usually absorb that dilution first. If SAFEs or convertible notes convert at closing, their shares can materially change the ownership picture. If the company has multiple classes of stock or side letters, the spreadsheet can look cleaner than the legal reality.

This is why I tell founders to mark up the cap table and the term sheet together. A strong headline valuation does not protect ownership if the fully diluted count is working against you.

Founders preparing for a round should also treat early legal setup as part of pricing the deal. The structure choices made during funding and seeding affect how much dilution shows up now, how much is deferred to the next round, and how hard it will be to explain the cap table to future investors or an acquirer.

A cap table is not just a spreadsheet. It is a legal allocation of ownership, and small definition changes can produce expensive surprises.

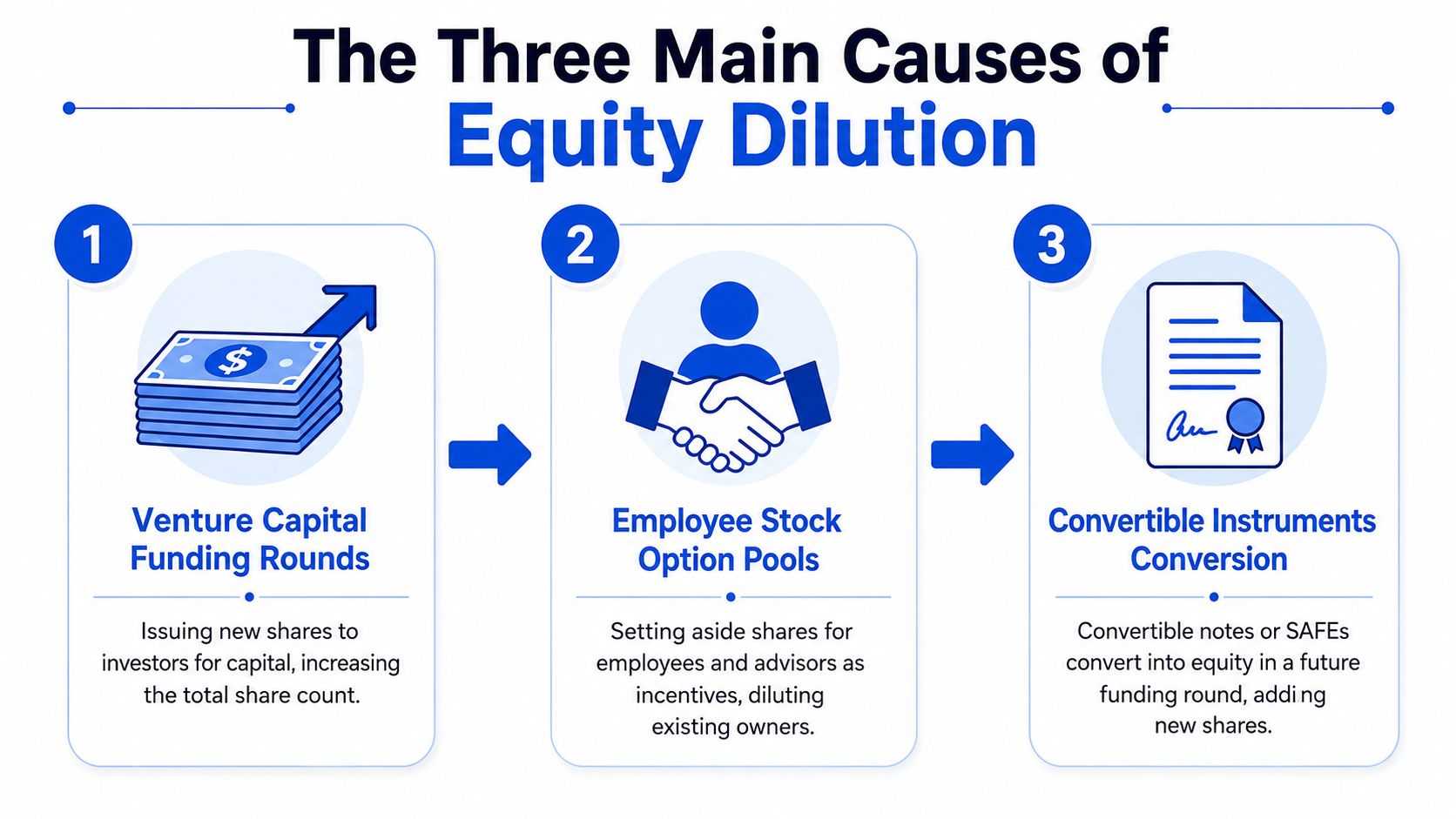

The Three Main Causes of Equity Dilution

Funding rounds get most of the attention, but they're only one source of dilution. In practice, founders usually get diluted through a sequence of actions that build on each other.

Priced equity rounds

A priced round issues shares to new investors at a negotiated price per share. That can be seed, Series A, or later rounds. This is the most visible dilution event because everyone can see the investor's new ownership on the cap table.

What works is raising enough capital to accomplish a real milestone. What doesn't work is raising too little to preserve optics. A founder who takes a smaller check just to protect percentage may be back in market too soon, often with less bargaining power.

Employee stock option pools

An option pool is the equity reserve used to hire and retain employees, executives, and sometimes advisors. Founders often underestimate its impact because the pool may sit unissued for a while. The dilution still exists once those shares are reserved in the cap table structure used for the financing.

A healthy option pool can be productive dilution. It gives the company a way to recruit people who can increase product velocity, sales execution, and operational discipline. A bloated pool, though, can become lazy drafting disguised as planning.

A founder should ask:

- Who is the pool really for: Near-term hires, or a vague future plan?

- When is it created: Before the round or after?

- How much hiring does it support: The legal model should match the operating plan.

Convertible instruments

SAFEs and convertible notes often create the sharpest surprise because their effect is delayed. They don't always feel dilutive when the company signs them. They become dilutive when they convert into equity in connection with a later financing.

That timing matters. Founders sometimes model only the new investor shares in the priced round and forget the convertibles that will convert at the same time.

According to Carta's explanation of share dilution, dilution often occurs at multiple events in sequence, not only at the priced round itself. Option pool expansions, convertible notes or SAFEs converting, and new investor shares can stack into a single cap-table change.

A founder shouldn't ask only, “How much dilution does this round cause?” The better question is, “What total dilution hits the cap table at closing?”

For Washington companies using alternative capital pathways, securities compliance can also shape how equity is issued and when. Founders considering broader solicitation or community financing should understand the legal structure first, especially in crowdfunding and securities law for Seattle entrepreneurs.

A Tale of Two Founders A Dilution Case Study

Two Washington software founders start in similar positions. Alex and Ben each build a promising company with a product in market, early customer traction, and a need for outside capital. Both care about ownership. They part ways on strategy.

Alex preserves percentage

Alex hates dilution. The financing process is approached like a defensive exercise. The company raises a smaller amount from an investor who offers a flattering valuation but limited help after closing. Alex keeps more of the cap table on paper.

That decision looks smart in the short term. The founder retains a larger headline stake. The board remains simple. The financing announcement sounds good.

Then operational reality sets in. Hiring moves slowly. The product roadmap stretches. The company comes back to market sooner than expected because the first round didn't provide enough runway to reach the next meaningful milestone.

Ben trades ownership for momentum

Ben takes the opposite approach. The company raises a larger round from an investor who asks for more equity but brings recruiting help, financing discipline, and sharper governance. Ben accepts more dilution upfront.

That choice doesn't feel comfortable. Most founders would prefer to keep a bigger percentage. But the larger round gives the company room to hire, test pricing, and build a stronger fundraising story for the next financing.

The second round arrives under different conditions. Ben's company has more bargaining power because the prior capital was used to create visible progress. Alex's company is still negotiating from need.

The lesson founders usually learn late

The legal lesson isn't that dilution doesn't matter. It does. Ben can still make mistakes by over-issuing equity, agreeing to an oversized option pool, or accepting investor controls that narrow founder flexibility.

The point is narrower and more useful. Ownership percentage is only one variable. A founder can preserve percentage and still lose strategic ground. Another founder can give up more ownership and build a far more valuable company.

A Washington founder reviewing financing terms should test at least three questions before signing:

| Question | Why it matters |

|---|---|

| Does this round fund real milestones? | Capital should buy time and progress, not just survival. |

| Does this investor improve the company beyond cash? | Board judgment, hiring help, and credibility can matter. |

| What does the next round look like if this one underperforms? | Bad assumptions compound quickly. |

Alex focused on dilution as loss. Ben treated dilution as a tool. Only one of those approaches tends to produce room for better legal and strategic choices later.

Beyond the Numbers The Strategic Impact of Dilution

Founders usually meet dilution first as a spreadsheet issue. It becomes much more than that once financing documents are signed.

Control can move faster than expected

Equity dilution is not just a reduction in ownership percentage. It also changes the economics of each share because new shares increase the denominator used to calculate per-share claims on earnings and voting rights, as described in Wikipedia’s stock dilution overview.

That matters because founders often track economics and ignore control. Those are related, but they aren’t identical. A founder can still own a meaningful stake and lose practical authority through board composition, protective provisions, investor veto rights, and voting alignment among preferred holders.

A cap table tells part of the story. The charter documents, investor rights agreement, voting agreement, and board structure tell the rest.

Psychology affects judgment

Dilution also changes founder behavior. A founder who feels over-diluted may become reluctant to hire aggressively, issue option grants, or raise follow-on capital even when the company needs it. Another founder may swing too far the other way and treat equity as cheap because it doesn’t feel like cash.

Neither instinct helps.

Founders build better companies when they treat equity like the most expensive currency on the balance sheet.

Investors view founder ownership differently

Investors usually want founders to remain strongly incentivized. But investors also need enough ownership to justify the work, risk, and reserve strategy that come with backing a startup. That tension is normal.

The practical takeaway is that dilution negotiations are rarely about a single number. They’re about incentives, governance, recruiting ability, and the company’s ability to finance the next stage without breaking alignment among the people around the table.

Protecting Your Stake Strategies to Manage Dilution

Dilution can’t be eliminated from a venture-backed company. It can be managed. Founders who approach it as a legal design problem usually fare better than founders who treat it as a surprise.

Negotiate the right valuation, not just the highest one

A stronger valuation can reduce dilution in a round, but valuation shouldn’t be viewed in isolation. The best term sheet is not always the one with the highest headline number. If the investor demands harsher controls, a larger pre-closing option pool, or terms that complicate the next financing, the apparent win may be expensive.

Founders should compare term sheets as full packages, not vanity metrics.

Model the option pool before anyone else does

Option pools are one of the most common places where founders get diluted without fully appreciating the size of the hit. A disciplined founder asks for a hiring plan that supports the pool size. If the company needs options for key hires, the pool should be grounded in a real recruiting map, not a generic request from counsel or investors.

A smaller but credible pool is often better than an oversized reserve with no near-term hiring logic.

Know what rights exist and who gets them

Some rights don’t stop dilution, but they shape its effect.

- Pro-rata rights: These let an investor buy into later rounds to maintain ownership.

- Anti-dilution provisions: These are usually investor protections that matter most in a down round.

- Vesting and repurchase rights: These don’t change financing dilution directly, but they protect the cap table from dead equity.

Founders should understand each right before signing. Language that looks standard can still produce a painful result in the wrong scenario.

Forecast dilution as a sequence

The strongest cap table planning usually includes:

- Current ownership and reserves

- Expected note or SAFE conversions

- Option grants tied to actual hires

- The next financing round and likely follow-on scenarios

Founders separate “Can this round close?” from “Does this financing path hold together over time?” The second question matters more.

Next Steps A Legal Checklist for Washington Founders

Washington founders should get legal advice before dilution becomes a live dispute. The cleanest cap tables usually start with early planning, not cleanup after a rushed financing.

A short checklist helps:

- Before incorporation: Decide how founder equity will be issued, vested, and documented.

- Before creating an option pool: Match the pool to a real hiring plan and board approvals.

- Before signing a SAFE, note, or priced term sheet: Model the conversion and the post-closing cap table.

- Before forecasting the next round: Test whether current terms create avoidable pressure later.

- Before choosing financing sources: Compare dilutive capital with other funding paths. Some founders may want to explore non-dilutive capital before issuing more equity.

Founders operating through entities other than a Delaware C corporation should also tighten the company’s governance documents early. For Washington businesses, the basics still matter. An operating agreement, for example, shapes ownership rights, governance, and transfer restrictions long before an investor appears. A useful starting point is understanding why every Washington LLC needs an operating agreement.

By Design Law Firm & Legal Consultancy, PLLC helps Washington founders build financing structures, governance documents, and cap table strategies that support growth without losing sight of control, compliance, or long-term value. Learn more at By Design Law Firm & Legal Consultancy, PLLC. Call us today at (206) 593-1519.