A founder is often closest to the problem when the cap table goes wrong. The company is moving fast, a seed round is almost signed, and the due diligence request looks simple enough: send the current cap table. Then the spreadsheet opens, and the trouble starts. A SAFE isn't reflected correctly. An early advisor promise never became signed paper. The option grant totals don't match the board approvals. What looked like a tidy ownership file turns into a legal and financing problem.

That moment is why capitalization table management matters. A cap table isn't clerical overhead. It's the company's ownership ledger, negotiation tool, audit trail, and, in practice, one of the first documents investors use to judge whether leadership runs a disciplined business.

Your Cap Table Is More Than a Spreadsheet

A capitalization table records who owns the company, what type of security they hold, and what happens when those rights convert, vest, or dilute. For a newly formed company with two founders, that may feel simple. It stops being simple the moment the business issues restricted stock, grants options, signs a SAFE, or starts discussing a priced round.

A clean cap table does more than answer “who owns what.” It answers harder questions that come up in real transactions. Who has vested equity and who does not. Which instruments convert later. Whether the option pool is available. Whether the board approved every issuance. Whether the numbers in the spreadsheet match the signed legal documents.

What founders usually discover too late

Founders often treat the cap table as a backward-looking record. Investors treat it as a forward-looking risk file. That difference matters.

A venture fund reviewing a company doesn't just want a list of holders. The fund wants confidence that the company can close the round without ownership disputes, surprise dilution, or cleanup work in the middle of drafting financing documents. That is one reason a fundraising process usually goes more smoothly when the legal records and cap table have been maintained together from the start, especially before the company begins funding and seeding work.

A messy cap table rarely stays a spreadsheet problem. It turns into a board consent problem, a securities compliance problem, or a closing-delay problem.

The cap table is part legal record, part strategy file

The legal source of truth is still the underlying paperwork. Stock purchase agreements, board consents, option grants, SAFEs, notes, and charter documents control. But the cap table is the operating view that brings those records together into one place so the company can make decisions.

That makes capitalization table management a strategic discipline. It affects fundraising readiness, hiring, option planning, founder dilution, and exit preparation. When the file is accurate and current, leadership can model consequences before signing a term sheet. When it isn't, the company negotiates in the dark.

Building Your Initial Cap Table Structure

A founder doesn't need an advanced platform on day one. A founder does need a structure that won't collapse after the first real financing event.

At minimum, the initial cap table should distinguish between authorized shares, issued shares, outstanding shares, and the fully diluted view. Those categories get confused constantly, and confusion at the start usually produces bad math later. If the company can't explain those buckets clearly, it isn't ready to model dilution or answer investor diligence questions.

What belongs in the first version

A usable early-stage cap table usually includes:

- Security holder identity. Legal name, contact information, and role.

- Security type. Founder common stock, preferred stock, option, SAFE, note, or warrant.

- Share or unit count. If the instrument doesn't convert yet, the company should track it separately rather than force it into common-equivalent shares too early.

- Grant or issuance date. Dates matter because approvals, vesting, and tax treatment all depend on timing.

- Vesting status. Founders and employees should not be mixed together in one undifferentiated ownership number.

- Board approval reference. The cap table should tie back to the actual authorization.

For founders who want a grounding in how share capital works at the company level, Stewart Accounting Services on share capital is a useful companion resource because it helps clarify the difference between what a company may issue and what it has issued.

Spreadsheet or software

A spreadsheet can work briefly. It often stops working sooner than founders expect.

The shift from manual spreadsheets to automated software reduced equity management errors by over 90%, and approximately 78% of Series A and B startups in the US used dedicated cap table software in 2023, according to Visible's cap table overview. That adoption trend isn't about fashion. Modern financing instruments create layers of conversion logic, vesting detail, and scenario modeling that spreadsheets handle poorly once the structure gets even moderately complex.

| Feature | Spreadsheet | Cap Table Software |

|---|---|---|

| Setup speed | Fast for a two-founder company | Slightly slower at the start |

| Manual math risk | High once options or convertibles appear | Lower because calculations are automated |

| Audit trail | Usually weak unless carefully maintained | Built-in history is standard |

| Scenario modeling | Easy to break | Usually structured and repeatable |

| Board and legal reconciliation | Manual | Easier to track against records |

| Investor readiness | Depends heavily on discipline | Stronger once the company has institutional financing |

A practical decision rule

A spreadsheet may be enough if the company has only founders, one class of common stock, and no outside money. That window is short.

The better time to move into software is usually before the first SAFE, before the first formal option grants, or before the company starts negotiating preferred terms such as preferred stock rights and structure. Once there are multiple stakeholder types, spreadsheets tend to create parallel versions, hidden formulas, and avoidable reconciliation work.

Practical rule: If someone needs to ask which tab is the current one, the company has already outgrown the spreadsheet.

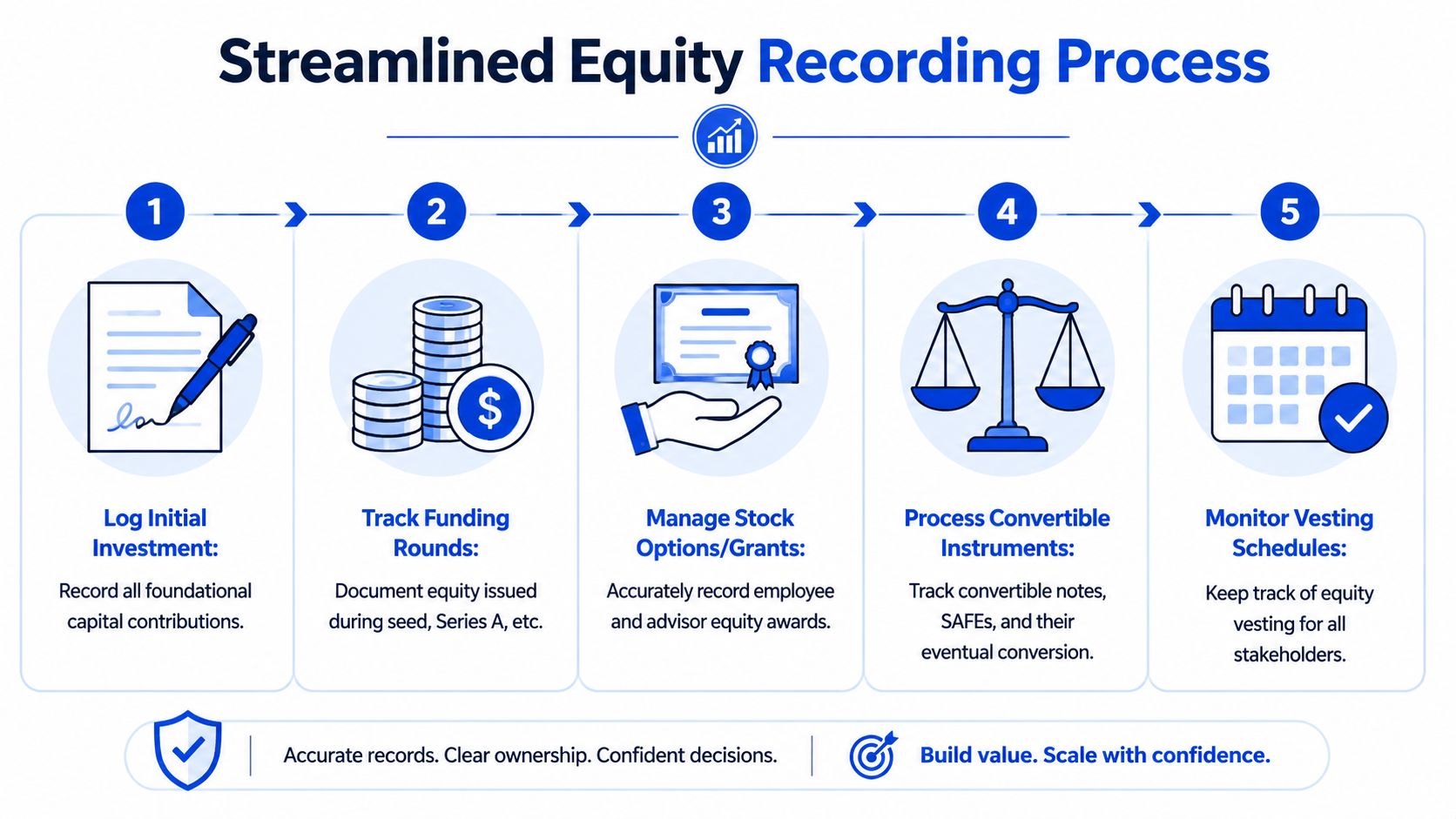

Recording Equity and Complex Financial Instruments

The strongest cap tables are built by disciplined recording, not heroic cleanup. Every issuance, grant, transfer, and financing event should be captured in a way that mirrors the signed documents. That is how a company creates a real single source of truth.

Founder stock and board-approved issuance

Founder equity should never appear in the cap table because “everyone knows” who owns it. It belongs there only after the company has completed the underlying steps: the board approves the issuance, the purchase documents are signed, and the ledger reflects the shares issued.

That means the cap table should record the holder, class, number of shares, vesting terms if any, and the approval date. If the founder shares are subject to vesting, the cap table needs to show vested and unvested status separately. One lump number hides risk and creates confusion later.

Options need more than a grant line

Stock options are where many early companies lose control of detail. A cap table entry for options should capture the grant date, option count, exercise price, vesting schedule, cliff if applicable, and status over time. It should also show whether options are still outstanding, have been exercised, or were forfeited after departure.

A founder doesn’t need to publish every employee detail to every investor. But internally, the company does need complete records. Without them, the option pool becomes unreliable, and hiring plans become guesswork.

SAFEs and notes should be tracked separately first

SAFEs and convertible notes cause repeated problems because teams try to force them into equity ownership before conversion. That is a mistake. Until conversion happens under the governing documents, those instruments should sit on their own ledger lines and be modeled on a pro forma basis.

That separate treatment matters because the conversion mechanics often depend on later valuation, discounts, caps, accrued terms, or negotiated definitions in the financing documents. If the company records them as though they are already common or preferred, the fully diluted picture becomes misleading.

A 2024 report showed that 43% of US startups face legal disputes or fundraising delays due to mismanagement of convertible debt instruments, with nearly a third of those issues stemming from unclear conversion terms or unrecorded equity stakes, according to LTSE’s best practices for cap table management.

Convertible instruments aren’t side notes. They are future ownership claims that need disciplined tracking from the day they are signed.

A recording process that holds up in diligence

A reliable workflow usually looks like this:

- Collect the controlling document first. Board consent, stock purchase agreement, SAFE, note, option grant, or transfer document.

- Enter the event immediately. Waiting for month-end or quarter-end invites drift.

- Tie the entry to the approval. A cap table without authority references is only a spreadsheet.

- Update the fully diluted model separately where needed. Especially for SAFEs and notes.

- Reconcile after the event closes. The signed documents, stock ledger, and cap table should align.

Where companies break the chain

The failure points are usually ordinary, not exotic:

- Unsigned promises. Someone “got equity” but no one can produce the agreement.

- Unrecorded departures. The person left, but the forfeiture or repurchase never made it into the records.

- Pool confusion. Management counts reserved options as available without checking granted but unapproved awards.

- Term mismatch. The spreadsheet reflects a valuation cap or vesting schedule that doesn’t match the executed form.

Those are not bookkeeping glitches. They are legal inconsistencies. Once investors start reviewing ownership, every one of them becomes expensive to resolve.

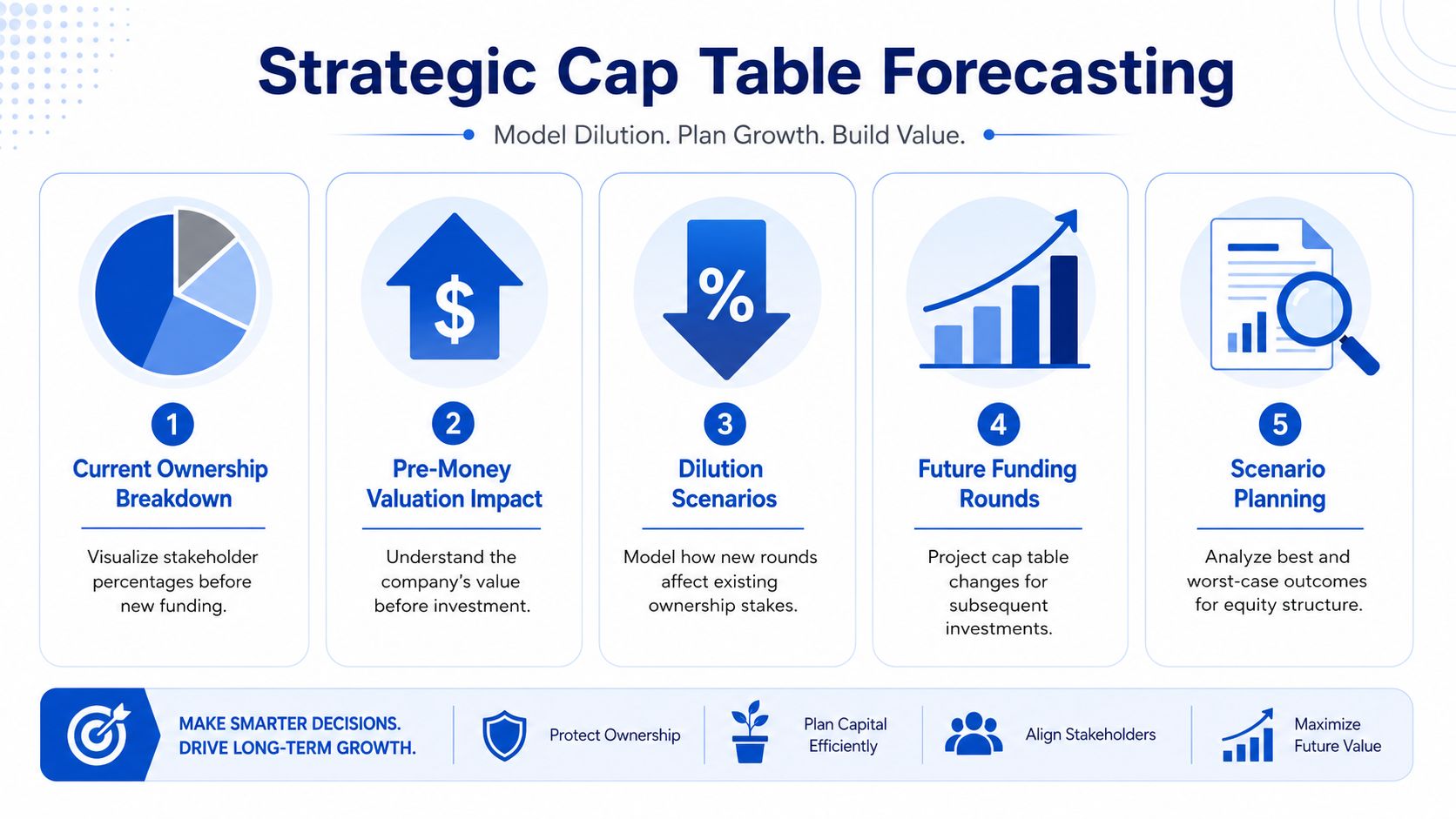

Modeling Dilution and Planning for Future Growth

A cap table earns its keep when leadership uses it before making the next financing decision. Historical accuracy is necessary. It isn’t enough. The company also needs to understand what future rounds, option pool increases, and conversions will do to control and economics.

Dilution modeling starts with a simple question: after new securities are issued, what percentage of the company will each existing holder still own? The answer affects founder influence, investor expectations, hiring capacity, and board conversations.

A clean cap table is directly tied to fundraising speed. Startups with clean cap tables close funding rounds 30% faster than those with discrepancies. The average time to close a Series A is 68 days for a well-managed startup, compared to 99 days for one requiring remediation, and 92% of VCs require a verified cap table before a due diligence meeting. Those figures come from the earlier-cited LTSE best-practices source, and they line up with what investors ask for in practice.

What to model before signing a term sheet

A founder should run at least these scenarios before agreeing to economics:

- New money in. How much ownership shifts if the company raises on the proposed valuation.

- Option pool expansion. Whether the pool increase happens before or after the financing and who absorbs that dilution.

- SAFE and note conversion. What those instruments turn into under the round assumptions.

- Best and worse cases. Not because every edge case will happen, but because financing documents often create them.

For founders trying to sharpen the valuation side of the discussion before translating it into dilution math, this guide to valuing small businesses is a practical refresher on how valuation approaches shape ownership outcomes.

Why software matters here

This is the point where dedicated software usually outperforms a spreadsheet by a wide margin. A spreadsheet can model dilution, but the chance of silent formula errors rises fast as assumptions multiply. Software platforms are better at running alternate scenarios, reflecting fully diluted capitalization, and preserving a record of what assumptions management used.

A short primer on equity dilution and its business impact can also help founders separate emotional reactions from the actual mechanics. Dilution isn’t always bad. Badly understood dilution is bad.

The following explainer is worth reviewing before major financing discussions:

The strategic use of forecasting

Good capitalization table management changes negotiation behavior. A founder who has modeled ownership outcomes can assess whether a lower valuation paired with a smaller pool ask is better than a headline valuation with hidden dilution. The board can also decide whether to hire from the current pool, refresh it now, or wait until after the next milestone.

That kind of planning turns the cap table from a passive record into a decision-making tool.

Maintaining Compliance and Investor Readiness

Investors do not reward last-minute cleanup. They reward companies that already maintain their ownership records as if diligence could begin tomorrow.

The most effective operating habit is a proactive quarterly review cadence. Silicon Valley Bank has recommended that approach to prevent gradual drift and preserve the cap table as an investor-facing audit trail, as explained in LTSE’s discussion of what a capitalization table is. The point of the review isn’t to create paperwork for its own sake. The point is to catch discrepancies while they are still fixable without drama.

What that quarterly review should include

The review should reconcile the cap table against all executed equity documents created since the last cycle. That includes option grants, exercises, terminations, share transfers, SAFEs, notes, board approvals, and any charter changes affecting rights or classes.

It should also confirm that records tied to compliance are current:

- Board approvals for equity issuances and grants

- 409A valuation support for option pricing

- Holder information so dead equity records don’t become diligence obstacles

- Document retention for every event that changed ownership

Investor-facing standard: provide a summary cap table that is transparent about classes, counts, and percentages without casually disclosing every stakeholder detail to every recipient.

Governance is easier when operations are systematized

A well-governed cap table depends on repeatable process. That is one reason founders often pair legal review with operational automation in adjacent finance workflows. For teams thinking about how repeatable documentation reduces manual error across the back office, Matil’s piece on automating financial operations is a useful read.

The same principle applies in corporate governance. If equity decisions are documented consistently, the company can trace how ownership changed and why. If approvals are scattered across email, PDFs, and conflicting spreadsheet versions, the company eventually pays for the disorder.

What investors will expect to see

By the time a company reaches institutional financing, investors usually expect more than a static file. They want to understand the current capitalization, key terms affecting control and economics, outstanding convertibles, available option pool, and any unusual rights or cleanup items. Companies negotiating on standard venture documentation often benefit from knowing how those deal documents fit together under the NVCA model forms framework.

Quarterly discipline does something else that founders underestimate. It reduces the emotional difficulty of corrections. Fixing a missing approval from last month is annoying. Fixing one from two years ago after multiple financings is a transaction risk.

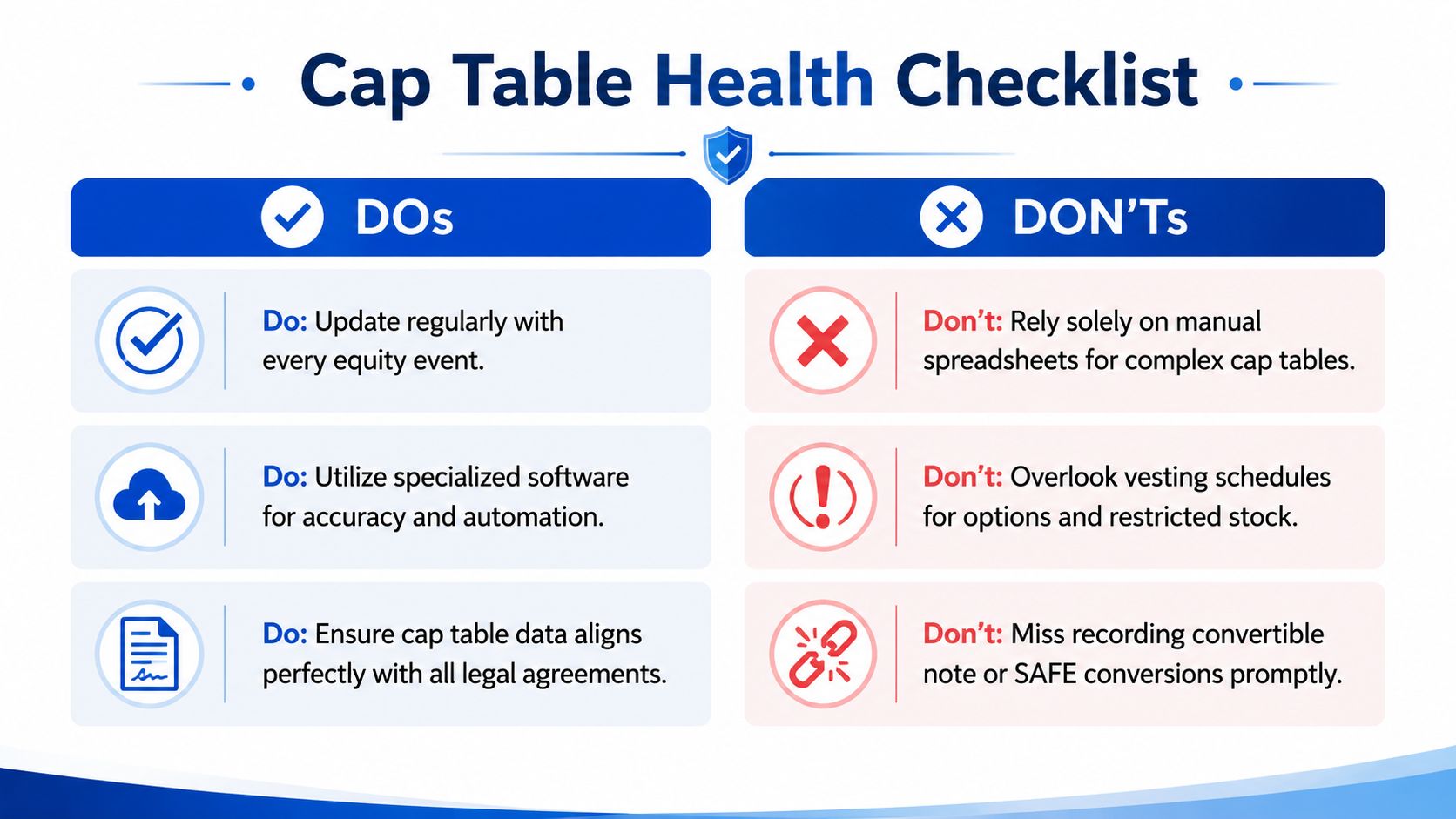

Common Pitfalls and Your Cap Table Checklist

Most cap table disasters don’t start with fraud or exotic structuring. They start with ordinary sloppiness that compounds over time. An option grant is approved but not entered. A SAFE is signed but never reflected in the model. A departed employee still appears to hold unvested equity. Those small misses stack.

Industry veterans have said that “almost every cap table we see has a math error,” often from unadjusted dilution or incorrect vesting, and startups using professional software to enforce reconciliation and maintain accurate records raised 18.4% more capital in 2024 compared to 2023, as noted earlier in the Visible source.

The mistakes that keep recurring

- Math without reconciliation. Percentages may look right while the underlying share counts are wrong.

- Handshake equity. If the grant wasn’t approved and documented, it isn’t cleanly on the cap table.

- Convertible instruments treated casually. SAFEs and notes often sit outside the main file until diligence exposes the omission.

- Departures left unresolved. Forfeitures, repurchases, and post-termination option treatment need to be reflected promptly.

- No single source of truth. Once several versions circulate, no one knows which file controls.

A founder checklist

A cap table is in good shape when the company can answer yes to most of these:

- Every equity event is entered promptly.

- Every entry ties back to an executed legal document.

- Founder vesting and employee vesting are tracked separately from headline ownership.

- SAFEs, notes, and warrants are tracked distinctly until conversion or exercise.

- The fully diluted model is current.

- The option pool reflects what is reserved, granted, exercised, forfeited, and available.

- Quarterly reconciliation happens even when no financing is pending.

- Board approvals and valuation support are easy to produce.

If the company can’t explain its cap table in one clean investor call, it probably can’t defend it in diligence.

Legal counsel becomes essential before a priced round, when drafting or accepting convertible instruments, when creating or refreshing an option pool, and anytime the numbers in the cap table stop matching the signed documents. Cleanup gets harder with every financing event. Early discipline is cheaper than late reconstruction.

Founders who want their ownership records to hold up under fundraising, hiring, and investor diligence can work with By Design Law Firm & Legal Consultancy, PLLC. The firm advises Washington startups and growth companies on entity formation, governance, financing, equity structuring, and the legal systems that keep a cap table clean, audit-ready, and built for long-term growth. Contact our law office today at (206) 593-1519 for a complementary consultation.