An angel just said yes. The founder leaves the coffee meeting feeling like the round is basically done, then opens a browser and finds five different “free” convertible note template downloads that all look similar and say different things.

That's where early fundraising gets sloppy.

A verbal commitment isn't financing. A discussion term sheet isn't financing either. The company gets funded when the business terms are translated into a binding document, signed cleanly, and matched to the company's actual compliance obligations in Washington. That gap between “sounds good” and “wire received” is where founders lose their bargaining power, miss filing steps, and create note terms they don't understand until the priced round arrives.

From Handshake to Term Sheet Your First Funding Step

A common Seattle startup scenario looks like this. A founder gets an email from an angel saying the investor is in for the seed round, subject to “standard note docs.” The founder assumes the rest is administrative, grabs a random convertible note template, forwards it, and waits for signatures.

That's the first legal fork in the road.

A convertible note template is often the fastest way to paper an early investment, but only when the founder understands what belongs in the note and what still belongs in negotiation. The first job isn't to sign. The first job is to convert the investor's verbal yes into a short written summary of business points, then move that summary into a binding note that matches the company's cap table, governing documents, and fundraising plan.

What should happen right after the investor says yes

The founder should lock down the basics in writing before a long-form document goes out:

- Investment amount: The note should state exactly what the investor is buying.

- Conversion economics: The parties should identify whether the deal uses a valuation cap, a discount, or another clearly defined mechanic.

- Timing expectations: The founder should know whether the investor expects a note immediately or wants a short discussion term sheet first.

- Side rights: Pro rata rights, information rights, or MFN rights should never appear as a surprise in the draft.

Founders building companies with strong operator control often benefit from reading Dokly's founder-led companies guide before papering investor rights. It frames the broader governance question that sits behind every early financing document.

The practical next step is getting the startup's investor process organized. A founder who hasn't worked with angels before should also understand how these investors usually approach early deals and diligence, which is covered well in this overview of angel business investors.

Practical rule: If the investor says “send over your standard note,” that doesn't mean the company should send the first template it finds online. It means the company should send a document it can defend clause by clause.

Many free templates skip the transition from non-binding discussion to binding agreement. That's a problem. The investor may think a cap is settled while the founder thinks it's still open. The founder may think sale-event conversion can be decided later. It can't. Once the binding note goes out, ambiguity gets expensive.

A short explainer can help founders get oriented before drafting begins:

Convertible Note vs SAFE Choosing Your Funding Path

Some founders reach for a note because it sounds more serious. Others default to a SAFE because it feels simpler. That's backward. The instrument should match the deal, not the founder's mood.

A convertible note is debt. A SAFE isn't. That one distinction drives most of the actual differences.

According to Adventum Legal, a convertible promissory note functions as short-term debt recorded on the company's balance sheet until conversion, carries a mandatory maturity date that is typically 18–24 months, and accrues interest at 5%–8% per annum, with both principal and accrued interest affecting the eventual equity conversion amount in a trigger event (Adventum Legal's term-by-term guide).

Side by side business differences

| Issue | Convertible note | SAFE |

|---|---|---|

| Legal character | Debt instrument | Not debt |

| Balance sheet treatment | Recorded as debt until conversion | Typically not booked as debt in the same way |

| Maturity pressure | Has a maturity date | No maturity date |

| Interest | Accrues interest | No debt interest feature |

| Investor psychology | Appeals to investors who want a repayment framework | Appeals to speed and simplicity |

That doesn't make the note worse. It makes it more loaded.

When a note makes sense

A founder should lean toward a note when one or more of these conditions exists:

- The investor expects debt features: Some angels want maturity, interest, and a cleaner fallback if the next round doesn't happen.

- The company needs discipline: A maturity date can force a founder to confront timeline risk instead of letting an unresolved SAFE stack drift for too long.

- The round is small and relationship-driven: Notes can work well when a small group of investors is aligned and the company wants one familiar paper set.

When a SAFE is usually cleaner

A founder should usually favor a SAFE when speed matters most and there's no appetite for debt mechanics. A SAFE avoids the maturity cliff and avoids balance-sheet debt treatment, which can matter if the company expects future lenders, grant reviewers, or experienced lead investors to scrutinize liabilities early.

A founder shouldn't ask, “Which document is easier?” The better question is, “Which document creates fewer avoidable problems six months from now?”

The fundamental mistake is mixing instincts. If the founder wants SAFE-style simplicity but accepts note-style terms because the template looked easy to fill in, the company inherits the burden without getting the clarity.

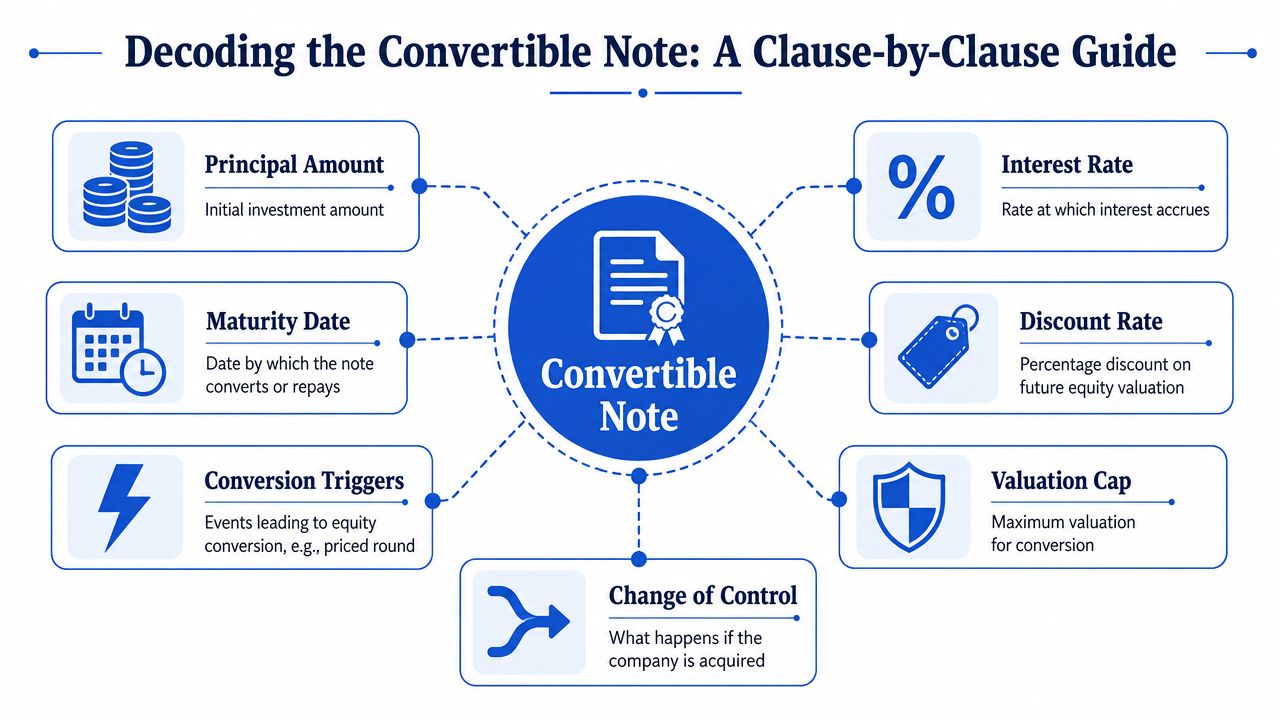

Decoding the Convertible Note A Clause by Clause Guide

The right convertible note template is short. That doesn't mean it's simple. Every short clause carries a cap-table consequence.

Principal amount and why founders underestimate it

The principal amount is the investor's loan amount. Founders tend to treat this as the easy part because it looks fixed and obvious.

It isn't the whole economic story. The note usually converts more than the original wire amount because interest can increase the conversion base. That means the founder shouldn't model dilution from principal alone.

Interest rate and the hidden dilution effect

A note's interest rate isn't just a lender formality. It increases what converts into equity if repayment never happens and the note rolls into the next financing.

Breaking Into Wall Street explains that convertible notes are debt instruments with a maturity date and accrued interest rate, and that the accrued interest increases the principal amount converted into equity, often resulting in greater dilution for founders. That source also notes that where both a discount and a valuation cap are present, the conversion mechanics usually favor the investor's best available share price (Breaking Into Wall Street on convertible notes).

Founders who ignore accrued interest usually discover the dilution when counsel builds the Series A conversion table. That's too late.

Maturity date and the real deadline

The maturity date tells everyone when the debt stops being abstract. If the company hasn't closed a qualifying financing by then, the founder has a negotiation problem, not just a calendar reminder.

The key question isn't whether maturity exists. It's what the note says happens at maturity. A good draft addresses extension, conversion, or repayment pathways clearly. A weak draft leaves everyone arguing over power after the runway is already thin.

Discount rate and what it really buys the investor

The discount rate rewards the investor for writing an earlier check than the next round's investors. The benchmark matters because it gives founders a reality check during negotiation.

Equidam reports that the average discount rate embedded in a convertible note is 32.59%, drawn from 552 distinct data points, and describes that figure as statistically stable. It also explains that this discount lets noteholders convert at a lower price than new investors in the priced round (Equidam's discount rate analysis).

That data matters because a founder hearing “we just want a standard discount” should ask what standard means. Some investors use the word casually. The math is not casual.

Valuation cap and where the leverage sits

The valuation cap is usually the term with the biggest emotional charge because it feels like a proxy for company value. It isn't exactly that. It's a pricing protection mechanism for the investor.

A lower cap gives the investor a better conversion price and increases dilution for the founders. A higher cap preserves more founder upside but may make the note less attractive. That's why founders should negotiate the cap as a financing term, not as a compliment to the business.

Conversion triggers and sale events

A good note defines the events that convert debt into equity. The obvious trigger is the next priced financing. The less obvious trigger is a company sale or other change-of-control event.

If the template is fuzzy here, the company can end up renegotiating under pressure. That's exactly when founders have the least influence.

One working checklist for reviewing the draft

Before a founder sends the draft back, this review list catches most of the practical errors:

- Read the conversion formula: The founder should understand exactly how the conversion price is calculated.

- Check defined terms: “Qualified Financing,” “Maturity Date,” and sale-event language should match the actual deal expectation.

- Model the dilution: The company should run the cap-table effect before signing, not after.

- Compare against market forms: Founders evaluating note language alongside later-round documents can use these NVCA model forms as a useful benchmark for how venture financing documents handle consistency and investor protections.

A note template isn't dangerous because it's legal. It's dangerous when the founder treats legal language as administrative filler instead of pricing logic.

Negotiating Key Terms to Protect Your Equity

A founder doesn't need to “win” every point. A founder needs to protect the cap table from terms that compound badly.

The first hard truth is this. If the investor already has conviction, the company doesn't need to give away every investor-friendly feature in the first draft. That includes stacking an aggressive cap, an aggressive discount, broad MFN rights, and expansive pro rata rights into one note just because the template allowed it.

Cap versus discount

AngelList explains that conversion price is determined by one of two specific mechanics, either a valuation cap or a discount rate, with the discount commonly 15%–20%, and that notes rarely use both simultaneously unless they are explicitly structured as a dual trigger (AngelList's convertible note explainer).

That point should change how founders negotiate. If the investor asks for both a low cap and a meaningful discount, the founder should treat that as a major economic ask, not minor drafting.

A practical negotiating stance looks like this:

- If the cap is founder-friendly: The founder can consider some movement on discount.

- If the discount is investor-friendly: The founder should push back on an aggressive cap.

- If the investor wants both: The company should ask why both are necessary and model the worst-case conversion outcome before agreeing.

Terms that quietly matter later

The note economics get most of the attention, but side rights can age badly.

MFN provisions can drag later concessions back into earlier notes. That can make the next bridge financing harder to structure. Pro rata rights can also become a real issue if too many small investors get them and the company later needs allocation flexibility.

A founder should also watch for any side letter that effectively rewrites the note economics. One “simple” side email about extra participation rights can become a diligence problem in the next round.

Negotiation stance: A founder should trade where the investor values certainty, not where the company loses future flexibility.

For founders trying to understand the downstream effect of these decisions, this explanation of equity dilution gives useful context on how small concessions today can expand in later rounds.

The disciplined move is simple. Keep the note economically coherent. If the investor wants stronger downside protection, the founder should narrow side rights. If the investor wants broad side rights, the founder should defend valuation terms more aggressively. Too many founders concede on all fronts because each point seems small in isolation.

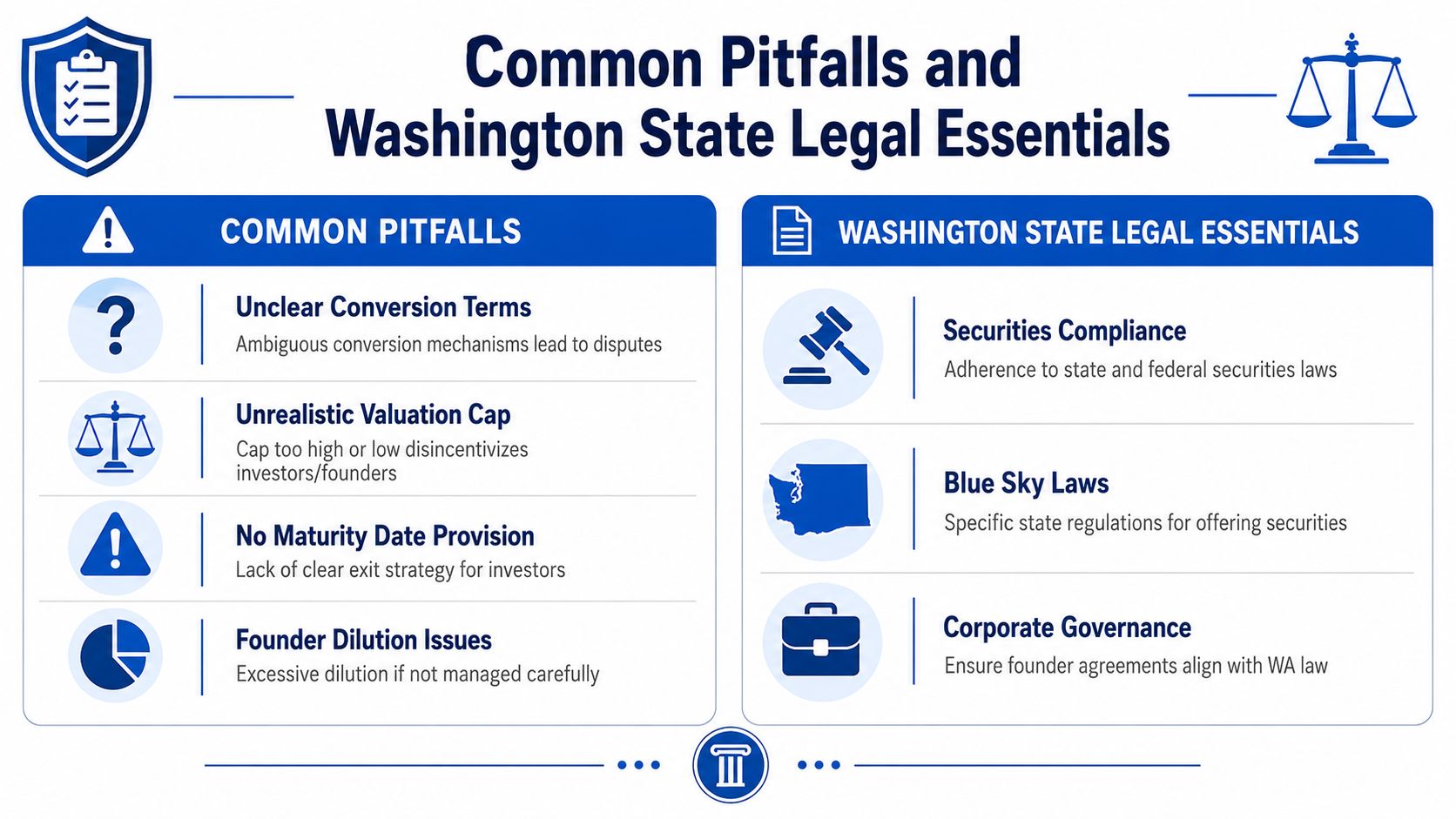

Common Pitfalls and Washington State Legal Essentials

The most expensive phrase in seed financing is “it's just a standard template.”

It usually isn't. It's a borrowed form, adjusted by someone who didn't understand what they deleted.

The market data founders shouldn't ignore

According to the Angel Capital Association model note discussion, seed-round convertible notes reach a 78% success rate in the U.S., but 34% of these deals fail due to common pitfalls such as ambiguous maturity triggers and omitted automatic conversion provisions. The same source notes that modern model notes now require compliance with the Corporate Transparency Act, and that these clauses are absent in 90% of free online templates (Angel Capital Association model convertible note materials).

That's the core warning. A free document may look polished and still be materially outdated.

The mistakes that show up most often

The recurring failures are usually boring. That's why founders miss them.

- Ambiguous qualified financing language: If the note doesn't define what financing size or type triggers conversion, the parties can end up disputing whether conversion was required.

- Missing sale-event mechanics: A company acquisition exposes every drafting shortcut. The note should state what investors receive and how that amount is calculated.

- Weak maturity drafting: If maturity arrives and the note has no clear fallback path, the company negotiates from weakness.

- Terms copied from another company: A founder in Washington shouldn't assume a form built for another jurisdiction fits local filing and governance realities.

Washington State issues founders should handle early

Washington founders need to think beyond the document itself. Securities compliance doesn't disappear because the check came from a friendly angel.

A startup issuing a note should confirm its federal exemption strategy and related filing process, including the Form D path where applicable, and make sure state securities issues are handled consistently with the offering structure. The company should also confirm that its charter documents, board approvals, and stock records line up with the financing.

Corporate Transparency Act compliance deserves separate attention. If the model note package assumes CTA-related obligations and the free template doesn't, that's not a drafting nit. It's a compliance gap.

A clean Washington checklist

A founder in Seattle or anywhere in Washington should insist on these basics before circulating signature copies:

- Board approval is documented: The company should approve the financing formally and keep the record organized.

- Security exemption analysis is confirmed: The financing should fit a valid exemption path.

- CTA implications are reviewed: The company should understand whether beneficial ownership reporting or related updates are triggered.

- Cap table records are current: Every note and side letter should match the company's internal records.

- Closing packet is complete: Signed note, resolutions, investor information, and payment records should live in one place.

The companies that get punished in diligence aren't usually the ones with bad businesses. They're the ones with missing approvals, inconsistent paper, and mystery investor rights.

What Happens at Maturity Answering the Hard Questions

The question founders avoid is the one they should negotiate before signing. What happens if the company reaches maturity without a priced round and without cash to repay the note?

That scenario feels dramatic when the note is signed. Later, it feels ordinary. Startups miss timelines all the time.

What usually happens in practice

Cooley GO addresses the question directly. Founders regularly ask what happens if they can't repay a convertible note at maturity, and while the notes are unsecured debt, the default scenario rarely involves litigation. Investors often negotiate extensions or automatic conversions instead, and most templates don't include enough flexibility for that outcome (Cooley GO FAQ on convertible debt).

That should reset the founder's thinking. Maturity is less about courtroom drama and more about advantage, relationship quality, and pre-drafted options.

The common outcomes

When a note reaches maturity, these outcomes usually dominate the conversation:

Extension of maturity

The investor gives the company more time. In exchange, the investor may ask for revised economics or a cleaner reporting cadence.Conversion under an agreed formula

The parties agree that the note converts into equity based on the note's existing mechanics or a negotiated substitute.Hybrid solution

Part of the note remains outstanding while the rest converts, or the extension is paired with an amendment on one economic term.

What matters is whether the original note anticipated any of this. If it didn't, every decision becomes bespoke under pressure.

How founders should prepare before maturity hits

A founder should start the maturity conversation early, while there's still room to negotiate rationally.

- Review the note before the deadline: The company should know exactly what rights already exist.

- Bring a current cap table: Investors respond better when the company can show the full conversion effect clearly.

- Offer a realistic path: If the company needs an extension, it should explain what milestone or financing process makes the extra time meaningful.

- Avoid casual email amendments: Material changes should be documented properly.

For founders trying to understand what investors may receive if the note converts into a later preferred round, this overview of preferred stock helps connect the note stage to what comes next in venture financing.

“Repayment at maturity” is often the legal default. It isn't usually the commercial outcome.

The smart founder doesn't wait to discover that the template lacked flexibility. The smart founder spots that issue before signature and builds in a realistic path for extension or conversion.

By Design Law Firm & Legal Consultancy, PLLC helps Washington founders turn investor interest into clean, enforceable financing documents that match real startup operations, compliance requirements, and long-term fundraising strategy. Companies that want practical legal support on convertible notes, startup financing, governance, contracts, IP, privacy, and technology matters can learn more at By Design Law Firm & Legal Consultancy, PLLC.