The email arrives, the partner says the firm is excited, and a term sheet is attached. For many founders, that feels like the hard part is over.

It isn't. The term sheet is often the moment when venture capital due diligence becomes real, intrusive, and time-consuming. Investors stop evaluating the story and start testing whether the company can withstand scrutiny across finance, legal, product, governance, and founder judgment.

Founders who treat diligence as a document dump usually create delay. Founders who treat it as an operating test usually move faster. That's the practical shift that matters. Venture capital due diligence is no longer just an investor checklist. It is one of the clearest ways a company can demonstrate discipline, maturity, and readiness for outside capital.

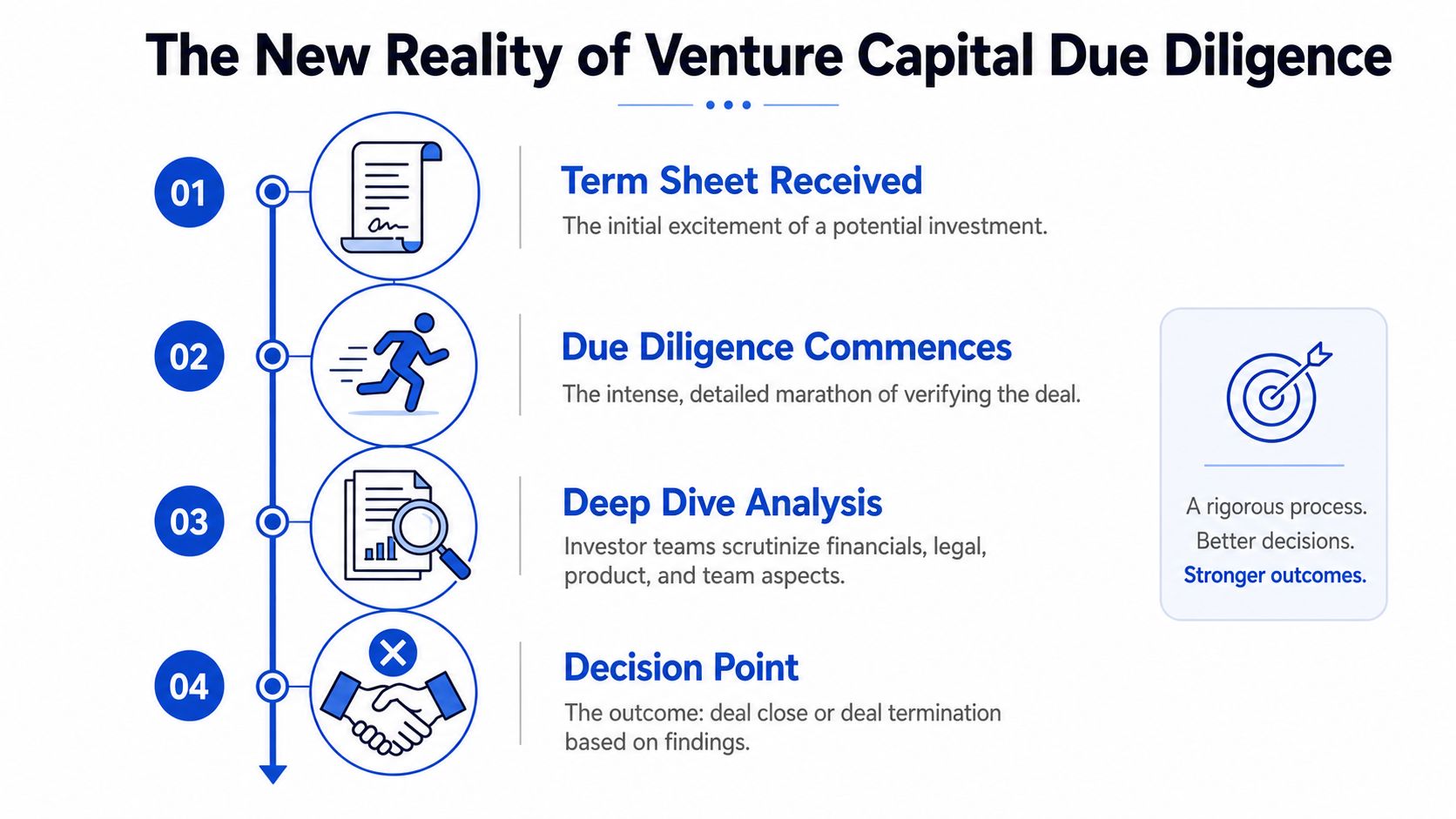

The New Reality of Venture Capital Due Diligence

A signed term sheet used to signal a relatively short path to closing. In the current market, it more often signals the start of a deeper review. Investors are taking longer, asking narrower questions, and pressing harder on proof.

According to OMERS Ventures on the shifting VC landscape, over 33% of VC firms now spend more than 5 weeks on any single new deal, and there has been a 38% increase in focus on customer diligence. That combination matters. It means the diligence process is not just slower. It is aimed more directly at whether the company's customer story holds up.

Why investors are pressing harder

This change reflects a more cautious investment environment. Investors want to understand not only whether a business can grow, but whether the growth assumptions are tied to verifiable customer behavior, sound go-to-market execution, and a management team that can handle pressure.

Recent regulatory attention has also sharpened the backdrop. A 2025 Columbia Law School Blue Sky commentary, discussing post-FTX enforcement pressure and broader gatekeeping concerns, describes how diligence can suffer when investors rely on reputational shortcuts instead of independent verification. That's part of why founders should expect more direct requests for support on revenue quality, customer contracts, compliance, and governance.

Due diligence now functions less like a final formality and more like a stress test of the company's internal controls.

What founders should take from that shift

The practical implication is simple. A founder should assume that almost every material claim will be checked, and that “we can get that later” creates friction. This is especially true for companies raising their first major round, where institutional investors are often evaluating not just the business but the management habits behind it.

A founder who needs a broader refresher on managing finances through startup funding will benefit from understanding how each stage changes investor expectations. The legal side of that readiness shows up quickly in a disciplined due diligence checklist for founders, because investors rarely separate legal hygiene from commercial credibility.

The opportunity hidden inside the process

The strongest founders don't wait for diligence to expose weaknesses. They use diligence to show that the business is run with the same care investors will later expect in board reporting, approvals, security practices, and contract management.

That mindset changes the tone of the deal. Instead of looking like a company scrambling to answer questions, the business looks like a company already prepared to operate with institutional capital.

Building Your Impeccable Virtual Data Room

A virtual data room is not an administrative afterthought. It is evidence. Before an investor speaks to a customer or reviews a contract, the data room tells them whether management is organized, careful, and transparent.

That impression forms fast. Under the standard framework described by Qubit Capital's VC due diligence checklist, investors evaluate four essential core areas: financial health, team strength, market fit, and legal compliance. The same source notes that a clean cap table is one of the fastest deal accelerators or killers in the process. That statement aligns with what counsel sees repeatedly in practice. Sloppy ownership records create distrust far beyond the cap table itself.

Start with structure, not volume

A messy room with 300 files is worse than a smaller room with precise organization. Investors and their counsel don't want to hunt. They want a folder structure that mirrors the way they review risk.

A useful model for founders comes from the M&A world, where sellers use virtual data rooms to reduce buyer friction. For a practical primer on how those platforms are used in transactions, this overview of a VDR for selling a business is helpful because the same principles apply in venture deals: permission control, version discipline, and clean indexing.

A founder-ready folder map

The room should have top-level folders that reflect actual diligence workflows.

Corporate

- Certificate of formation or incorporation

- Bylaws or operating agreement

- Board and stockholder consents

- Subsidiary records, if any

- State qualification filings

Capitalization and securities

- Current cap table

- Stock ledger

- SAFEs, convertible notes, warrants

- Equity incentive plan documents

- Option grants and board approvals

- Prior financing documents

Financial

- Historical financial statements

- Current budget

- Cash flow materials

- Bank statements

- Tax filings

- Debt documents, if any

Commercial

- Revenue summary by customer

- Standard customer contract form

- Top customer agreements

- Pipeline materials used in fundraising

- Churn or retention analyses, if maintained internally

Legal and compliance

- Material contracts

- Employment and contractor agreements

- Insurance policies

- Privacy policy and terms of use

- Regulatory correspondence, if any

- Any template non-disclosure agreement guidance used with employees, contractors, or counterparties

Intellectual property and product

- Trademark, copyright, patent, and domain records

- IP assignment agreements

- Open-source software policy, if one exists

- Product architecture overview

- Security policies and incident response materials

Essential Virtual Data Room Document Checklist

| Category | Key Documents |

|---|---|

| Corporate | Formation documents, bylaws or operating agreement, board and stockholder consents |

| Capitalization | Current cap table, stock ledger, SAFEs, notes, warrants, option plan and grants |

| Financial | Financial statements, budget, cash flow materials, bank statements, tax filings |

| Commercial | Standard customer forms, major customer contracts, revenue support, pipeline materials |

| Legal and compliance | Material contracts, employment and contractor agreements, insurance, policies |

| Intellectual property and product | IP registrations, assignments, product documentation, security and governance materials |

What makes a data room credible

Completeness matters, but internal consistency matters more. The board consent should match the equity issuance. The option grant should match the cap table. The contractor agreement should contain the same IP assignment assumptions the company is making in pitch meetings.

Practical rule: If two documents answer the same question differently, investors will assume the less favorable answer is the true one until proven otherwise.

Founders should also name files clearly, lock down outdated drafts, and keep an index of what has been uploaded. If a company uses DocuSign, Carta, Google Drive, Dropbox, SharePoint, or Notion internally, that's fine. But the diligence room itself should present a single controlled source of truth. A room that anticipates investor questions often shortens the back-and-forth before those questions even arrive.

Mastering the Core Diligence Pillars

Once the data room is built, investors start reading for signal. They are not just checking whether documents exist. They are asking what those documents reveal about judgment, control, and execution risk.

Financial diligence means testing assumptions

Investors want more than a spreadsheet. They want to know whether revenue projections, burn assumptions, and runway claims are grounded in actual operating facts. The legal issue here is often disclosure discipline. If a company has presented one growth narrative in the pitch deck and another in the budget model, the discrepancy will surface.

Strong founders make it easy to reconcile:

- Revenue logic should tie to signed contracts, renewals, or a clearly described pipeline methodology.

- Cash position should match bank records and debt obligations.

- Burn analysis should show where management can cut, delay, or restructure spend if the market changes.

The dangerous pattern is not aggressive forecasting by itself. It is unsupported forecasting.

Legal and IP diligence reveals hidden liabilities

Legal diligence is where many young companies discover that fast execution left gaps. Investor counsel will review formation records, board approvals, material contracts, employment arrangements, litigation exposure, and intellectual property ownership.

Trade secrets deserve special care. If the company's value depends on proprietary processes, models, code, or customer insights, it should be able to show a coherent protection framework. A practical resource on protecting trade secrets is useful here because investors do not treat “confidential” as a substitute for process.

Three term sheet provisions also deserve immediate attention because they can reshape economics and control. CRV's due diligence checklist highlights full ratchet anti-dilution clauses, investor veto rights over key company decisions, and participating preferred stock with higher liquidation multiples as terms founders should scrutinize carefully during the diligence and deal review process.

A founder should assume that every missing signature, every vague IP assignment, and every side letter will be read as a governance signal.

Product and technical diligence asks whether the company can scale safely

Investors usually bring product, technical, or operating advisors into this part of the review. They want to understand what has been built, how defensible it is, and what risks are embedded in the architecture.

That review often includes:

- Code and architecture clarity: whether the system is maintainable and understandable.

- Dependency risk: reliance on key vendors, open-source components, or a single engineer.

- Security and data governance: whether the company knows what data it holds, where it sits, and who can access it.

For companies with heavy contract volume, converting legal and technical materials into a searchable format can reduce friction internally before the investor review begins. This guide to AI review for legal markdown conversion is a practical example of how teams are making dense legal material easier to analyze across functions.

A short explainer on the investor lens is useful here:

Team diligence is more searching than most founders expect

This is the pillar founders routinely underestimate. According to TechCrunch's reporting on VC due diligence, 60% of early-stage deals collapse post-screening due to founder-VC misalignment, yet only 12% of due diligence checklists include structured behavioral assessments. That means investors say team quality matters, but many founders still don't prepare for how informally and intensely that judgment is made.

Investors will look for:

- Decision-making under stress

- Founder alignment on strategy and control

- Communication habits with difficult stakeholders

- Willingness to hear bad news early

- Coachability without fragility

This part of diligence rarely arrives as a formal memo request. It shows up in repeated meetings, reference calls, reactions to negotiation pressure, and whether the founders answer hard questions directly. The company may have an excellent product and still lose the deal if the investor believes the working relationship will break under strain.

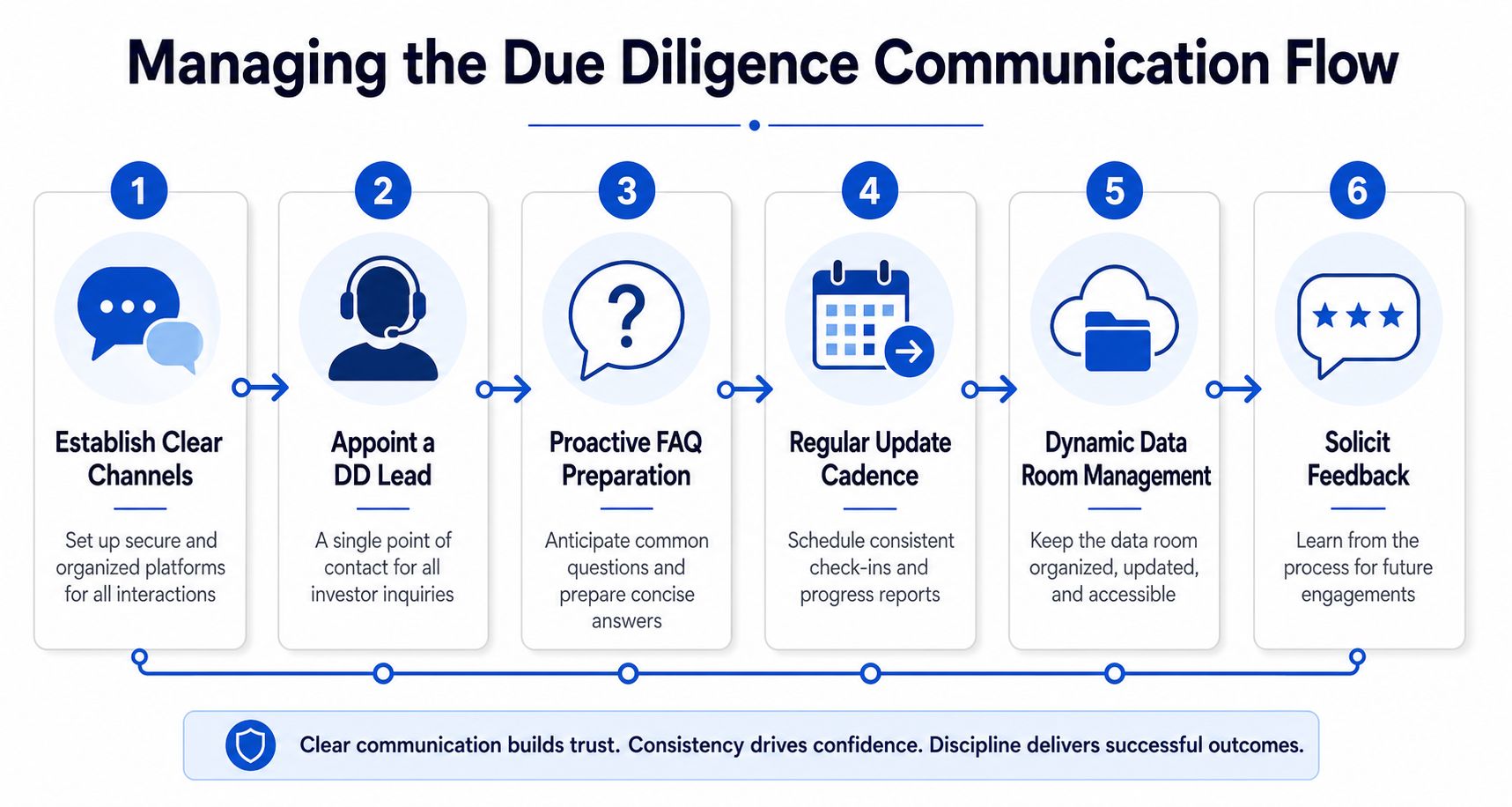

Managing the Due Diligence Communication Flow

Diligence stalls less often because of one catastrophic issue than because of poor process. Questions get answered by the wrong person. Files are sent over email instead of uploaded centrally. One investor request leads to three inconsistent responses from finance, product, and counsel.

The cleaner approach is to treat diligence like a transaction workstream with one owner, one tracker, and one record of truth. That matters even more because the process itself has two distinct phases. The VC Factory's analysis of why venture capital due diligence fails describes exploratory due diligence as the pre-term-sheet phase used to spot red flags, and confirmatory due diligence as the post-term-sheet phase for detailed verification. The same source states that experts recommend 40% to 50% of time be allocated to financial and legal fundamentals during this phase.

Build a communication system before the questions multiply

The best diligence processes are boring. Requests come in, they are logged, ownership is assigned, supporting documents are uploaded, and the response goes out in a controlled format.

A workable founder process usually includes:

- Single diligence lead: one executive, often the CEO, COO, or finance lead, who triages all requests.

- Shared request tracker: usually in Airtable, Notion, Google Sheets, or Excel.

- Central response rule: final answers are delivered from one channel, not from side emails.

- Counsel escalation line: legal questions go to counsel early, not after a partial answer has already created confusion.

Match the response to the question

Not every question deserves a long memo. Some require a document, some require a short explanation, and some require a controlled call with counsel present. Founders often lose momentum by over-answering simple requests and under-answering serious ones.

A useful internal rule is to classify each request:

- Document request

Upload the document and provide a one-sentence description. - Clarification request

Answer directly, then cite the supporting file. - Issue request

Describe the problem, current status, and remediation plan. - Sensitive request

Route through counsel before responding.

Response discipline: Fast is helpful. Consistent is better. Accurate is non-negotiable.

Keep momentum without sounding defensive

Investors do not expect a perfect company. They do expect a company that can identify issues, explain them clearly, and fix them responsibly. If a customer contract is unsigned, say so and explain whether performance has started, whether payment has been received, and what correction is underway. If a board consent was missed, disclose it and get the cleanup process moving.

Weekly diligence update emails can help when the process gets heavy. They should be short and factual: documents added, open items, anticipated timing, and any item requiring discussion. That cadence reduces duplicate requests and shows management is in control of the process rather than reacting to it.

Sidestepping Deal-Killing Red Flags and Pitfalls

Many founders assume deals fail in diligence because investors discover dramatic fraud, hidden lawsuits, or a catastrophic product problem. Those things happen, but the more common cause is simpler. The company made claims it could not support, or it let small governance failures pile up until they looked systemic.

That pattern is visible in the data. According to AInvest's analysis of venture capital diligence inefficiencies, traditional diligence often misses up to 73% of startup failure signals, and 80% of new founders fail their first diligence attempt due to unverified assumptions. The practical lesson isn't that diligence is broken beyond repair. It's that founders must verify their own story before an investor starts doing it for them.

The red flags that surface fastest

Some problems signal disorder immediately.

Unverified commercial claims

If pipeline statements, retention claims, or customer concentration narratives cannot be tied to actual records, investors start discounting management credibility.Ownership ambiguity

Missing stock issuances, unsigned option paperwork, unclear SAFE treatment, or informal founder transfers create avoidable friction.IP uncertainty

Contractors who built code without assignment language, brand assets used without clear ownership, and undocumented open-source practices can all become material concerns.Leadership inconsistency

If founders tell different stories about priorities, fundraising use of proceeds, or hiring plans, investors infer conflict even if no conflict is admitted.

Neutralize risk before the investor names it

Founders do not need a flawless business. They need a company that can identify weaknesses and address them in an orderly way.

A practical pre-diligence audit should include:

- Sampling key relationships: review a slice of customer contracts, vendor agreements, and employment arrangements for signature, term, assignment, and termination issues.

- Reconciling core statements: make sure the pitch deck, financial model, CRM reports, and board materials do not contradict one another.

- Checking governance records: board consents, stock approvals, and option grants should align with the actual cap table and ledger.

- Documenting known issues: if a problem exists, prepare a short memo explaining the exposure and remediation path.

Investors can live with risk. They have trouble with surprise, inconsistency, and denial.

What doesn't work

Three founder habits regularly undermine otherwise financable companies.

First, sending “draft” materials as if they were final. A draft customer agreement with no signatures is not proof of revenue quality. Second, answering legal questions with commercial optimism. “That should be fine” is not an answer to an IP chain-of-title problem. Third, hiding minor defects out of fear they will derail the deal. Concealed issues age badly. Disclosed issues with a remediation plan are often manageable.

A disciplined company runs its own mock diligence before the investor starts. That means testing assumptions, reconciling records, and asking whether an outsider could understand the business from the evidence alone. If the answer is no, the company has work to do before the financing process reaches full speed.

Turning Diligence into a Strategic Advantage

The strongest founder posture is not defensive. It is operational. Venture capital due diligence gives a company a chance to prove that management can run more than a product roadmap. It can run a corporation.

That matters long after closing. The habits built during diligence become the habits that shape board communication, approval workflows, investor updates, compliance responses, and future financings. A clean room, a coherent response process, and credible disclosure discipline tell investors that the company will likely be easier to govern after the money arrives.

This is also where capitalization discipline pays off. A company that understands its ownership record, approvals, and securities history will avoid avoidable delay and negotiate from a clearer position. Founders who need to tighten that area should understand the basics of capitalization table management before the next round begins, not after counsel for the lead investor starts asking questions.

Done well, diligence becomes more than a hurdle. It becomes the company's first serious demonstration of institutional readiness. That is often what separates a promising startup from a fundable one.

By Design Law Firm & Legal Consultancy, PLLC helps startups and growth-stage companies prepare for financing with practical counsel on corporate records, contracts, intellectual property, data governance, and transaction readiness. Founders who want legal guidance that is clear, business-minded, and built for execution can learn more at By Design Law Firm & Legal Consultancy, PLLC.