A founder closes the laptop after reading a term sheet and realizes the valuation wasn't the only negotiation that mattered. Buried in the governance section are board seats, approval rights, and a chair structure that will shape who gets heard when the company misses plan, hires a new executive, or handles a security incident. For many Washington startups, that's the moment the board stops being a formation checkbox and becomes a power map.

That shift happens early. A company may still be refining product-market fit, but one financing round can change the conversation from “Who incorporated the company?” to “Who controls board votes?” and “Who approves the next financing, equity plan, or CEO package?” Founders who treat board design as an afterthought often discover too late that a bad structure slows decisions, confuses authority, and creates avoidable friction between management and investors.

A strong board of directors structure does the opposite. It gives the company oversight without paralysis, expertise without micromanagement, and accountability without constant drama. That matters even more in Washington's tech market, where startups move quickly, compliance questions arrive early, and governance often has to catch up with fundraising, hiring, product launches, and data risk.

The practical problem is that most advice on boards is either too generic or too public-company oriented. A Seattle founder raising a seed or Series A round doesn't need abstract theory. The founder needs to know what Washington law requires, how many directors make sense right now, what to put in bylaws, how voting rules work, and how to keep the board useful between meetings. Founders reviewing NVCA model forms and venture financing documents can see how quickly these issues become contractual, not merely conceptual.

Introduction From Term Sheet to Boardroom

A venture financing usually changes three things at once. It adds capital, adds expectations, and adds people who believe they have earned a say in strategy. The board is where those expectations collide.

One founder may want a three-seat board with two founders and one investor. Another investor may push for a fifth seat and an independent director acceptable to both sides. Neither position is automatically right. The right answer depends on control, stage, trust, and whether the company needs operational help, governance discipline, or both.

Why the structure matters immediately

A board isn't just the group that approves annual budgets and signs off on major transactions. It becomes the place where a startup tests whether its governance can keep pace with growth. A sloppy structure often produces familiar problems:

- Deadlocked votes: Even-numbered boards can create avoidable stalemates.

- Unclear authority: Directors drift into management decisions because nobody set boundaries.

- Weak oversight: Friends of the founders may support management but fail to challenge risky decisions.

- Investor frustration: Board observers and directors often receive inconsistent information, which breeds distrust.

Practical rule: The best startup boards are small enough to decide, but broad enough to challenge.

Board design is strategy, not paperwork

In Washington companies, board structure also sits next to real legal mechanics. Corporate law, bylaws, shareholder arrangements, officer appointments, and state filings all interact. That's why founders shouldn't separate “fundraising terms” from “governance terms.” The term sheet often starts the legal architecture that will govern the company for years.

For tech companies, the board's role now reaches well beyond finance. Directors are expected to engage with hiring risk, product risk, cyber risk, regulatory issues, and increasingly AI-related oversight. A board that fits the company at formation may become dysfunctional after the first institutional round unless the company updates composition, cadence, and committee practices.

The useful question isn't whether the company needs a board. A Washington corporation either needs one or must lawfully allocate those duties elsewhere. The better question is whether the company is building a board that can help it survive pressure.

The Legal Blueprint Washington State Requirements

A Washington founder usually feels the legal pressure on board structure at an inconvenient moment. The certificate has been filed, stock is about to be issued, an investor asks for board approval language, and nobody can say with confidence who has authority to act for the company. That problem starts early, in the formation documents.

Under RCW 23B.08.010, every Washington corporation must have a board of directors with at least one individual, unless the articles of incorporation or a shareholders' agreement lawfully shifts those functions elsewhere under Washington's Revised Corporation Act.

That gives a startup room to start lean. It does not permit vagueness.

If the company will operate with a board, the governing documents should say the exact number of directors or give a clear method for setting that number. I often see founders leave this loose because everyone agrees, at formation, on who is in charge. The trouble comes later, when a financing, bank resolution, option grant, or founder departure forces the company to prove who had authority on a particular date.

What should be in place at formation

Washington corporations should have these items aligned from the beginning:

- Board authority: The company needs at least one director unless valid governing documents assign those duties elsewhere.

- Bylaws: Washington corporations are expected to adopt bylaws, typically through the incorporator or the initial board, to govern internal procedures and decision-making, as outlined by the Washington Secretary of State's corporation formation guidance.

- Director number or formula: The bylaws or articles should state the number of directors or the process for fixing that number.

- Officer roles: The company should identify who is serving in the statutory officer functions, even if the startup uses business titles that sound less formal.

- Consistency across documents: Articles, bylaws, stock issuance records, shareholder agreements, and early resolutions should all point to the same governance structure.

This is one place where founders who previously ran LLCs get tripped up. A corporation has more formal approval mechanics, and those mechanics matter once you issue stock or split authority among founders and investors. Founders comparing entity types often miss that difference until they review the governance consequences described in these Washington LLC operating agreement considerations.

The filing deadline that exposes weak governance

Washington also requires an early public filing step that forces these decisions into the open. A corporation must deliver its initial report to the Secretary of State, and that filing identifies the company's registered agent and principal leadership roles, as reflected in the Washington Secretary of State's annual and initial report instructions.

For startups, that requirement does more than satisfy a filing rule. It tests whether the company has assigned responsibility. If no one knows who is acting as secretary, or the founders disagree about whether a board chair exists, the reporting issue is usually a symptom of a broader governance failure.

Where Washington startups make avoidable mistakes

The common problem is not deliberate noncompliance. It is casual drafting and casual implementation. Founders pull bylaws from Delaware forms, keep Washington-specific exceptions out of the shareholder documents, or approve major actions by email without checking what the bylaws permit.

Small g governance matters here as much as legal form. A startup can technically have the right documents on paper and still create risk if directors are unclear about who decides what, officers do not maintain minutes or written consents, and major approvals are handled informally because the team is moving fast. That is how cap table disputes, invalid approvals, and investor diligence problems start.

A Washington corporation can stay lean at the start, but it cannot stay vague.

The fix is practical. Match the articles, bylaws, shareholder arrangements, officer appointments, and board resolutions from day one. If the plan is to begin with one director and expand after a priced round, write that transition into the documents and approval process before the pressure arrives.

Building Your Board Size and Composition

Board size should fit the company's stage. A two-founder software startup and a public company don't need the same architecture, and trying to borrow the public-company model too early usually creates drag.

For public companies in the United States, the average board size has converged at approximately 8.5 directors, with independence reaching 77.5% as of 2024, while private companies often keep boards at three to seven directors, with odd-numbered boards preferred to avoid deadlocks, according to research on board size and independence. That split reflects a practical truth. Mature companies need broader oversight and committee depth. Startups need speed, trust, and a limited number of decision makers.

What early-stage companies need

A seed or Series A company usually benefits from a compact board that includes the people who carry financing, operating, and governance weight. In practice, that often means founders, a lead investor, and one independent director once the company reaches the point where outside judgment adds value.

For startups and mid-sized technology companies, a lean insider-independent hybrid of five to seven members, including a CEO and at least three independent directors with expertise in cybersecurity, IP, or AI law, is described as an effective model in Esade's discussion of board duties and composition. That doesn't mean every seed-stage company should immediately install seven directors. It means founders should think in terms of capability, not status. If the company handles sensitive data, one independent director with real security judgment may be more valuable than another investor seat.

Comparison by stage

| Attribute | Early-Stage Startup (Seed/Series A) | Established Public Company |

|---|---|---|

| Typical size | Small, usually built for speed and direct engagement | Larger, built for oversight and committee coverage |

| Main participants | Founders, lead investor, selected independent voice | Mostly independent directors plus executive leadership |

| Core objective | Fundraising support, strategic guidance, disciplined decision-making | Formal oversight, compliance, succession, risk governance |

| Meeting style | Direct, operationally informed, tightly focused | Structured, committee-driven, process-heavy |

| Main risk | Overpersonalized governance or investor-founder deadlock | Slow decisions and diluted accountability |

A founder should also model board composition alongside dilution and control. Governance and economics aren't separate tracks. Board seats often track financing influence, protective provisions, and future rounds, which is why cap table planning and board planning belong in the same conversation when reviewing capitalization table management issues.

What works and what doesn't

What works is an odd number of directors, clearly chosen for role coverage. A founder-director carries company context. An investor-director brings financing perspective. An independent director can challenge both sides when emotions rise.

What fails is the “everyone important gets a seat” model. That creates a board that is too large for a startup and too under-structured for a public company. It also creates divided loyalties. A customer representative, a friendly adviser, and multiple small investors may all be valuable stakeholders, but they don't all belong on the board.

A startup board should be built around decisions the company must make in the next stage, not honors for people who helped in the last one.

Another mistake is treating independence as symbolic. A true independent director shouldn't function as a tiebreaker controlled by management or investors. The value comes from judgment, not neutrality theater.

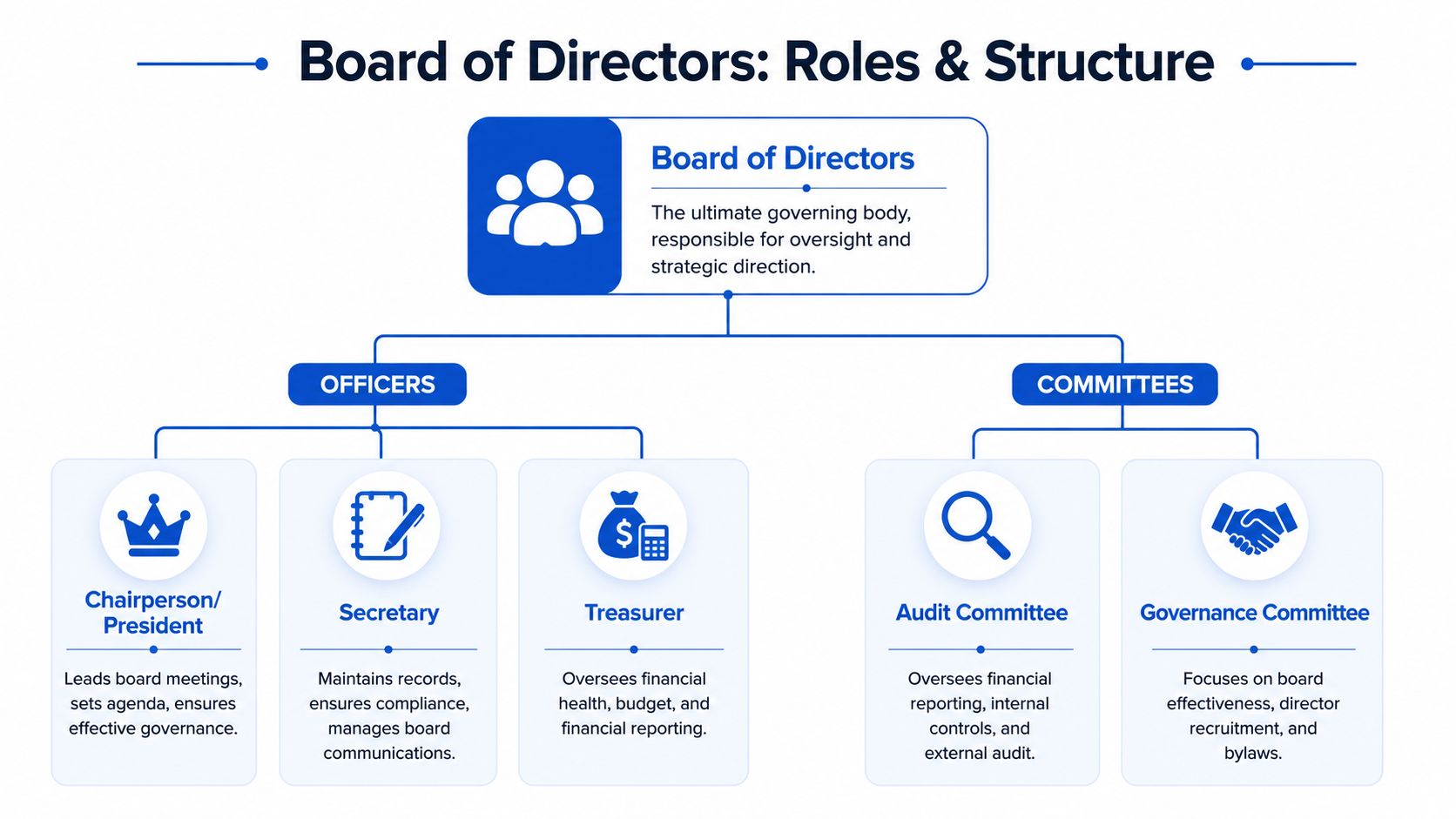

Key Roles Responsibilities and Committees

The board meeting starts in ten minutes. The financing documents are signed, the company is hiring fast, and a director asks who is responsible for approving the option pool increase, documenting the related-party contract, and deciding whether a data security issue belongs with management or the board. If nobody can answer cleanly, the problem is not the people. It is the structure.

A board works only when authority is allocated on purpose. Under Washington law, the board manages the business and affairs of the corporation, subject to any limits in the articles of incorporation or a shareholder agreement, as reflected in RCW 23B.08.010. For founders, that legal rule has a practical consequence. Titles, committee assignments, and officer duties should be set early enough that major decisions do not turn into ad hoc negotiations.

A simple organizational picture helps:

Chair CEO and independent directors

The chairperson controls board process. That includes setting agendas, deciding what gets queued for discussion or formal action, and making sure directors receive materials with enough time to review them. In a Washington startup, the chair also shapes the small g governance culture. A disciplined chair creates space for disagreement, keeps minutes tied to actual resolutions, and prevents the meeting from drifting into management status updates with no corporate action.

The CEO runs the company day to day, but does so under board oversight. Good CEOs give directors the information needed to exercise judgment, including bad news, assumptions behind forecasts, and areas where management wants a decision instead of informal feedback. Founders often miss this trade-off. The same person may be best positioned to lead the business and least well positioned to referee the board's supervision of management.

The independent director provides separation where startup boards usually lack it. Independence is less about optics than function. An effective independent director can press for cleaner conflict handling, ask whether a financing process was fair to common stockholders, and insist that risk oversight be assigned to a person or committee instead of left in the air. That matters in Washington companies because fiduciary decisions are judged from the record the board creates, not from assumptions about everyone's good intentions.

Comparative models are useful here. In some countries, oversight and management sit in separate bodies, and employee representation is built into board design, as summarized in the overview of board models and governance practice. A Washington startup will usually operate with a single board, so separation has to be built through role clarity, meeting discipline, and independent judgment.

Committees that matter as the company grows

Most early-stage companies do not need three standing committees on day one. They do need clear responsibility for recurring issues that carry legal or financing risk.

The audit committee usually takes first responsibility for financial reporting, internal controls, related-party transactions, and oversight of the outside accountants. In a private startup, that committee may be informal at first. Once revenue grows, debt enters the picture, or investor reporting becomes more demanding, informal oversight stops working well.

The compensation committee handles executive pay, bonus metrics, and equity awards. Avoidable mistakes are often observed in this area. If the full board casually approves founder compensation or option grants without a defined process, the company creates trouble for diligence, tax review, and future fairness questions.

The nominating and governance committee handles board refresh, director recruitment, onboarding, and governance housekeeping. In practice, this committee often becomes the place where a company decides whether an observer should become a director, whether a founder-chair arrangement still makes sense, and whether the board has the expertise to oversee AI, privacy, or regulated product issues.

For boards that want a practical comparative framework outside the U.S. market, Lighthouse's framework for UK boards is useful because it ties roles, reporting, and risk to actual board work rather than abstract governance theory.

Specialized committees can also make sense. A software company with meaningful cybersecurity exposure may assign privacy and security oversight to the audit committee or create a risk committee if the issue load justifies it. A life sciences company may need clearer board-level handling of clinical, regulatory, or scientific oversight. The right choice depends on where a mistake would be expensive, hard to reverse, or likely to attract investor scrutiny.

This short explainer is worth watching before assigning titles and committee work:

The internal power structure founders should respect

The secretary and treasurer are often treated as leftover titles from a form book. That is a costly habit.

The secretary is usually the keeper of process. Notices, minutes, written consents, board records, and corporate books often run through that office, even when outside counsel helps. If the secretary function is weak, the company can have valid decisions in substance but a poor paper trail when investors, auditors, or opposing counsel ask for proof.

The treasurer role varies more in startups, especially where a CFO or finance lead carries the primary workload. Still, the function matters. Cash reporting, reserve planning, debt compliance, and board-level financial accuracy have to belong to someone. If nobody owns that discipline, directors cannot exercise oversight with confidence.

Governance usually breaks first in the records, then in working relationships, and then in control.

Founders should treat role design as operating infrastructure, not ceremony. Clear assignments reduce conflict, improve board judgment, and make the company easier to finance, diligence, and defend.

The Governance Engine Bylaws Voting and Cadence

A Washington startup often discovers its governance problems during a stressful vote, not during drafting. A financing is ready to close, one director misses the meeting, another objects to the notice, and nobody is sure whether the board can act by written consent. At that point, the issue is no longer theory. It is delay, bargaining advantage, and preventable cost.

Bylaws are where that risk gets controlled. Under the Washington Business Corporation Act, the board and shareholders operate within a statutory framework, but the corporation still needs clear internal rules for meetings, quorum, officer authority, and board action. Washington law permits bylaws to contain provisions for managing the business and regulating corporate affairs so long as they are consistent with law and the articles. See RCW 23B.02.060 on corporate bylaws.

Bylaws should answer the questions that create friction

Good bylaws do not read like a law school outline. They answer the questions that come up when the company is tired, under pressure, and trying to close something important.

A workable set of bylaws usually addresses how meetings are called, what notice is required, what counts as quorum, whether directors can participate remotely, when the board may act by unanimous written consent, how vacancies are filled, and which officers have authority to sign. Washington law supplies some default rules, but founders should not rely on defaults if the cap table is changing or investors are joining the board. See RCW 23B.08.200 through 23B.08.240 on meetings, action, and quorum.

Meeting rhythm belongs here too, even if the bylaws stay general and the board calendar carries the detail. For an early-stage tech company, quarterly board meetings are usually the floor. If cash is tight, a product launch is slipping, or enterprise customers create concentration risk, monthly update calls can help management keep directors informed without turning every issue into a formal vote.

Founders also learn quickly that board process and reporting quality are tied together. A board cannot exercise judgment well if the financial package shows up late or changes every month. Management teams that invest early in creating investor-ready financials make board meetings shorter, cleaner, and more useful.

Voting rules should be boring

That is a compliment.

The best voting mechanics leave very little room for argument. Under Washington law, unless the articles or bylaws provide otherwise, a quorum of the board consists of a majority of the number of directors prescribed or fixed. The same chapter also limits how low the quorum can be set. See RCW 23B.08.240 on quorum and voting. In practice, that means the company should decide early whether it wants to stay with the statutory default or customize the rule within the limits the statute allows.

Board terms deserve the same attention. Startups often use annual election cycles because they match shareholder meetings and keep the governance record clean. Longer director terms can add continuity, but they also make it harder to adjust the board after a financing, a founder departure, or a strategic shift. Washington corporations can structure these mechanics in different ways through their articles, bylaws, and election process, but the right answer depends on how much flexibility the company expects to need.

Useful bylaws usually cover a few recurring pressure points:

- Quorum: State how many directors must be present before the board can act.

- Notice: Specify timing and delivery method for regular and special meetings.

- Remote participation: Confirm whether directors may attend by phone or similar communications equipment, consistent with Washington law.

- Written consent: State when unanimous written consent is permitted and how it must be documented.

- Vacancies: Clarify who fills an open seat and whether a specific class of stock has approval rights.

- Committee authority: Distinguish between matters a committee may approve and matters it may only recommend.

Small g governance decides whether the paper works

Founders tend to focus on formal authority. The harder part is board behavior.

A board calendar, pre-read deadline, consent process, and standing agenda can do more for decision quality than another page of boilerplate. If directors receive materials a week late, debate strategy without current numbers, or use meetings to relitigate founder-investor trust issues, the bylaws will not save the process. They will only define the edges of the dispute.

That is why governance documents should be read together. The bylaws may say the board can approve an action, while financing documents, protective provisions, or a shareholders' agreement that allocates approval rights may require a separate stockholder or class vote before the company can close the deal. I often see startups miss this point during bridge financings and secondary sales, where everyone assumes board approval alone is enough.

Cadence turns those rules into habit. Set regular meeting dates. Fix a deadline for board materials. Reserve agenda time for runway, hiring, major contracts, product risk, litigation, and compliance. Boards work better when directors know what will be discussed, when they will see it, and what requires a vote.

From Plan to Reality Implementing Your Board

The first real board problem often shows up when someone outside the company asks for proof. A bank wants the resolution that opened the account. An investor asks who approved the stock issuance. Diligence counsel requests the organizational actions, and the company has a filed certificate, a half-finished cap table, and no clean minute book.

The first moves after incorporation

In Washington, forming the corporation is only the start. The company then needs to complete the organizational steps that turn a state filing into an operating business with traceable authority.

That usually means written incorporator action or an organizational meeting, followed by board action adopting bylaws, appointing officers, authorizing share issuances, approving banking authority, and addressing tax and recordkeeping matters. For a startup, these are not clerical details. They establish who had authority to act, when that authority began, and whether later approvals rest on a valid foundation under the Washington Business Corporation Act, including RCW 23B provisions governing incorporators, directors, officers, and corporate action.

Washington also expects prompt follow-through on state filings after formation. The Secretary of State provides the filing process and reporting requirements through its corporations and charities filing system. If that deadline gets missed, the problem is rarely dramatic on day one. It usually surfaces later, during financing, banking, or a sale process, when someone checks whether the company kept its records current.

A practical implementation checklist

The cleanest approach is to handle implementation in a fixed order:

Confirm the initial board structure

Match the board to the company's current documents and financing posture. A founder-only board may be workable at formation. It may stop working the moment an investor gets a board seat right.Paper the organizational actions correctly

Use written consents or minutes that clearly identify the actor, the action taken, and the effective date. Sloppy resolutions create expensive cleanup work.Issue stock only after authority is clear

Confirm that the board approved the issuance, the form of consideration, and any required securities law and charter points before shares are treated as outstanding.Appoint officers with defined authority

Titles should match actual responsibility. If the company has a president and a CEO, the records should make clear who can sign what.Build the record set now

Keep the certificate, bylaws, resolutions, stock records, and key consents in one place. If the company cannot produce them quickly, it does not really have control of its governance file.Calendar state and internal deadlines

Put reporting dates, annual meeting requirements, option approval timing, and regular board dates on the company calendar while the team is still small.

Working standard: If diligence started tomorrow, the company should be able to produce a coherent record showing who served, what was approved, and whether the approvals matched the governing documents.

Changing the structure as the company grows

Board implementation is not a one-time setup task. It changes when the company closes a priced round, expands the option pool, adds a venture lead, replaces a founder executive, or starts preparing for acquisition diligence.

The legal step is usually straightforward. The coordination is where startups make mistakes. A board expansion may require an amendment to the bylaws, a stockholder vote, or separate approval rights tied to preferred stock documents. In Washington startups, I often see the same failure pattern. Everyone agrees on the business decision, but no one checks whether the charter, investor rights documents, voting agreements, and board approvals all line up.

Good implementation also includes director onboarding. New directors need enough information to exercise judgment without wasting the first two meetings catching up. Give them the charter and bylaws, current cap table, financing documents, recent board materials, budget, insurance summary, major customer concentration, and any active dispute or regulatory issue. That package does more than save time. It reduces the risk that a director votes on a partial record or asks management to revisit decisions that were already made correctly.

A board is durable when the paperwork, approvals, and habits match. That is the practical test.

Best Practices and Common Pitfalls

Most board advice stops at what might be called Big G governance. Bylaws, votes, committees, charters. Those mechanics matter, but they don't explain why one board helps a company think clearly while another board with similar documents becomes a source of friction.

The missing piece is small g governance. That includes information flow between meetings, the quality of the chair-CEO relationship, how dissent gets handled, whether directors know when to stay in oversight mode, and whether management gets surprised by board concerns at the meeting itself. In nonprofit governance research, 71% of nonprofit boards struggled to find practical material on these operational dynamics, according to Egon Zehnder's discussion of small g governance. The same gap shows up in startup companies.

What high-functioning boards actually do

Strong boards usually share a few habits:

- They separate oversight from management: Directors ask hard questions without trying to run weekly operations.

- They create disciplined information flow: Pre-reads arrive on time, key issues are flagged early, and surprises are rare.

- They recruit for usefulness, not loyalty: The company adds directors who fill capability gaps, not friends who will keep meetings pleasant.

- They normalize dissent: Good boards make it safe to disagree before the vote, not after the damage.

One emerging area where this matters is investor participation. The Angel Capital Association reported that in 2022, only 20% of angel deals included a board director from the reporting angel group, while 17% had passive board observers, in its discussion of angel involvement and board seats. The practical lesson isn't that every investor should get a seat. It's that founders should think deliberately about whether the company wants passive capital, active governance, or a mix of both.

Common mistakes that weaken boards

The most common failures are predictable.

First, the board gets filled with people who are comfortable, available, or politically hard to exclude. That creates an echo chamber.

Second, management sends too much data and too little judgment. A 70-page deck can hide more than it reveals.

Third, meetings become status updates. Directors read slides aloud, debate details that belong to managers, and rush the few issues requiring board-level decisions.

Fourth, nobody manages communication outside formal meetings. Then pressure builds privately, and the actual meeting turns into a performance rather than a working session.

Good governance isn't measured by how polished the board book looks. It's measured by whether the right people can confront the right problem at the right time.

The human side founders often underestimate

Board effectiveness also depends on how people present and communicate. That isn't cosmetic. A founder who can't explain a financing problem, hiring miss, or product delay clearly may lose confidence even when the underlying business is salvageable. For leaders preparing for difficult presentations, a targeted communication resource like finding a pronunciation coach for executives preparing for board meetings can help sharpen delivery in high-stakes settings.

The practical standard is simple. A healthy board should make the company more durable, not more theatrical. If directors are surprised often, if minutes are thin, if roles are fuzzy, or if governance only appears when fundraising starts, the board structure needs work.

For Washington founders, the best board of directors structure is rarely the most elaborate one. It is the structure that fits the company's stage, satisfies the law, gives investors confidence, protects decision quality, and still lets management build.

Founders, investors, and executives building or revising a board need documents and governance mechanics that fit the company they have, not a generic template. By Design Law Firm & Legal Consultancy, PLLC advises Washington businesses on corporate formation, board governance, shareholder arrangements, technology risk, and the legal infrastructure that supports durable growth.