Two founders launch a company on trust. They split the equity evenly, move fast, and put the hard conversations off for later. Months later, one wants to raise outside capital on aggressive terms. The other wants to stay lean. Then a strategic buyer appears, a key employee expects equity, or one founder needs to step back for personal reasons.

That's when a handshake stops being a strength and starts becoming a liability.

A shareholders' agreement exists for that exact moment. Founders often ask what is a shareholders agreement when things are still friendly and momentum is high. The better question is what happens when the company faces its first serious disagreement and nobody wrote down the rules. In a startup, legal ambiguity rarely stays contained. It spills into cap table disputes, board conflict, financing delays, and damaged relationships.

The Unspoken Risks of a Handshake Deal

A common startup pattern looks harmless at the beginning. Two people build a product, divide shares, and rely on mutual confidence instead of formal governance. That works until the business has to make a decision that affects control, money, or timing.

One founder may believe a sale should require unanimous approval. The other may assume a majority can force the transaction through. One may think a departing founder keeps all vested stock without restrictions. The other may expect a buyback at a discounted value. If nobody wrote the answers down, each side usually believes the law will naturally support its position. It often doesn't.

That's why founder disputes become so expensive. The argument usually isn't just about economics. It's about different expectations that were never translated into enforceable terms.

The most dangerous governance gap isn't hostility. It's misplaced confidence that everyone means the same thing.

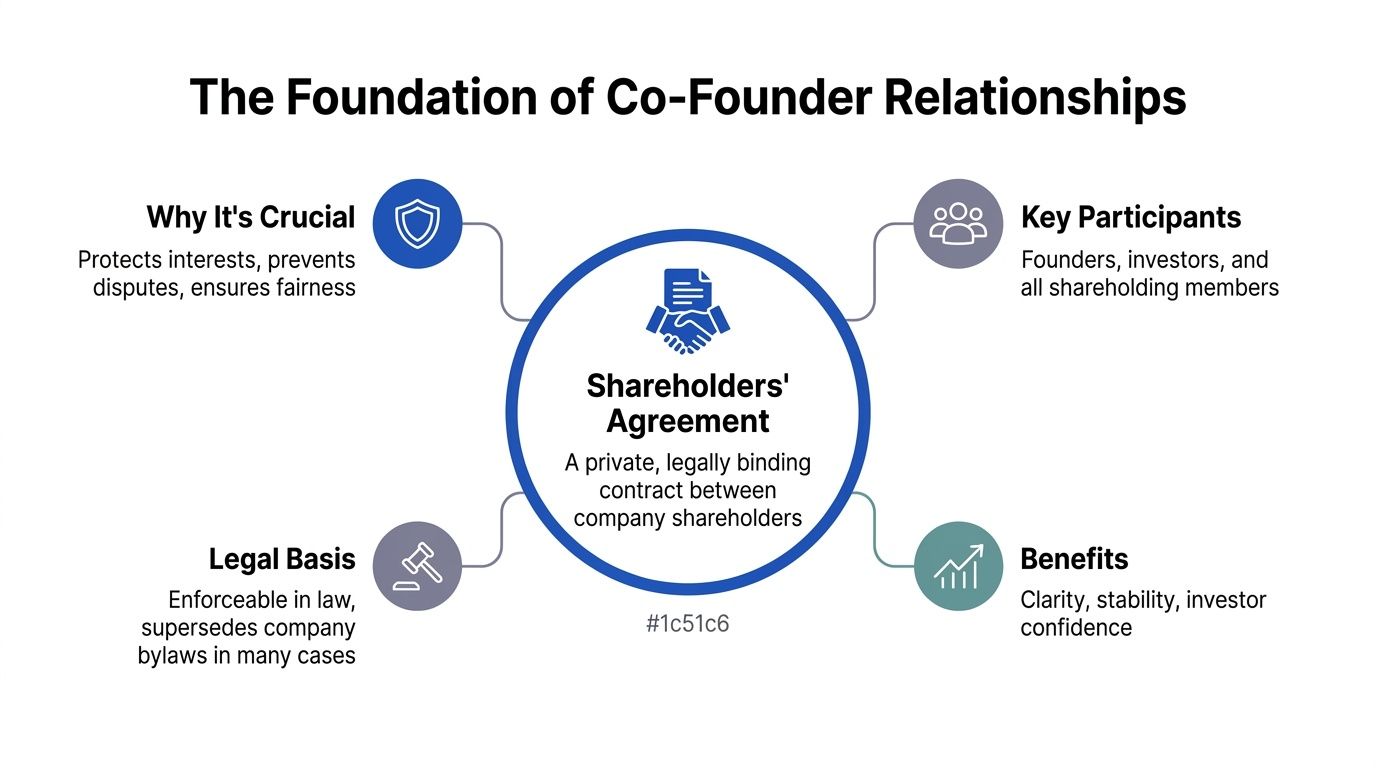

A solid shareholders' agreement acts as the company's internal rulebook. It tells the shareholders what happens if someone wants to sell, leaves the company, stops performing, dies, becomes disabled, or blocks an important decision. It also gives the corporation a framework for handling disputes before they harden into litigation.

Dispute process matters just as much as substantive rights. Founders that want a practical overview of how escalation paths should work can review these dispute resolution clause considerations alongside their governance documents.

Without a written agreement, even experienced founders often default to informal bargaining. That's rarely efficient. It drains time, distracts management, and makes investors nervous. A company can survive bad product assumptions more easily than a broken founder relationship with no legal structure around it.

The Foundation of Co-Founder Relationships

A shareholders' agreement is a private contract among the shareholders of a corporation. It sets the rules for ownership, control, decision-making, transfers, and exits. In practical terms, it functions like a business pre-nup. It doesn't assume failure. It assumes change.

A concise definition appears in DiliTrust's overview of shareholder agreements: a shareholders' agreement is a legally binding internal contract that defines ownership structure, voting rights, and decision-making protocols. It must include a pre-defined share valuation methodology to prevent significant legal problems during disputes or exit events.

What the agreement actually does

This document governs the internal relationship between the people who own the company. It answers operational questions that are too specific, too sensitive, or too commercial to leave to default statutory rules alone.

Typical areas include:

- Ownership structure: who owns what, and whether different holders have different rights

- Voting mechanics: which decisions need a simple majority, supermajority, or unanimous approval

- Board influence: who appoints directors, how directors are removed, and what founder consent rights survive financing rounds

- Share transfers: whether a founder can sell stock freely or must first offer it internally

- Exit economics: how minority holders participate in a company sale and how valuation works if someone exits early

A founder who's already using confidentiality agreements should think of this as a separate layer of internal governance. An NDA protects information. A shareholders' agreement allocates power, responsibility, and economic outcomes. For that distinction, this overview of NDA agreements helps clarify what each document is designed to do.

Why sophisticated founders treat it as core infrastructure

A well-drafted agreement creates certainty before stress hits. It also protects relationships by replacing emotional negotiation with predetermined rules. That matters because startup disputes often arise when everyone is under pressure at the same time. A financing is live. Payroll is due. One founder is overloaded. Another is questioning strategy.

Practical rule: If the business would struggle to answer “what happens if one shareholder says no,” the governance structure isn't finished.

This is also where many founders misunderstand the document's legal weight. A shareholders' agreement isn't just a side letter or a ceremonial founder memo. When drafted properly, it becomes one of the company's central governance instruments.

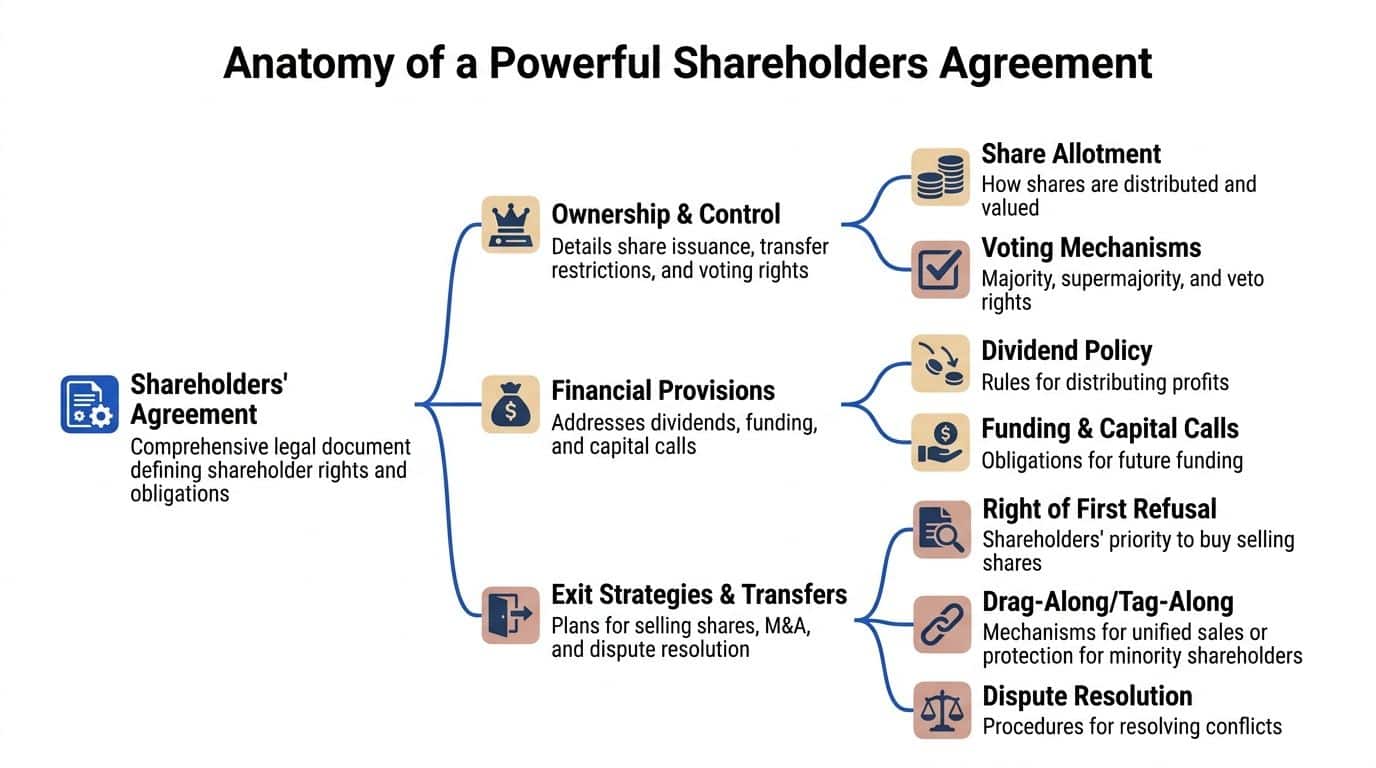

Anatomy of a Powerful Shareholders Agreement

A useful agreement doesn't try to sound complex. It solves predictable problems with specific clauses. Founders should read each provision by asking one question: what real business mess does this clause prevent?

A visual breakdown helps show how these moving parts fit together.

Ownership and control

The first job of the agreement is to define who controls what. That means more than listing percentages.

Some rights follow economic ownership. Others should be negotiated separately. A founder with a minority stake may still need the right to appoint a director. An investor with protective provisions may have veto power over issuing new shares, taking on debt, or approving a sale. If those rights aren't clear, conflicts move quickly from the boardroom to counsel.

This section often addresses:

- Voting thresholds: which matters require ordinary approval and which require enhanced consent

- Board appointments: whether founders, lead investors, or specific share classes nominate directors

- Reserved matters: decisions that can't proceed without specific shareholder approval, such as major acquisitions or large capital outlays

Founders often focus on percentage ownership and ignore procedural control. That's a mistake. Control usually turns on meeting mechanics, director appointment rights, and consent thresholds, not just headline equity.

A broader governance perspective can help here. AuditReady's IT governance insights are useful because they frame shareholder interests within the larger governance environment a growing company has to manage.

The section below offers a practical explainer before the transfer and exit terms come into play.

Transfer restrictions and exit rights

Shareholders rarely stay aligned forever. The agreement needs a controlled process for ownership changes.

A strong transfer section usually includes pre-emption or right of first refusal concepts so existing holders can buy shares before they go to an outsider. It should also address tag-along and drag-along rights. Tag-along rights protect minority holders by allowing them to join a sale on the same terms. Drag-along rights let a qualifying majority require minority holders to participate in a company sale when a legitimate exit is on the table.

These clauses are where legal drafting meets business power. If the drag threshold is too low, minority holders can be steamrolled. If it's too high, a serious acquirer may walk away because the cap table is impossible to close.

Deadlock and disputes

The most neglected provisions are often the ones that matter most when the company is under strain. Equal ownership structures are especially vulnerable. According to Taylor Rose's discussion of shareholder agreement deadlock planning, to manage 50:50 ownership deadlocks, an agreement must include explicit cross-option agreements and staged exit mechanisms, often incorporating key person insurance provisions and compulsory mediation or arbitration clauses to handle valuation and resolution when a shareholder dies or departs.

That matters because 50:50 sounds fair until there's a deadlock over hiring, fundraising, or selling the business.

Useful deadlock tools include:

- Cross-option agreements: one side can buy, or be required to sell, under predefined circumstances

- Staged resolution: negotiation first, then mediation, then arbitration or a forced separation mechanism

- Key person planning: insurance or liquidity planning if a founder dies or becomes incapacitated

A deadlock clause shouldn't just identify the problem. It should move the company to a decision.

Contingencies that founders avoid discussing

Every agreement should confront uncomfortable scenarios directly. Death, disability, divorce, termination for cause, and voluntary resignation all affect ownership and control. A founder's departure shouldn't leave the company guessing whether shares vest, can be repurchased, or remain fully transferable.

This is also where valuation language earns its keep. If the agreement says the company can repurchase shares but never explains the pricing method, the dispute moves to another battlefield.

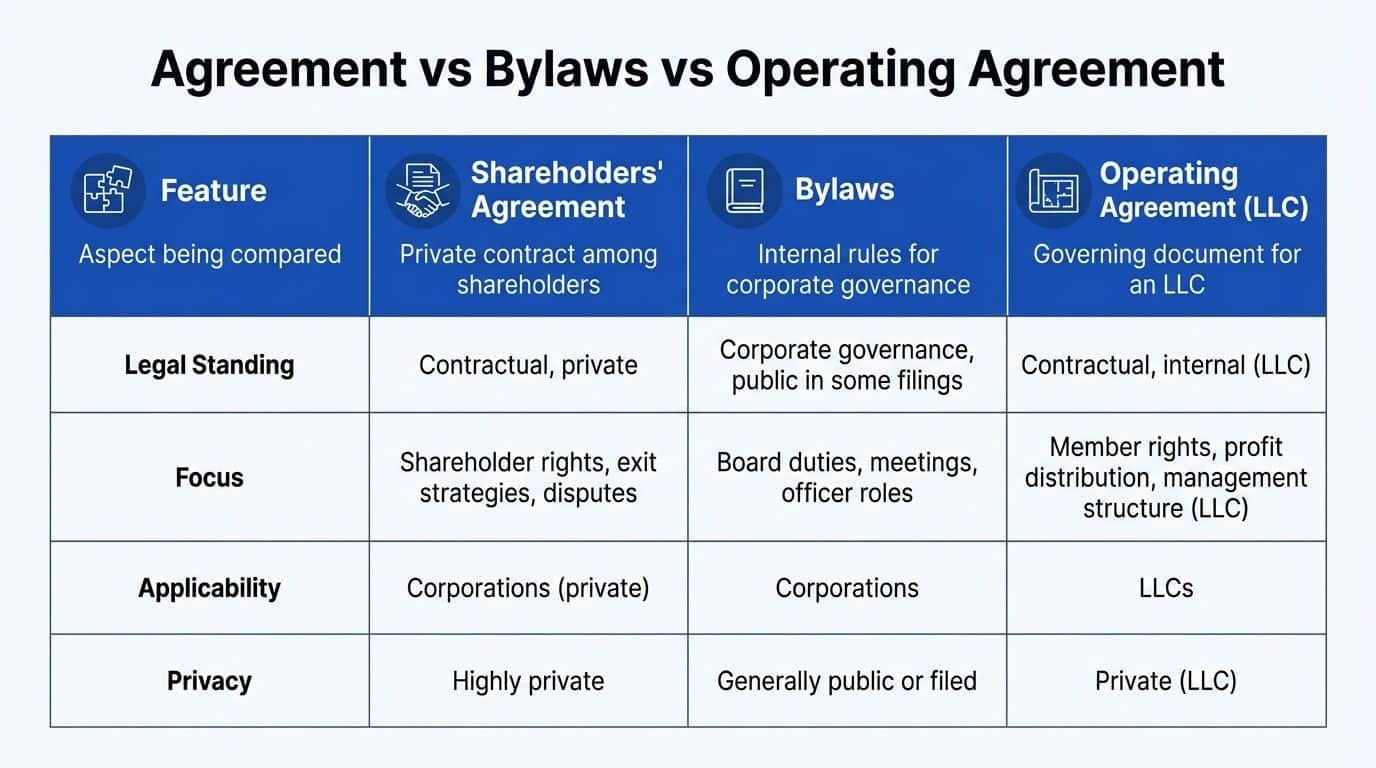

Agreement vs Bylaws vs Operating Agreement

Founders regularly use these documents interchangeably. That creates confusion at exactly the wrong time, especially during diligence or a dispute. A shareholders' agreement, bylaws, and an LLC operating agreement may overlap in subject matter, but they don't serve the same function.

The following comparison captures the distinction at a glance.

Key differences that matter in practice

| Document | Main role | Who it binds | Typical subject matter |

|---|---|---|---|

| Shareholders' agreement | Private contract among owners | Signatory shareholders and, indirectly, the corporation when structured properly | Transfer rights, voting arrangements, exits, dispute process |

| Corporate bylaws | Internal governance rules for the corporation | The corporation, directors, officers, and governance process | Meetings, officer duties, board procedures |

| Operating agreement | Core governance contract for an LLC | LLC members and managers | Profit allocation, management rights, membership issues |

A corporation usually has bylaws whether the founders think about them or not. A shareholders' agreement is different. It's negotiated and crafted for the specific company. It often addresses issues bylaws either don't cover or shouldn't cover in detail.

For LLC founders in Washington, the parallel document is the operating agreement, not a shareholders' agreement. That distinction becomes critical when teams use online templates without matching the document to the entity type. This explanation of why every Washington LLC needs an operating agreement is a useful reference for that separate structure.

What happens when documents conflict

Conflict between private agreements and formal governance documents is one of the most underestimated legal risks in founder planning. According to Antler's startup shareholders' agreement analysis, recent court rulings show 42% of shareholder disputes stem from such conflicts, especially when contract terms like drag-along rights clash with state-mandated share laws.

When documents pull in different directions, the company doesn't get flexibility. It gets uncertainty.

That uncertainty surfaces during financings, exits, and internal disputes. The practical fix is simple in concept and harder in execution. Draft all governance documents as a coordinated package, not as isolated paperwork created at different times by different people.

When Washington Startups Absolutely Need an Agreement

The right time to put a shareholders' agreement in place is earlier than most founders think. Waiting until a conflict appears usually means the parties have already lost the benefit of neutral, rational drafting.

Four moments that should trigger action

Washington startups should treat these business milestones as drafting or review triggers:

- At incorporation or immediately after formation: this is when founder expectations are easiest to align

- Before issuing founder or advisor equity: equity grants without transfer and vesting discipline create future cleanup work

- Before the first meaningful hire with stock or options: employee equity changes the governance picture

- Before outside money arrives: investors will examine voting rights, transfer mechanics, and consent thresholds closely

For startups in Seattle and the broader Puget Sound region, this is even more important in fast-moving technology businesses. Cap tables change quickly. New investor rights get layered in. Data use, AI governance, and privacy obligations can alter how boards evaluate risk and control.

Why a static agreement fails high-growth companies

A common founder mistake is treating the agreement as a one-time formation document. That approach breaks down in venture-backed or rapidly scaling companies. According to KMCO's discussion of common shareholder agreement problems, 68% of agreements become obsolete within 3 years due to rapid equity changes and new investors, and agreements need dynamic amendment triggers tied to funding milestones to remain effective.

That statistic matters because it captures a real operational problem. A document drafted for two founders can become misaligned after a SAFE round, an expanded option pool, a seed financing, or the arrival of preferred stock holders with board rights.

A better approach is to build amendment triggers into the agreement itself.

What a living document looks like

A dynamic agreement typically includes review points tied to actual company events, such as:

- Financing milestones: a priced round, major note conversion, or new investor class

- Equity plan changes: expansion of the employee stock option pool or material refresh grants

- Leadership transitions: a founder leaving an executive role while remaining a shareholder

- Regulatory shifts: changes that affect AI products, data privacy obligations, or board-level compliance oversight

Washington tech companies don't need more paperwork. They need governance that evolves at the same pace as the business. That's what separates a document that merely exists from one that protects the company.

Practical Drafting and Risk Mitigation Tips

Most shareholder disputes can be traced back to vagueness, not malice. Founders usually know the broad outcome they want. Problems arise when the document uses soft language where precision is required.

According to Hch Lawyers' guidance on drafting enforceable shareholder agreements, for an agreement to be enforceable in many US jurisdictions, it must be a written document signed by all shareholders and made known to the corporation. It must also specify which jurisdiction's laws apply to prevent conflicts during litigation.

Drafting points worth getting right the first time

A practical drafting checklist should include the following:

- Fix the valuation method early: don't leave buyout pricing to a future argument. Choose a method and define when it applies.

- Define departure categories carefully: resignation, termination for cause, disability, and retirement should not produce the same economic result.

- Make dispute resolution realistic: mediation or arbitration only works if the process is affordable, clear, and matched to the likely dispute.

- Coordinate with the cap table: the legal document should match actual ownership, vesting, and dilution assumptions. Founders who haven't cleaned this up should review capitalization table management fundamentals before finalizing governance terms.

What tends to go wrong

Some clauses fail because they're too thin. Others fail because they try to over-control future business decisions.

A few recurring errors stand out:

- Overly rigid investor restrictions can make the company difficult to finance.

- Undefined “cause” language creates litigation risk when a founder exits under pressure.

- Boilerplate transfer provisions often ignore how startups raise money and issue equity in practice.

Founders' shortcut: If a clause would require everyone to “figure it out later,” it probably isn't finished.

The best drafting process forces the founding team to answer hard questions while they still trust each other. That's not pessimistic. It's efficient.

Your Next Steps for a Secure Foundation

A shareholders' agreement is one of the few startup documents that protects both the business and the relationship between the people building it. It creates clarity around ownership, control, exits, dispute process, and the uncomfortable contingencies founders would rather postpone. Those issues don't stay theoretical for long.

For Washington startups, the bigger lesson is that this can't be a static template pulled from the internet and forgotten in a data room. Growth changes the cap table. New investors change governance. Regulation changes board priorities. The agreement should evolve with the company.

Founders asking what is a shareholders agreement usually think they're asking for a definition. They're really asking how to prevent future misalignment from becoming a legal crisis. The answer is a specific, coordinated, regularly updated agreement that reflects how the company operates in practice.

Generic forms are rarely built for venture financing, founder departures, investor rights, or the governance demands facing technology companies. Cleaning up a bad agreement after a dispute starts usually costs more, takes longer, and limits options.

Early legal work in this area isn't administrative overhead. It's part of the company's operating system.

Founders who want a durable governance foundation can work with By Design Law Firm & Legal Consultancy, PLLC, a Seattle-based business and technology law firm serving startups and growth-stage companies across Washington State. The firm helps clients draft, review, and update shareholders' agreements that fit real-world financing plans, cap table changes, board dynamics, and evolving regulatory risks.