Two founders form a Washington LLC on a Friday afternoon, split ownership with a handshake, and pull a template off the internet that night. Six months later, one wants to put in more money, the other doesn't. A third advisor expects equity that was “discussed.” Nobody can agree on whether profits should be distributed, reinvested, or reserved for taxes. The problem isn't the business idea. The problem is that the founders never wrote down the rules.

That's usually the moment founders start searching for how to write an operating agreement. By then, the document isn't a planning tool anymore. It's damage control.

A strong operating agreement does something far more useful than satisfy a startup checklist. It forces early decisions about control, economics, founder exits, and future funding, then turns those decisions into enforceable contract language. For a Washington startup, that matters even more because state law gives LLCs flexibility. Flexibility is valuable only if someone uses it well.

Why Your WA Startup Needs an Operating Agreement

A Washington startup can form fast and still be badly exposed. The filing goes through, the company exists, and everyone gets back to product, customers, and hiring. Then a real decision shows up. One founder wants to raise outside money on aggressive terms. Another wants to stay lean and avoid dilution. Without an operating agreement, that fight starts with guesswork.

Washington law gives LLCs a lot of contractual freedom. It also gives founders a false sense that they can fill in the details later. An LLC operating agreement is not required by law in Washington under RCW 25.15.018, and the state does not require filing it with the Secretary of State. Once the members sign it, though, it becomes a binding internal contract, as explained in this Washington operating agreement overview.

For a startup, that contract is not paperwork. It is the rulebook for money, control, and exits.

If the members never write those rules down, Washington's default LLC provisions step in. Those defaults may work for a small family business with stable ownership. They are usually a poor fit for a startup that expects uneven founder contributions, changing compensation, SAFE or preferred financing, profit reinvestment, vesting, advisor equity, or a sale process on a compressed timeline.

A useful operating agreement answers practical questions before they become expensive disputes:

- Who owns each percentage interest, and whether any of that equity vests over time

- What each founder contributed, and what happens if one person does not deliver promised cash, work, or IP

- Which decisions managers can make alone, and which decisions require member approval

- Whether the company can force additional capital contributions or accept dilution instead

- How tax distributions, retained earnings, and other cash distributions are handled

- What happens if a founder quits, is terminated, dies, files bankruptcy, or wants to transfer units

- How the company approves new investors, amends terms, or prepares for an acquisition

Those are growth questions, not just legal questions.

Founders who want a plain-language primer on what an LLC operating agreement does will find that resource useful before comparing it against Washington-specific concerns. For a more local view, this discussion of why every Washington LLC needs an operating agreement explains why state-level flexibility cuts both ways.

Single-member LLCs need this document too. In practice, banks, investors, buyers, and counterparties often ask for it during diligence. A written agreement also helps show that the company is being treated as a separate legal entity, which matters if liability protection is ever challenged.

I tell founders the same thing in Seattle, Bellevue, and Tacoma. The operating agreement is where the business model meets the cap table. If it is silent on funding, control shifts, transfers, and founder departures, the company will end up negotiating those issues under pressure, usually when the circumstances are more critical and the relationships are worse.

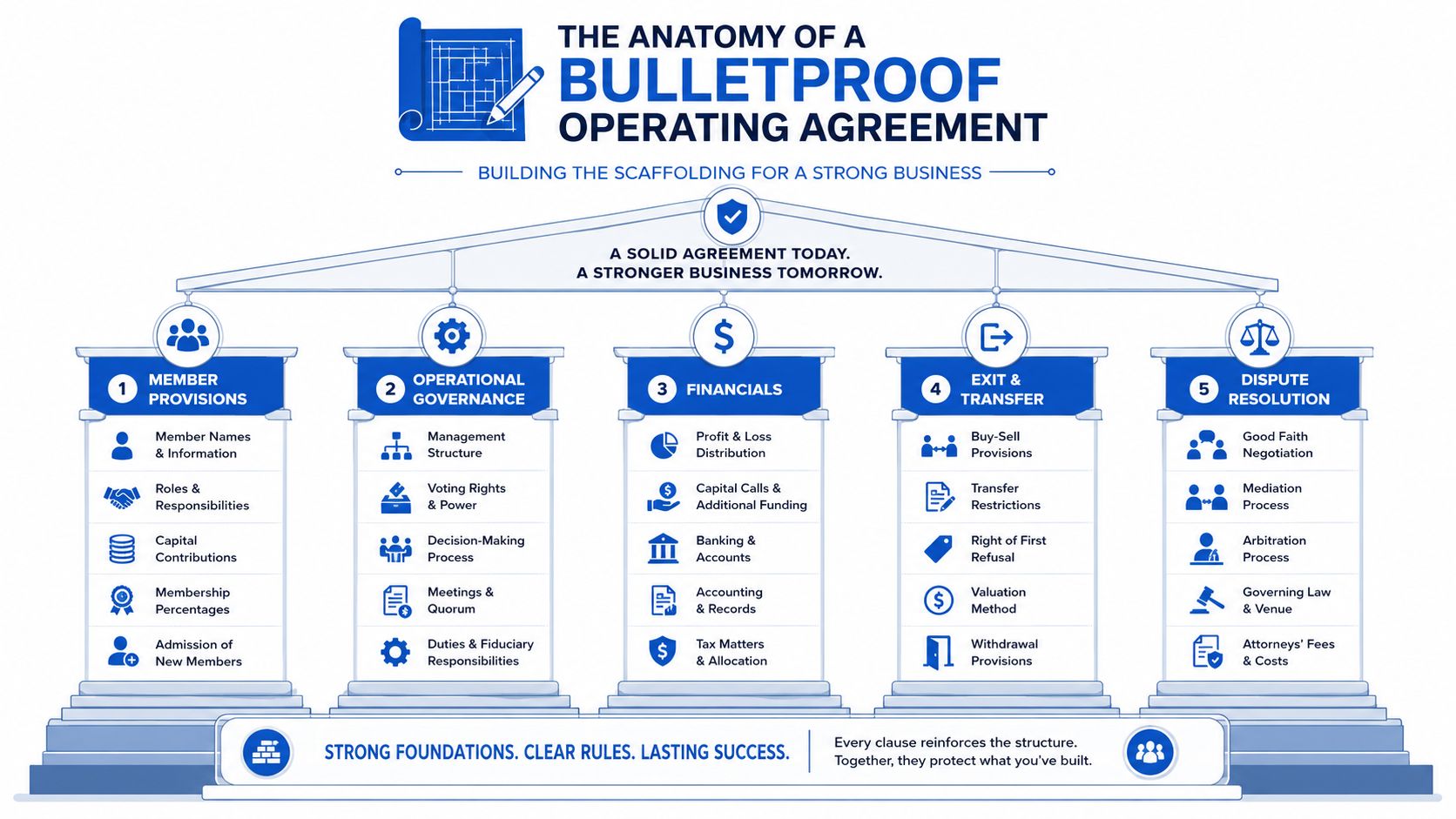

The Anatomy of a Bulletproof Operating Agreement

A founder leaves six months before a seed round. Another says the company owes them more equity because they worked full-time without salary. The lead investor asks who can approve new units, who signs financing documents, and what happens if the board structure changes after closing. If the operating agreement is thin, those questions become emergency negotiations.

A strong operating agreement gives clear answers before money or relationships are under strain. For a Washington startup, that usually means drafting for the company you expect to become, not just the company that exists on filing day.

Start with the company's legal and economic baseline

The first pages should do more than restate what was filed with the Secretary of State. They should lock down the facts that everyone will rely on later in diligence, tax reporting, banking, and equity discussions.

At minimum, state:

| Topic | What to spell out |

|---|---|

| Company details | Legal name, Washington formation, principal office, business purpose |

| Members | Full legal names and status as members |

| Ownership | Each member's percentage or unit interest |

| Effective date | When the agreement starts governing |

If the LLC has issued units instead of simple percentage interests, say so clearly and tie those units to an attached cap table or schedule. Startups often outgrow vague ownership language faster than founders expect.

Draft the capital section for real funding pressure

The capital contribution clause should answer three practical questions. What did each member contribute. How is that contribution valued. Can the company require more money later.

I see problems here all the time. A founder says sweat equity counted as a capital contribution, another founder disputes the value, and the agreement never defined whether future cash calls were optional, mandatory, or dilutive.

Use plain language and set the rule:

Sample language

“Each Member's initial capital contribution is listed on Exhibit A. No Member is required to make any additional capital contribution unless this Agreement expressly states otherwise or the Members approve a capital call under the voting standard set forth in Section [X].”

If someone contributes IP, equipment, customer contracts, or other non-cash assets, identify the asset and its agreed value in an exhibit that is attached and adopted with the agreement. If you skip that step, you create room for later fights over whether the asset was ever transferred, what it was worth, and whether ownership was issued validly in return.

Treat distributions and allocations as separate decisions

Founders often collapse three different concepts into one. Ownership. Tax allocations. Cash distributions. They are related, but they are not interchangeable.

The agreement should spell out:

- How profits and losses are allocated

- Whether the company can retain cash for operating reserves

- Whether tax distributions will be made, and on what formula

- How new money or changing ownership affects mid-year allocations and distributions

That drafting work matters for founder compensation as much as investor economics. Teams comparing salary, bonus, and equity models sometimes use outside reading on business profit sharing strategies to sort through the business choices before they reduce them to legal terms.

Separate daily authority from company-changing decisions

A startup cannot function if every vendor contract, hire, or product decision needs unanimous approval. It can also blow up if one person can sell assets, admit a new investor, or rewrite economics without a meaningful vote.

The fix is a decision structure with tiers.

Ordinary course matters can sit with managers or a simple majority. Big items should require a higher threshold. A short list of company-changing actions should require supermajority or unanimous approval, depending on the risk and the makeup of the cap table.

For many Washington startups, that protected list includes:

- Admitting new members

- Issuing additional equity or convertible interests

- Borrowing above a stated threshold

- Approving mergers, asset sales, or dissolution

- Amending the operating agreement

- Entering related-party transactions

Generic templates are often insufficient. A two-founder services business and a venture-backed startup should not use the same approval mechanics. If you expect SAFEs, priced rounds, option-style incentives, or a sale process, the voting section needs to reflect those paths from the start.

Define what happens when authority is contested

Many LLC disputes start with a simple question. Who had authority to do that.

The agreement should say who can bind the company, when written consent is required, what records must be kept for approvals, and what happens if members deadlock on a major decision. Clear process language reduces the odds that a governance fight turns into a lawsuit. Founders working through those clauses should review dispute resolution provisions for LLC operating agreements alongside the voting section, because procedure often decides whether a disagreement stays manageable.

One sentence can save a lot of money later: define the decision, define the vote required, and define who signs.

Tailoring Your Agreement for Washington State Law

A generic national template can cover ownership percentages and meeting notices. It usually misses the parts that matter most under Washington law.

Washington gives LLCs room to modify fiduciary duties

One of the most important Washington-specific features is this. RCW § 25.15.038(6)-(7) allows an LLC to modify the statutory duty of loyalty and duty of care in the operating agreement, so long as the change isn't unreasonably broad, as discussed in this Washington operating agreement guide.

That flexibility is powerful. It also carries risk.

A startup with multiple founders may want to narrow conflict restrictions so members can invest in other ventures, serve on advisory boards, or pursue adjacent projects without automatically breaching fiduciary obligations. A passive investor may want narrower duties than an operating founder. A manager may want indemnification and clear safe-harbor language for business judgments made in good faith.

Modify carefully, not casually

Founders shouldn't read that statute as permission to erase responsibility. A clause that tries to eliminate accountability in broad, casual language can create more problems than it solves.

A workable drafting approach usually asks:

- Who owes duties. Members, managers, or both.

- Which activities are permitted. Outside investments, related businesses, board service.

- What approval process applies. Disclosure, consent, recusal, or written waiver.

- What conduct remains prohibited. Fraud, intentional misconduct, bad-faith self-dealing.

Practical rule

The more flexibility the company wants around founder side projects or investor involvement, the more specific the fiduciary-duty language needs to be.

Local legal judgment holds greater importance than a template. Broader formation issues often overlap with entity selection, tax elections, and governance choices, especially for founders who first considered out-of-state setups. This discussion of LLC formation pitfalls and out-of-state setup risks highlights why Washington-specific drafting shouldn't be an afterthought.

Community property deserves a direct conversation

Washington is a community property state. For married founders, that can affect how ownership interests are characterized and what happens if a member later divorces, dies, or transfers interests. A national template often says little or nothing about spousal claims, required consents, or transfer restrictions tied to marital property issues.

That doesn't mean every spouse becomes a member. It does mean the operating agreement should address transfer mechanics and, when appropriate, coordinate with separate marital or estate planning documents. Founders usually regret ignoring this issue only when a triggering event forces everyone to deal with it under pressure.

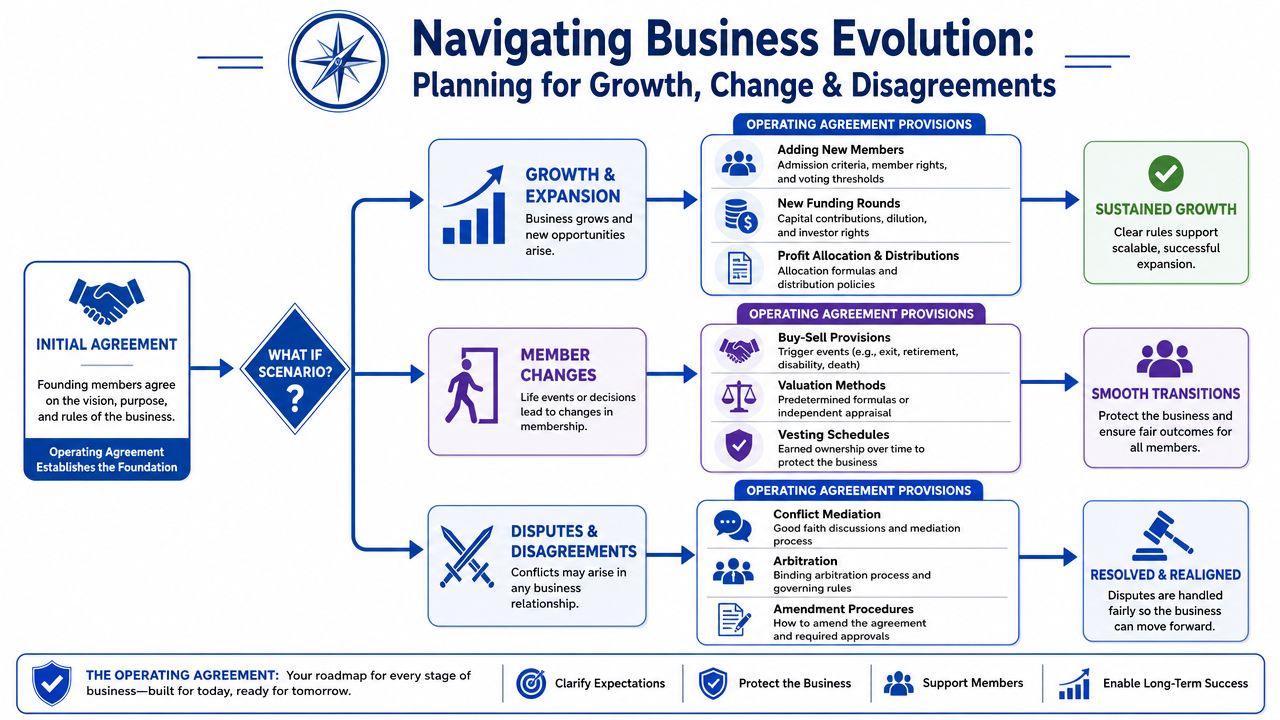

Planning for Growth Change and Disagreements

A Washington startup can look stable on paper and still break under ordinary growth. The usual pattern is familiar. Two founders form an LLC, split ownership, use a template, and move on. Twelve months later, one founder has put in more cash, the company is talking to investors, a SAFE is outstanding, and nobody agrees on whether the next contribution is a loan, a capital call, or dilution.

Funding clauses need to handle real startup pressure

This part of the agreement has to do more than record who contributed what at formation. It should set rules for what happens when the company needs more money, on short notice, and the members have different appetites for risk.

For startups, that usually means answering questions a template skips. Can managers issue new units without unanimous approval? Is a future capital call mandatory, optional, or board-approved only? If one member funds a shortfall and another does not, does the contributing member get dilution protection, preferred repayment, or a convertible instrument instead of additional equity?

Those choices have long-term consequences. A mandatory capital call can keep the company alive, but it can also force out a founder who cannot keep funding the business. Voluntary contributions avoid that pressure, but they often create resentment unless the agreement spells out the economic return for the member putting in more cash.

A workable clause usually addresses at least these points:

| Question | Why it matters |

|---|---|

| Is a future capital call mandatory or optional? | Members need to know whether they can be required to fund a cash shortfall |

| What happens if a member declines to contribute? | The company needs a defined remedy, such as dilution, a member loan, or a purchase right |

| How are distributions handled after new money comes in? | Members need a clear rule for whether new capital changes payout priorities |

The legal document also needs to match the company's actual ownership records. Once an LLC starts tracking SAFEs, notes, profits interests, or changing membership percentages, sloppiness in the paperwork becomes expensive. Founders dealing with that complexity should keep the agreement aligned with their capitalization table management process.

Buy-sell provisions are where friendships survive or fail

A serious operating agreement plans for departures before anyone wants to leave. That includes resignation, disability, death, bankruptcy, misconduct, and a founder who stops contributing but refuses to sell.

The buy-sell terms should answer four practical questions. What event triggers a buyout? Who has the first right to buy, the company, the remaining members, or both? How is the price set? How long does the buyer have to pay?

Valuation is usually the pressure point. A fixed formula is cheap to administer, but it gets stale fast in a startup with uneven revenue and changing investor interest. An appraisal process is more defensible, but it adds cost and delay. Installment payments help the company preserve cash, but the departing member will want security and clear default consequences.

Washington founders should be especially careful here because many LLCs operate with a small member group and heavy founder dependence. If one member leaves suddenly, the business may not have the cash to fund a lump-sum redemption. The agreement should reflect that reality instead of promising a buyout the company cannot perform.

A short video can help frame how these issues surface in practice.

Dispute resolution should slow conflict before it explodes

Dispute clauses work best when they are procedural, not aspirational. “The parties will try to work it out” does not help much once trust is gone. A better approach is a staged process with deadlines and defined decision points.

The agreement can require senior-level negotiation for a set period, then mediation, then arbitration for specified claims. It should also preserve access to court for narrow issues that need immediate action, such as injunctive relief, misuse of company IP, or an attempt to transfer units in violation of the agreement. The American Arbitration Association discusses tiered dispute resolution provisions and drafting considerations in its guidance on multi-step dispute resolution clauses.

That structure is not just about saving fees. It buys time. In closely held startups, the primary objective is often to keep the company operating while the principals fight about money, control, or exit terms. A well-drafted process reduces the chance that a business disagreement turns into a court filing that scares employees, customers, and investors.

Washington-specific drafting also matters here. If the company wants arbitration, the clause should be clear about scope, forum, and provisional court remedies. If it wants mediation first, the agreement should say who selects the mediator and how costs are shared. Otherwise, the dispute process itself becomes the first dispute.

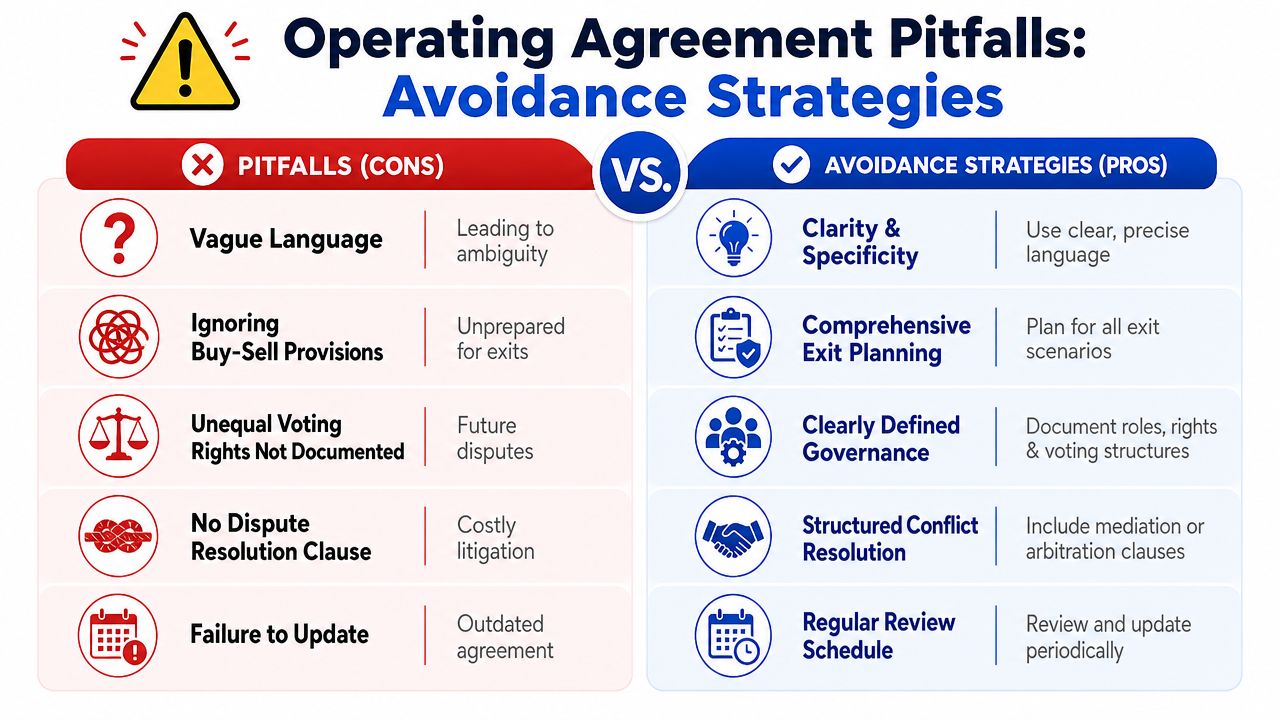

Common Drafting Pitfalls and How to Sidestep Them

Founders often assume a decent template plus goodwill is enough. It usually isn't. Operating agreements fail less from exotic legal issues than from ordinary vagueness.

The internet template problem

Templates are useful starting points. They're dangerous ending points.

Thomson Reuters notes that operating agreements drafted without professional legal review frequently lack buy-sell rules and dissolution terms, both of which are essential when a member dies or goes bankrupt, in this article on operating agreement pitfalls and legal review. Those are exactly the events when the document gets tested hardest.

Vague voting language creates deadlock

One of the most common drafting mistakes is treating voting as a single concept instead of a series of specific mechanisms. A workable agreement has to define who votes, whether votes are per capita or weighted, what quorum applies, and which threshold governs each major action.

This analysis of voting thresholds in operating agreements explains why failing to distinguish between majority, supermajority, and unanimous consent is a primary cause of intra-member deadlock.

Here's where founders usually go wrong:

- “Major decisions require approval.” Approval by whom, and at what threshold?

- “Members vote based on ownership.” On all issues, or only some?

- “Unanimous consent for important matters.” Which matters count as important?

Other mistakes that keep showing up

Some errors look minor on paper and become expensive later.

- Non-cash contributions without valuation. If one founder contributes software code, equipment, or services, the agreement should state the agreed value and resulting ownership consequences.

- No dissolution roadmap. When the company winds down, someone has to know who votes, who liquidates assets, and how remaining property gets distributed.

- Failure to update the document. An agreement written for two founders often no longer fits after an investor comes in, a member becomes passive, or the company changes its revenue model.

The phrase “we'll figure that out later” usually means “we'll argue about that later.”

Finalizing Executing and Maintaining Your Agreement

A founder closes a seed round, sends the investor the company records, and realizes the signed operating agreement does not match the cap table, the managers listed in practice, or the transfer limits everyone thought were in place. That is not a drafting problem anymore. It is a diligence problem, a credibility problem, and sometimes a consent problem that can delay the financing.

Make it binding the right way

Execution is the point where legal terms become company records. In Washington, the operating agreement does not get filed with the Secretary of State, so the signed copy in your records is often the best evidence of what the members agreed to. If signatures are missing, exhibits are incomplete, or different people are working from different drafts, the company has created uncertainty that will surface at the worst time: a dispute, an audit, bank onboarding, or investor diligence.

Use a closing process that is boring and exact.

- Confirm the final draft matches the actual terms, including ownership percentages, capital contributions, manager authority, and any side terms that were folded into emails or term sheets.

- Attach every exhibit and schedule. Missing contribution schedules and member lists create avoidable arguments later.

- Collect signatures from each required party under the agreement's execution and amendment rules.

- Date the agreement consistently and keep a clean PDF of the fully signed version.

- Store it with the LLC's core records, alongside the certificate of formation, written consents, tax elections, and later amendments.

- Distribute the same final copy to founders, managers, and anyone responsible for corporate records.

Notarization is usually a practical choice, not a statutory requirement. I often recommend it when founders are signing in different places, when one member may later challenge authenticity, or when the company expects outside diligence soon. If you want that extra evidentiary step, notary services can help coordinate signatures without turning execution into a weeks-long project.

Keep the agreement current

An operating agreement for a two-founder bootstrapped LLC rarely fits the company twelve months later. Washington startups change fast. A priced round, SAFEs converting into equity, a founder leaving but keeping an economic interest, or a shift from member-managed to manager-managed governance can all make the original document inaccurate.

The risk is not abstract. If the agreement says one thing and the company operates another way, the written record starts working against the business. Investors notice. Buyers notice. Adverse parties notice.

Review the agreement after any event that changes economics, control, or exit rights:

- New funding or investor rights

- Founder departures, terminations, or vesting disputes

- Changes to tax treatment

- Manager appointments or board-style governance changes

- New transfer restrictions, buyout rights, or drag-along terms

- A planned sale, merger, or internal reorganization

Washington law gives LLCs substantial contractual freedom, which is helpful for startups. It also means the paper matters. If your agreement has an amendment provision, follow it exactly. Do not rely on an email thread, a Slack message, or everyone “understanding” the new arrangement.

A good maintenance habit is simple: review the agreement at least annually and after any major financing or ownership change, then adopt a written amendment or restated agreement while memories are fresh and incentives are still aligned.

For Washington founders who want operating agreements that match real startup economics, governance needs, and long-term growth plans, By Design Law Firm & Legal Consultancy, PLLC provides Seattle-based business counsel focused on practical drafting, risk management, and durable legal infrastructure for companies across Washington State.